![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-401-CUTS

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-401-CUTS

for the current year.

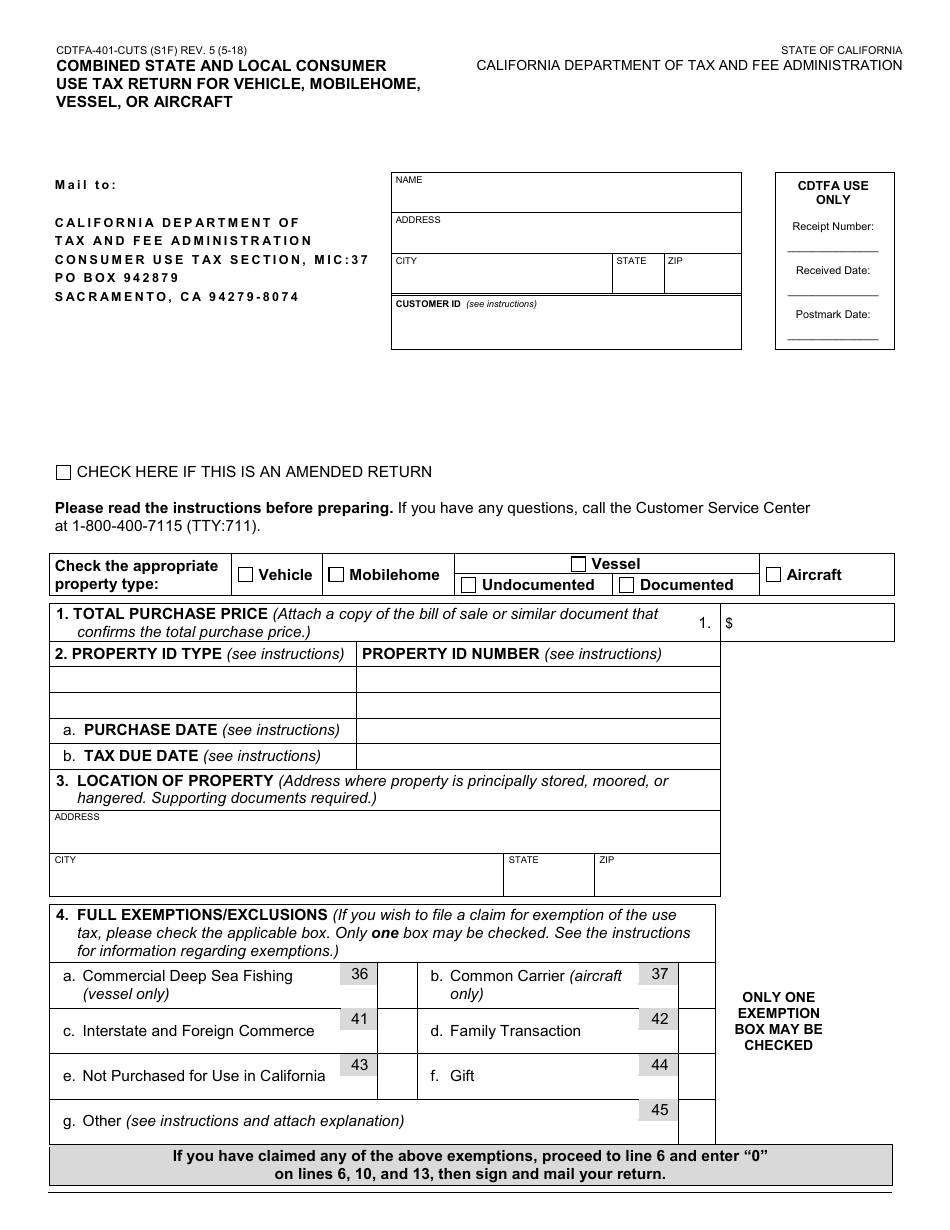

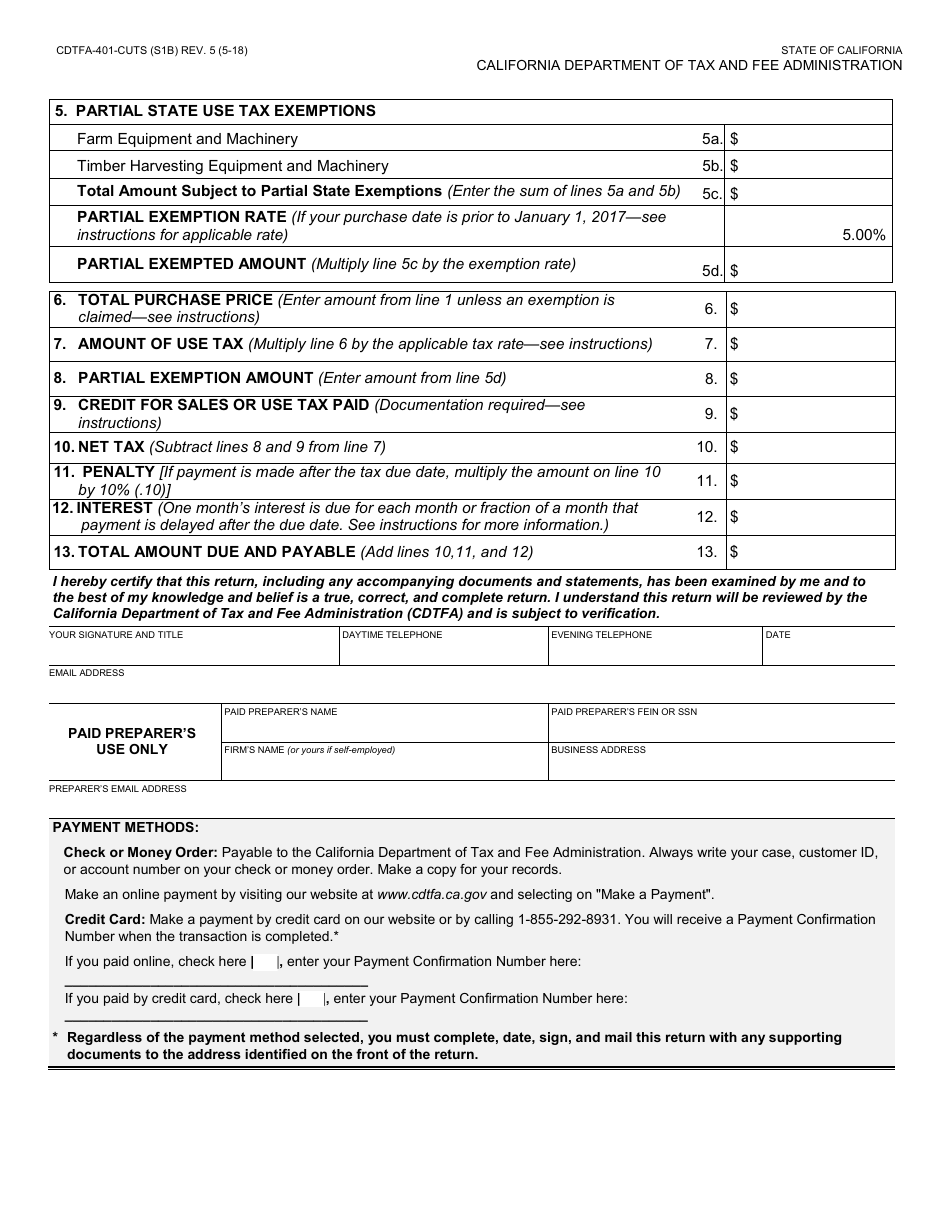

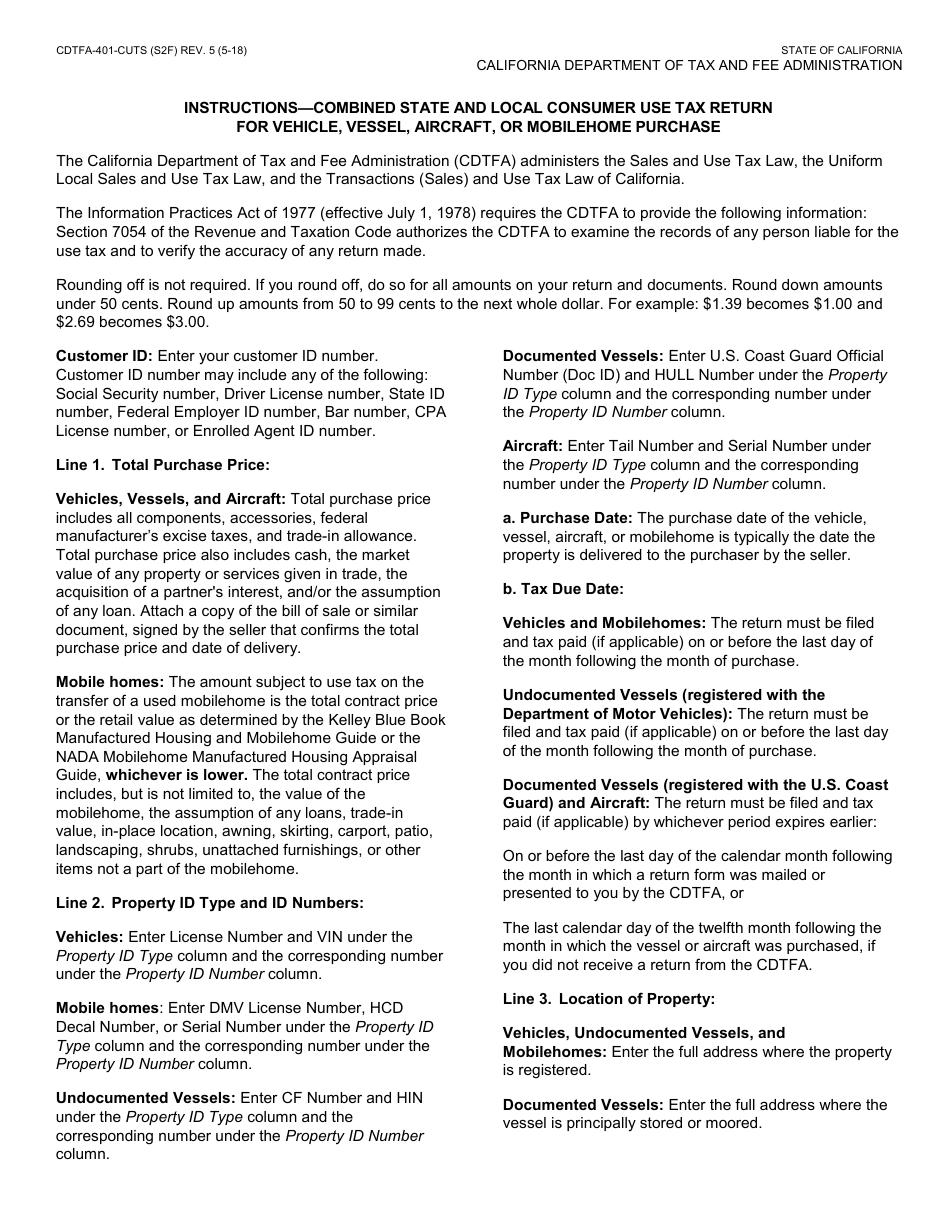

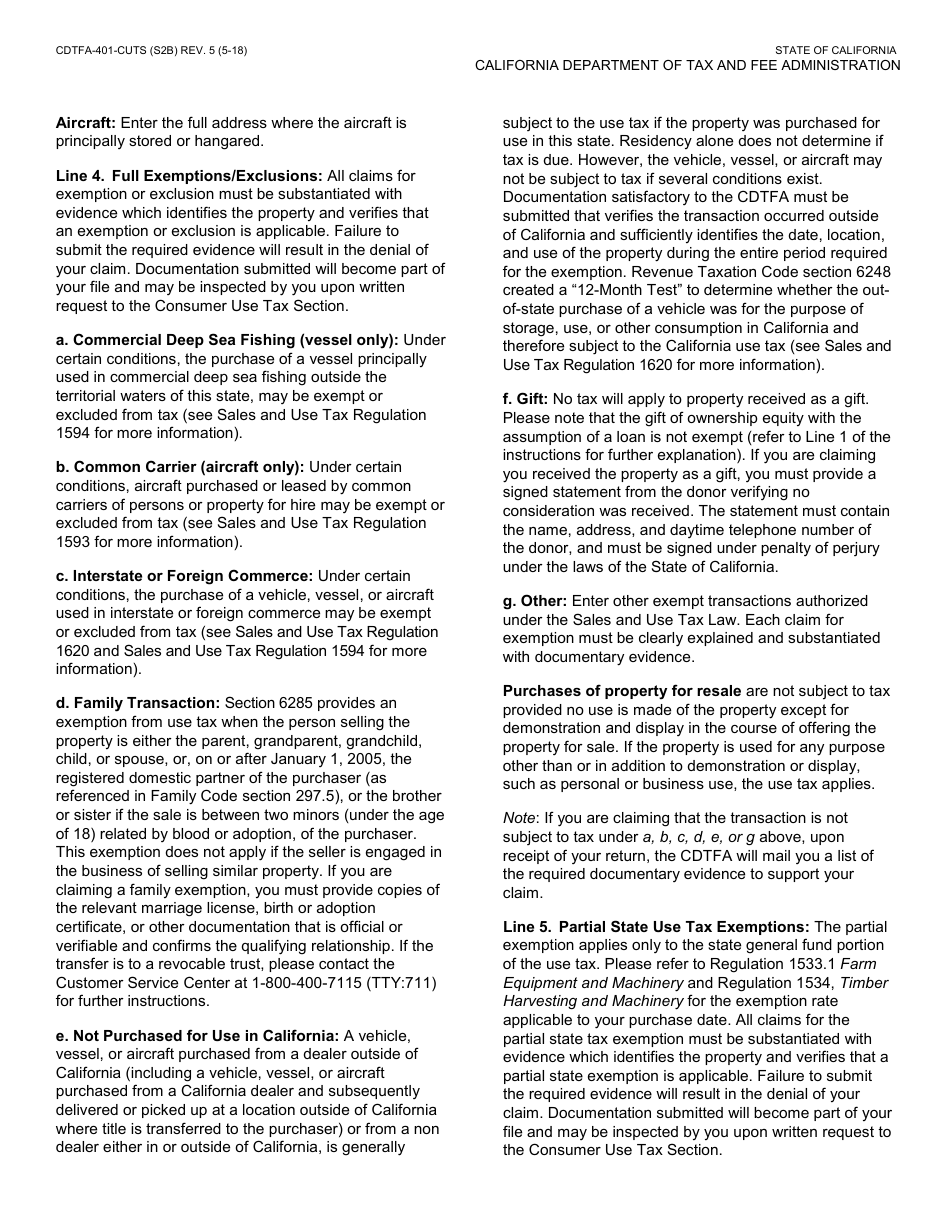

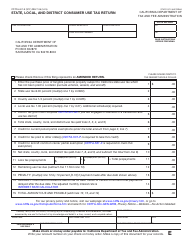

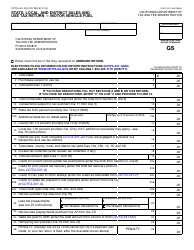

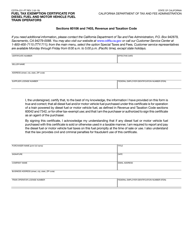

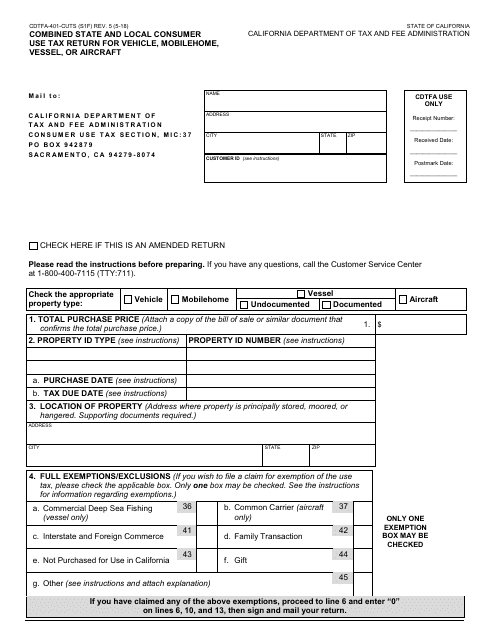

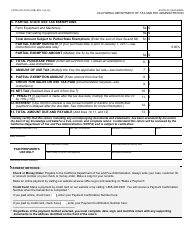

Form CDTFA-401-CUTS Combined State and Local Consumer Use Tax Return for Vehicle, Mobilehome, Vessel, or Aircraft - California

What Is Form CDTFA-401-CUTS?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CDTFA-401-CUTS?

A: Form CDTFA-401-CUTS is a Combined State and Local Consumer Use Tax Return for Vehicle, Mobilehome, Vessel, or Aircraft in California.

Q: Who needs to file Form CDTFA-401-CUTS?

A: Individuals or businesses who have purchased a vehicle, mobile home, vessel, or aircraft for use in California and are liable for paying consumer use tax need to file Form CDTFA-401-CUTS.

Q: What is consumer use tax?

A: Consumer use tax is a tax on the use, storage, or consumption of tangible personal property that was purchased for use in California but was not subject to California sales tax.

Q: What information do I need to complete Form CDTFA-401-CUTS?

A: To complete Form CDTFA-401-CUTS, you will need information about the purchase of the vehicle, mobile home, vessel, or aircraft, including the purchase price, date of purchase, and seller information.

Q: When is the deadline to file Form CDTFA-401-CUTS?

A: Form CDTFA-401-CUTS is due on or before the last day of the month following the month in which the purchase was made.

Q: Are there any penalties for not filing Form CDTFA-401-CUTS?

A: Yes, failing to file Form CDTFA-401-CUTS or paying the required consumer use tax can result in penalties and interest being assessed by the CDTFA.

Q: Can I claim any exemptions on Form CDTFA-401-CUTS?

A: Yes, there are certain exemptions available for certain types of purchases. You should consult the instructions for Form CDTFA-401-CUTS or contact the CDTFA for more information on claiming exemptions.

Form Details:

- Released on May 1, 2018;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-401-CUTS by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.

Download Form CDTFA-401-CUTS Combined State and Local Consumer Use Tax Return for Vehicle, Mobilehome, Vessel, or Aircraft - California

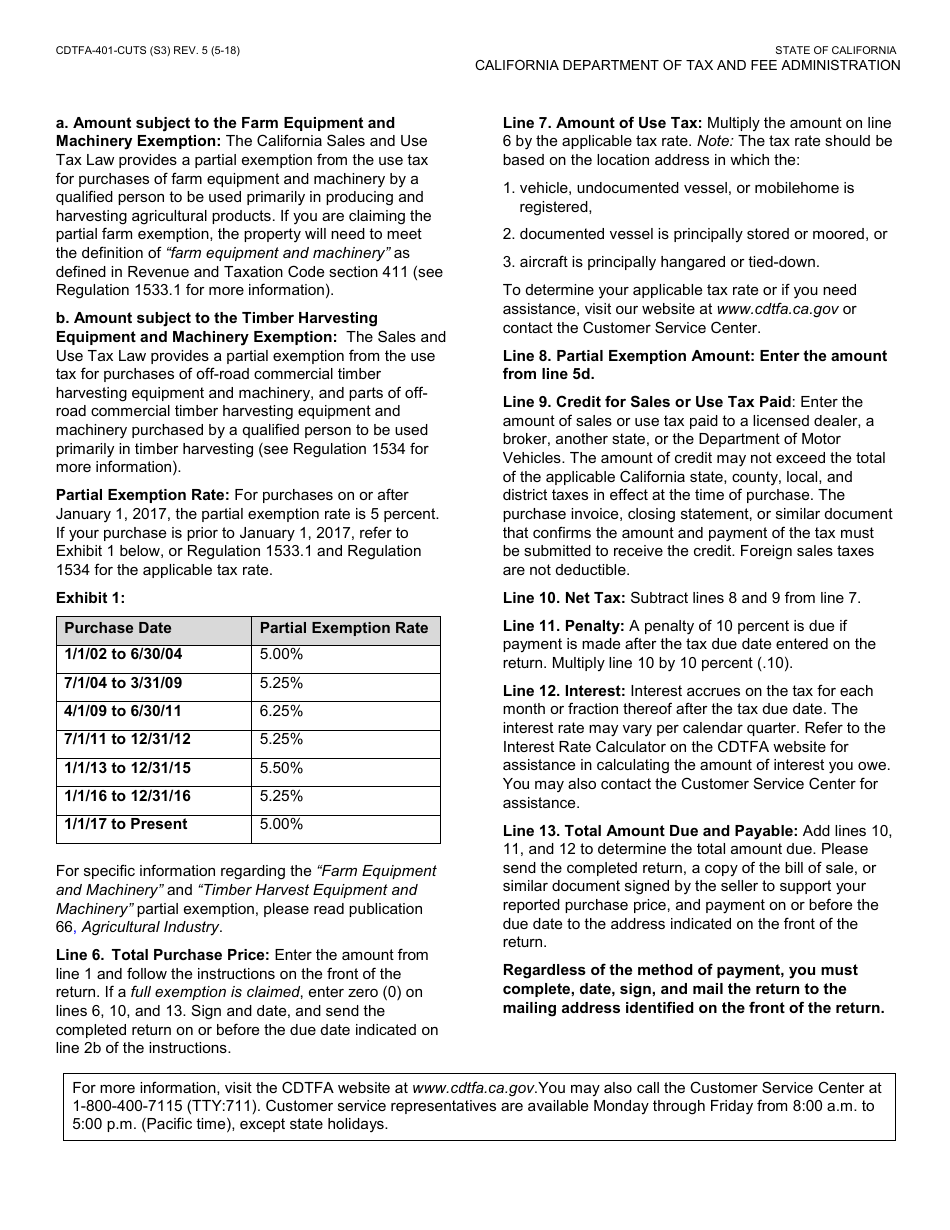

1

2

3

4

5