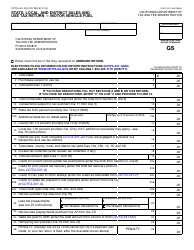

![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CDTFA-401-A

for the current year.

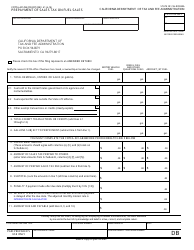

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CDTFA-401-A

for the current year.

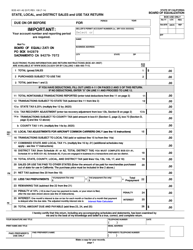

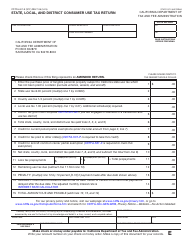

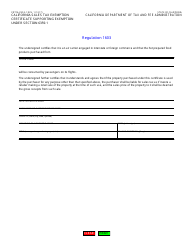

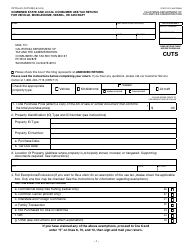

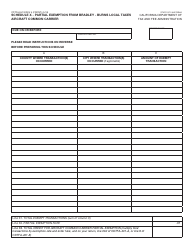

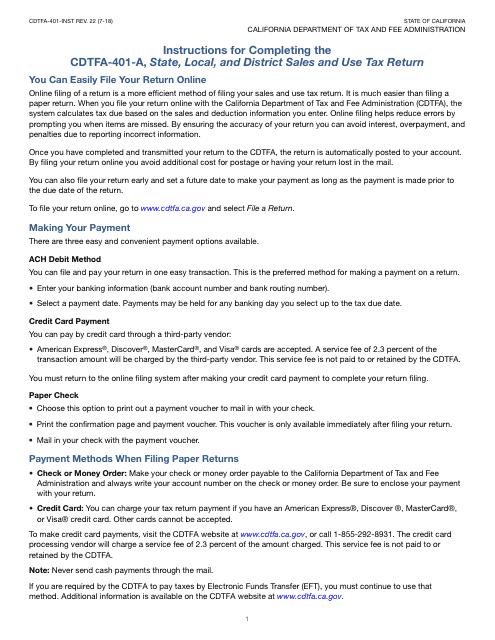

Instructions for Form CDTFA-401-A State, Local, and District Sales and Use Tax Return - California

This document contains official instructions for Form CDTFA-401-A , State, Local, and District Sales and Use Tax Return - a form released and collected by the California Department of Tax and Fee Administration. An up-to-date fillable Form CDTFA-401-A is available for download through this link.

FAQ

Q: Who needs to file Form CDTFA-401-A?

A: Businesses registered with the California Department of Tax and Fee Administration (CDTFA) and engaged in sales and use tax activities in California.

Q: What is Form CDTFA-401-A used for?

A: Form CDTFA-401-A is used to report and pay state, local, and district sales and use taxes owed to the State of California.

Q: When is Form CDTFA-401-A due?

A: Form CDTFA-401-A must be filed and the taxes paid on or before the last day of the month following the reporting period.

Q: What information is required on Form CDTFA-401-A?

A: Form CDTFA-401-A requires information such as the business's name, address, and account number, as well as details of sales and purchases subject to sales and use tax.

Q: Are there any penalties for late or incorrect filing of Form CDTFA-401-A?

A: Yes, there are penalties for late or incorrect filing of Form CDTFA-401-A. It is important to file on time and ensure all information is accurate to avoid penalties and interest charges.

Q: What do I do if I have questions about Form CDTFA-401-A?

A: If you have questions about Form CDTFA-401-A, you can contact the California Department of Tax and Fee Administration's customer service for assistance.

Instruction Details:

- This 11-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the California Department of Tax and Fee Administration.

Download Instructions for Form CDTFA-401-A State, Local, and District Sales and Use Tax Return - California

1

2

3

4

5

6

7

8

9

10

11