![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form ET-1

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form ET-1

for the current year.

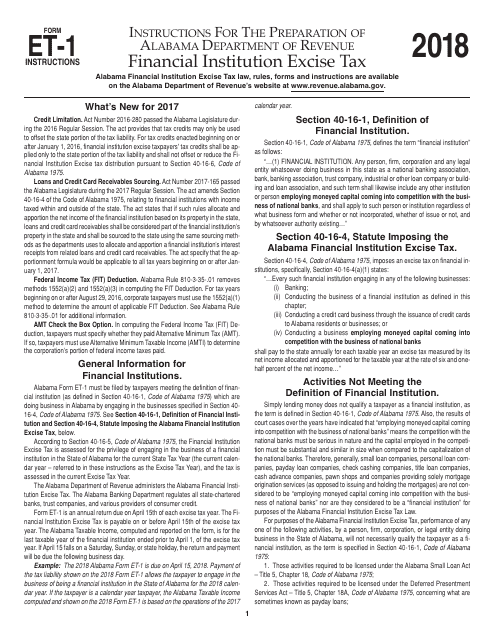

Instructions for Form ET-1 Financial Institution Excise Tax - Alabama

This document contains official instructions for Form ET-1 , Financial Institution Excise Tax - a form released and collected by the Alabama Department of Revenue. An up-to-date fillable Form ET-1 is available for download through this link.

FAQ

Q: What is Form ET-1?

A: Form ET-1 is the Financial Institution Excise Tax form that needs to be filed by financial institutions in Alabama.

Q: Who needs to file Form ET-1?

A: Financial institutions operating in Alabama need to file Form ET-1.

Q: What is the purpose of Form ET-1?

A: The purpose of Form ET-1 is to report and pay the Financial Institution Excise Tax, which is imposed on financial institutions by the state of Alabama.

Q: How often do financial institutions need to file Form ET-1?

A: Financial institutions need to file Form ET-1 annually.

Q: What information is required to complete Form ET-1?

A: To complete Form ET-1, financial institutions need to provide information such as their gross receipts, net income, and any tax credits they are claiming.

Q: When is Form ET-1 due?

A: Form ET-1 is due on or before the last day of the fourth month following the close of the financial institution's taxable year.

Q: Are there any penalties for late or incorrect filing of Form ET-1?

A: Yes, there are penalties for late or incorrect filing of Form ET-1. Financial institutions may be subject to interest charges and penalties for failure to file or pay the tax on time.

Instruction Details:

- This 6-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Alabama Department of Revenue.

1

2

3

4

5

6