![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-549-L

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-549-L

for the current year.

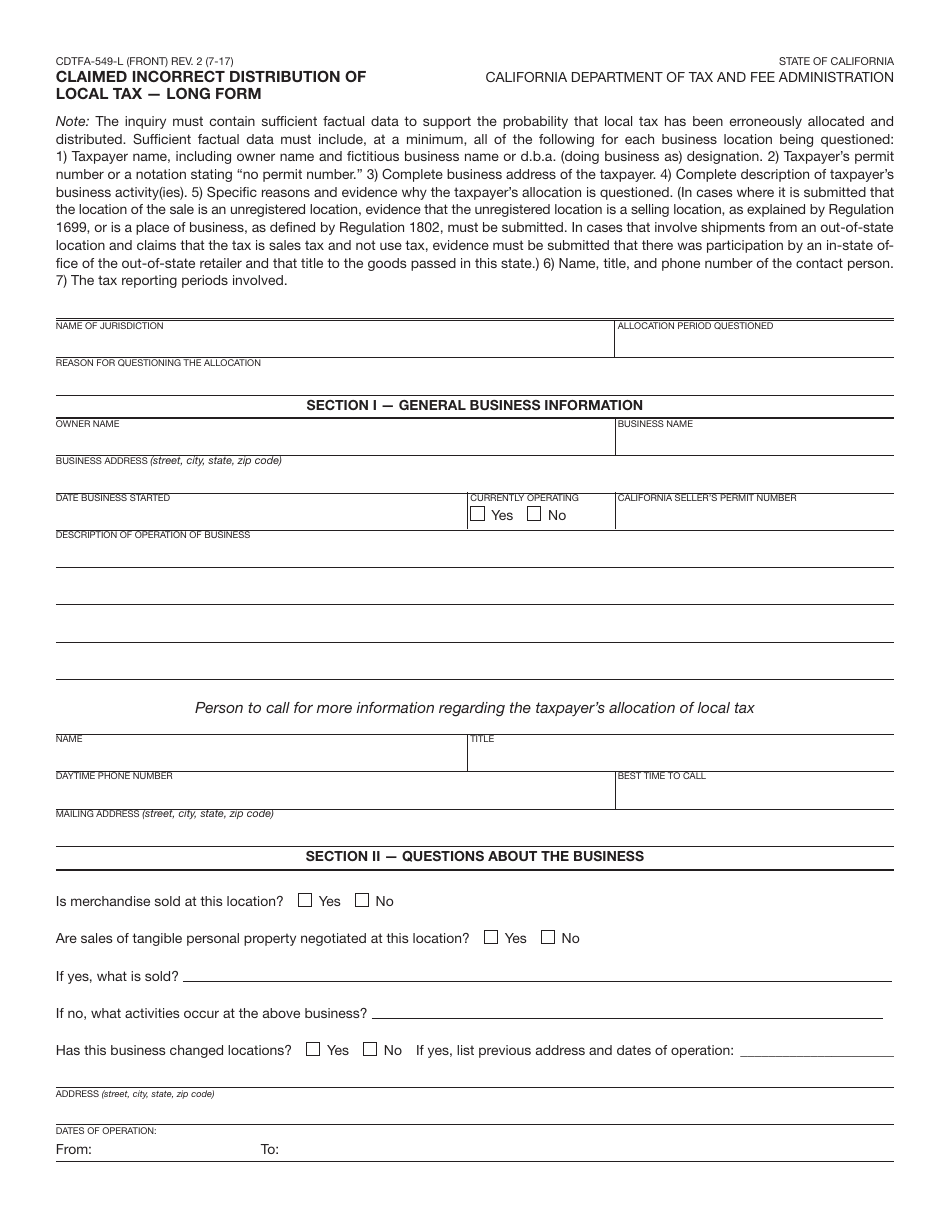

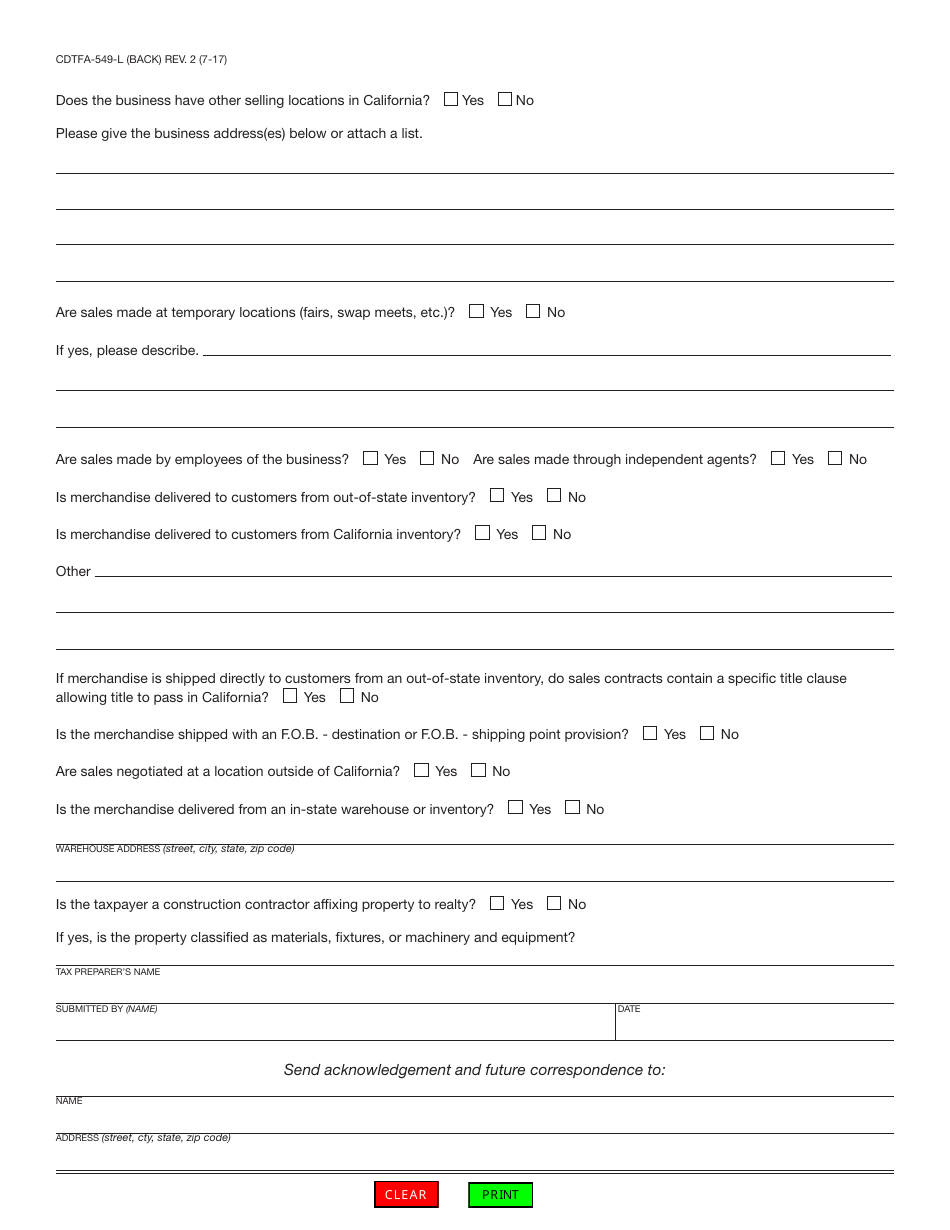

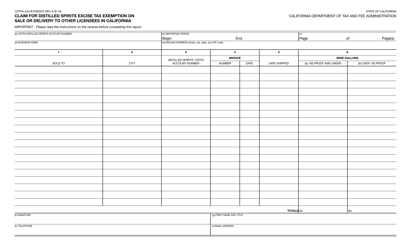

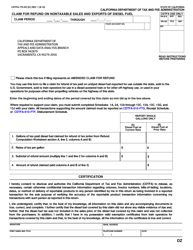

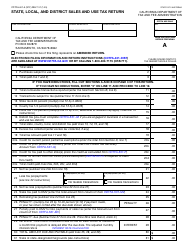

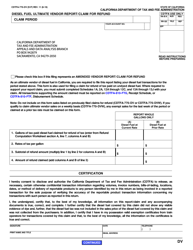

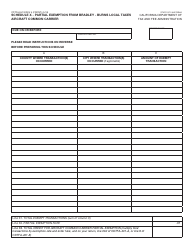

Form CDTFA-549-L Claimed Incorrect Distribution of Local Tax - Long Form - California

What Is Form CDTFA-549-L?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CDTFA-549-L?

A: Form CDTFA-549-L is a form used in California to claim an incorrect distribution of local tax.

Q: When should I use Form CDTFA-549-L?

A: You should use Form CDTFA-549-L when you believe there has been an incorrect distribution of local tax in California.

Q: What information is required on Form CDTFA-549-L?

A: Form CDTFA-549-L requires information such as your name, address, account number, the period covered by the claim, and details about the incorrect distribution.

Q: Is there a deadline for submitting Form CDTFA-549-L?

A: Yes, there is a deadline for submitting Form CDTFA-549-L. The exact deadline can vary, so it's important to check the instructions on the form or consult with the CDTFA.

Q: What happens after I submit Form CDTFA-549-L?

A: After you submit Form CDTFA-549-L, the CDTFA will review your claim and may request additional information. They will then make a determination regarding the incorrect distribution of local tax.

Q: Can I appeal the decision made on my Form CDTFA-549-L claim?

A: Yes, if you disagree with the decision made on your Form CDTFA-549-L claim, you have the right to appeal the decision and request a formal hearing.

Form Details:

- Released on July 1, 2017;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-549-L by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.

Download Form CDTFA-549-L Claimed Incorrect Distribution of Local Tax - Long Form - California

1

2