![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-501-WG

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-501-WG

for the current year.

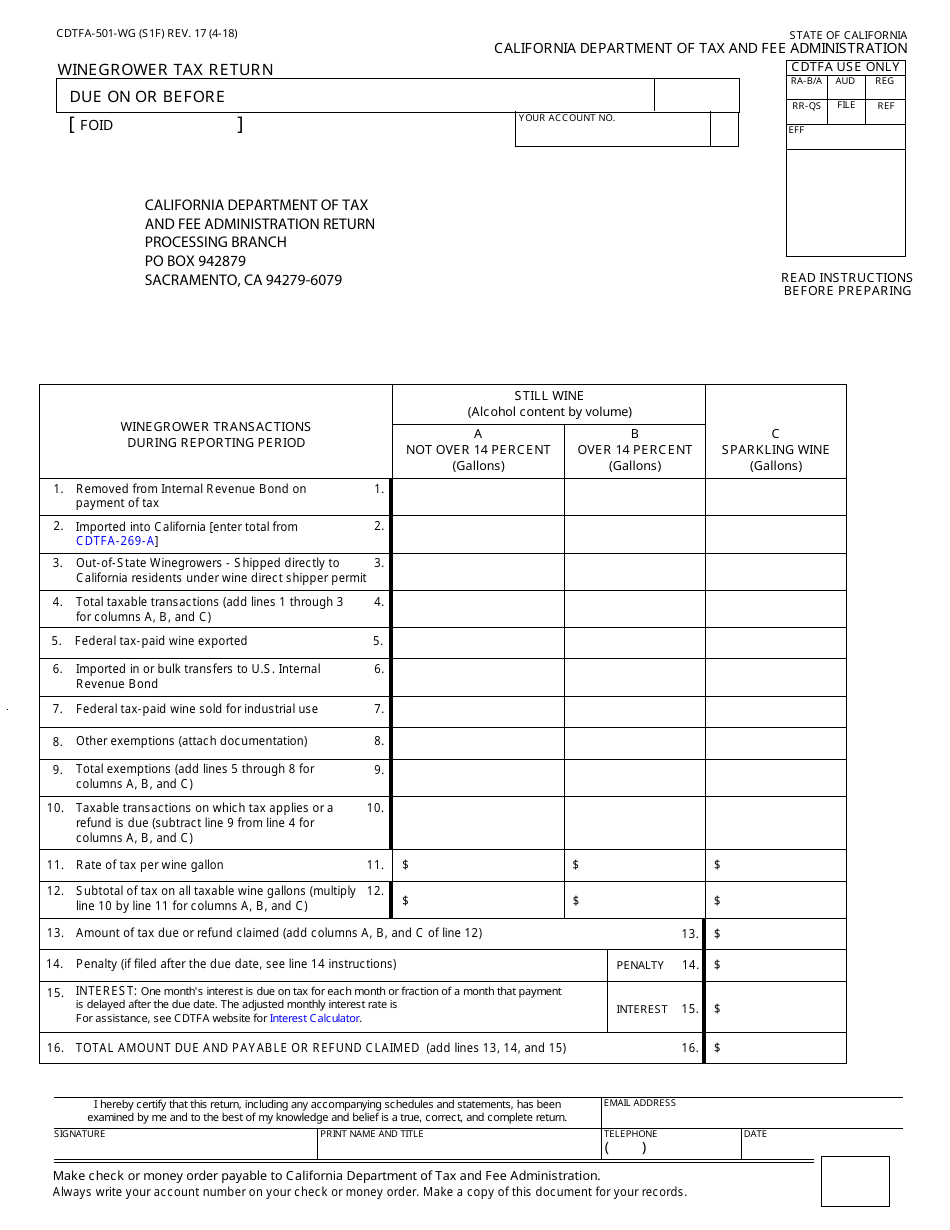

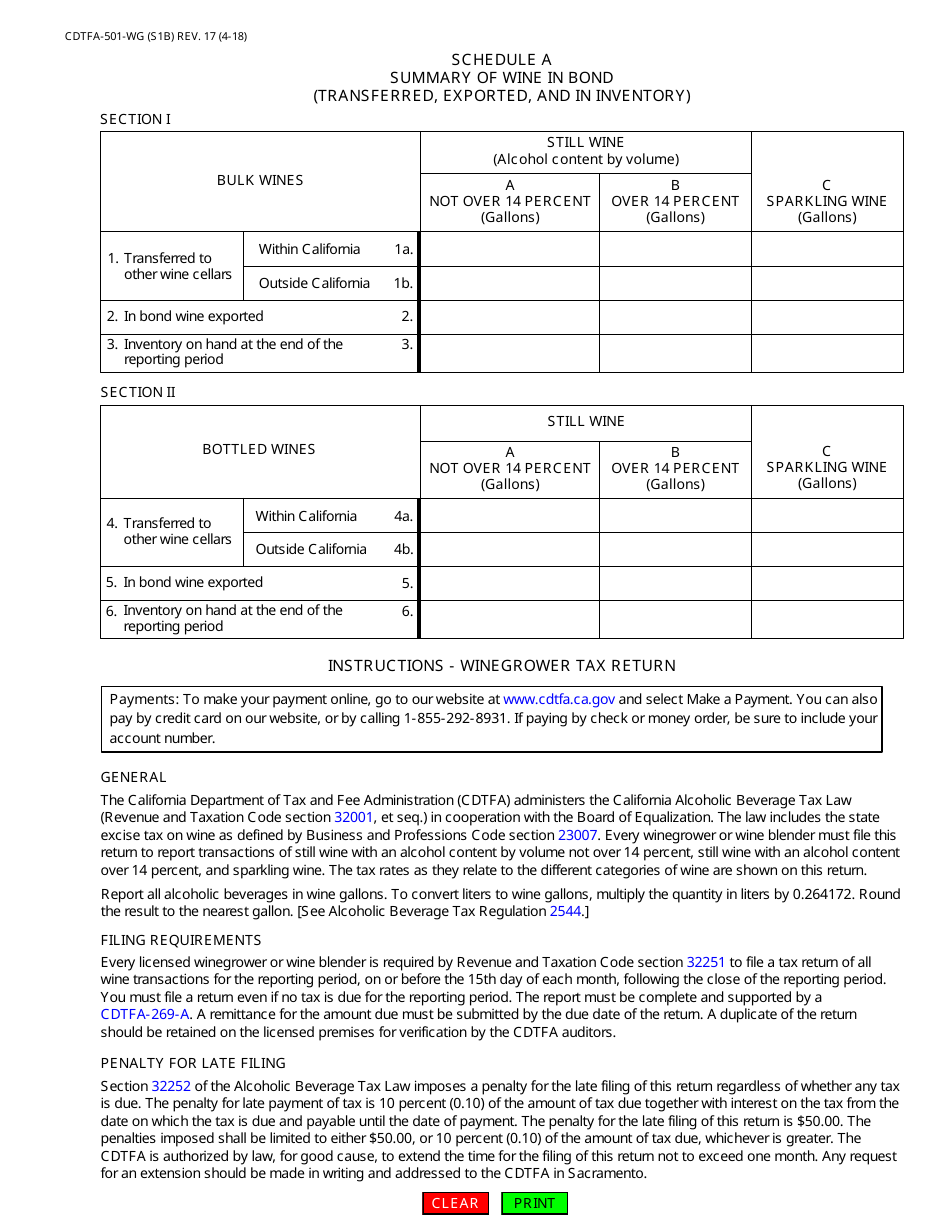

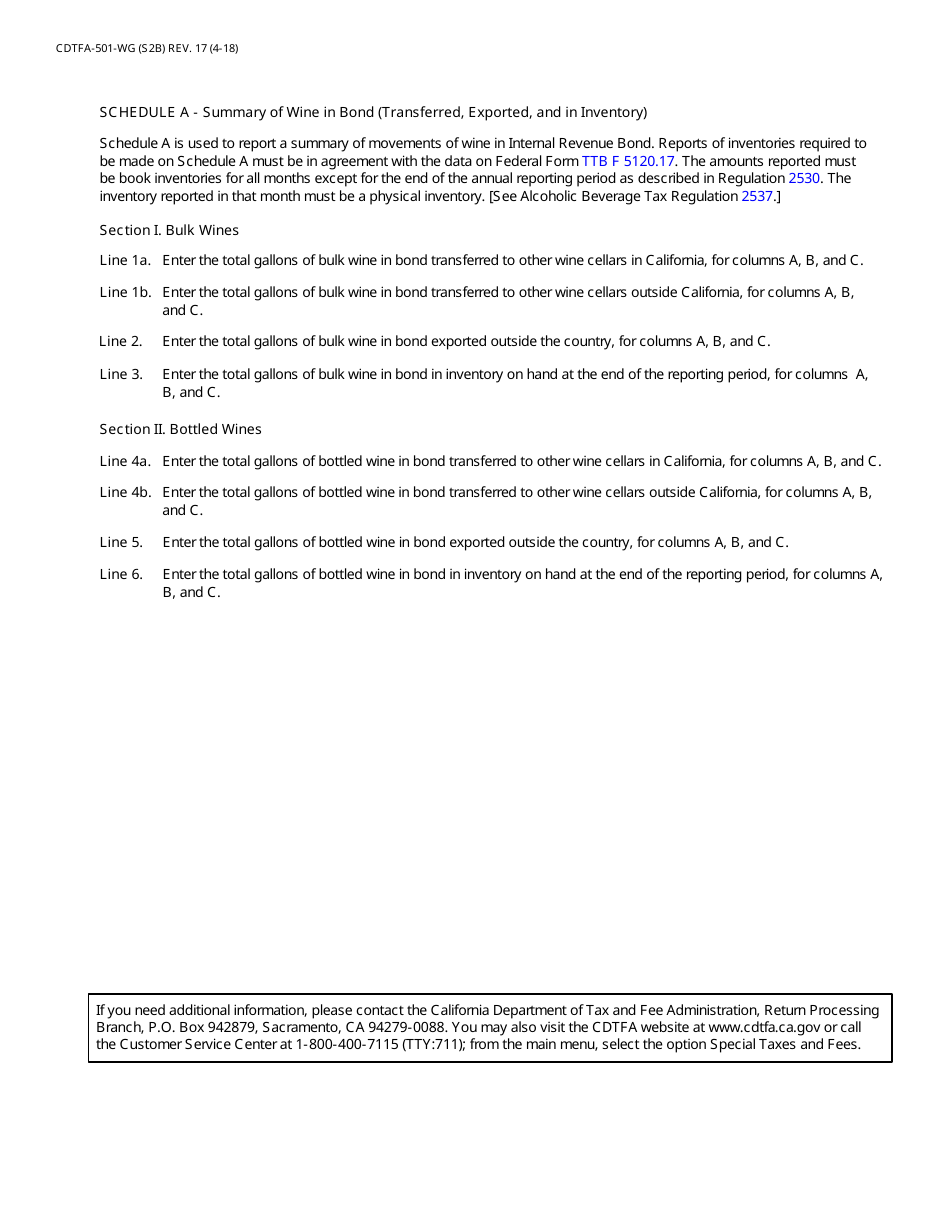

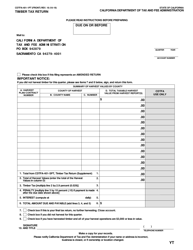

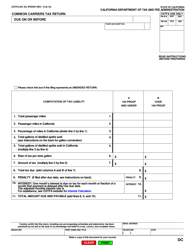

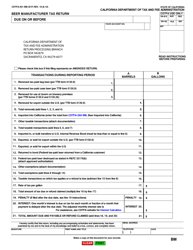

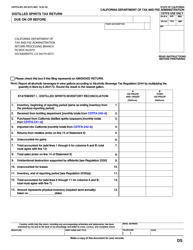

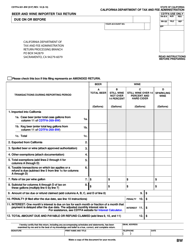

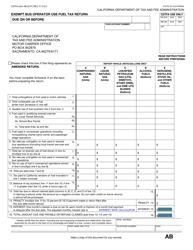

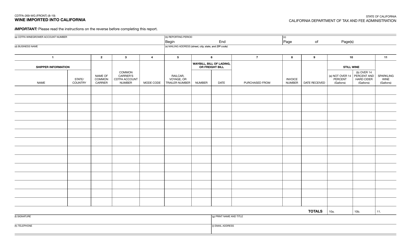

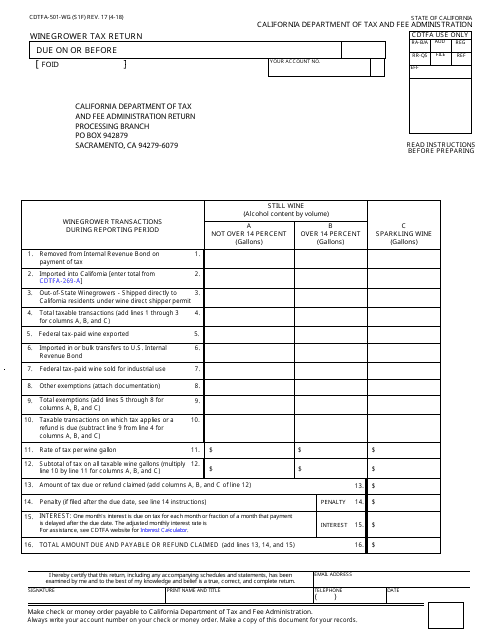

Form CDTFA-501-WG Winegrower Tax Return - California

Fill PDF Online

Fill out online for free

without registration or credit card

What Is Form CDTFA-501-WG?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

Form Details:

- Released on April 1, 2018;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-501-WG by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.

Download Form CDTFA-501-WG Winegrower Tax Return - California

1

2

3

4