![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CERT-106

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CERT-106

for the current year.

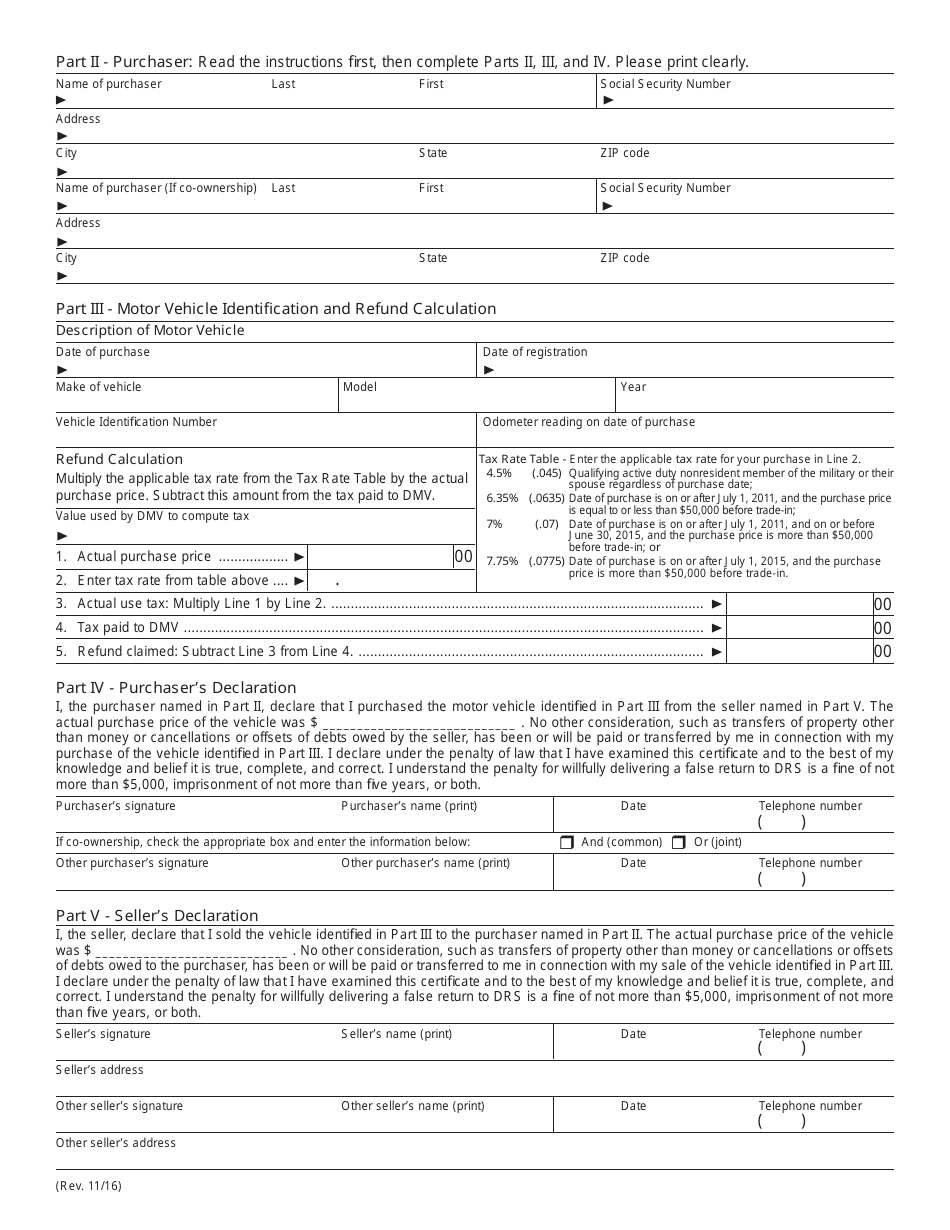

Form CERT-106 Claim for Refund of Use Tax Paid on Motor Vehicle Purchased From Other Than a Motor Vehicle Dealer - Connecticut

What Is Form CERT-106?

This is a legal form that was released by the Connecticut Department of Revenue Services - a government authority operating within Connecticut. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is CERT-106?

A: CERT-106 is a form used in Connecticut to claim a refund of use tax paid on a motor vehicle purchased from other than a motor vehicle dealer.

Q: What is use tax?

A: Use tax is a tax on goods purchased for use, storage or other consumption in Connecticut.

Q: Who can use CERT-106 form?

A: Anyone who paid use tax on a motor vehicle purchased from other than a motor vehicle dealer in Connecticut can use CERT-106 form.

Q: How tofill out CERT-106 form?

A: You need to provide detailed information about the motor vehicle and the purchase, including the amount of tax paid. You also need to sign and date the form.

Q: What documents should I include with CERT-106 form?

A: You should include copies of all relevant documents such as purchase receipts, bill of sale, and proof of payment of use tax.

Q: What is the deadline to submit CERT-106 form?

A: The CERT-106 form must be filed within 3 years from the date of purchase.

Q: How long does it take to process a CERT-106 refund claim?

A: The processing time can vary, but the department aims to process refund claims within 90 days of receipt of a complete application.

Q: Can I claim a refund of use tax paid on a motor vehicle purchased from a motor vehicle dealer?

A: No, you cannot claim a refund of use tax paid on a motor vehicle purchased from a motor vehicle dealer using CERT-106 form. You need to contact the dealer directly for any refund request.

Form Details:

- Released on November 1, 2016;

- The latest edition provided by the Connecticut Department of Revenue Services;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form CERT-106 by clicking the link below or browse more documents and templates provided by the Connecticut Department of Revenue Services.

Download Form CERT-106 Claim for Refund of Use Tax Paid on Motor Vehicle Purchased From Other Than a Motor Vehicle Dealer - Connecticut

1

2