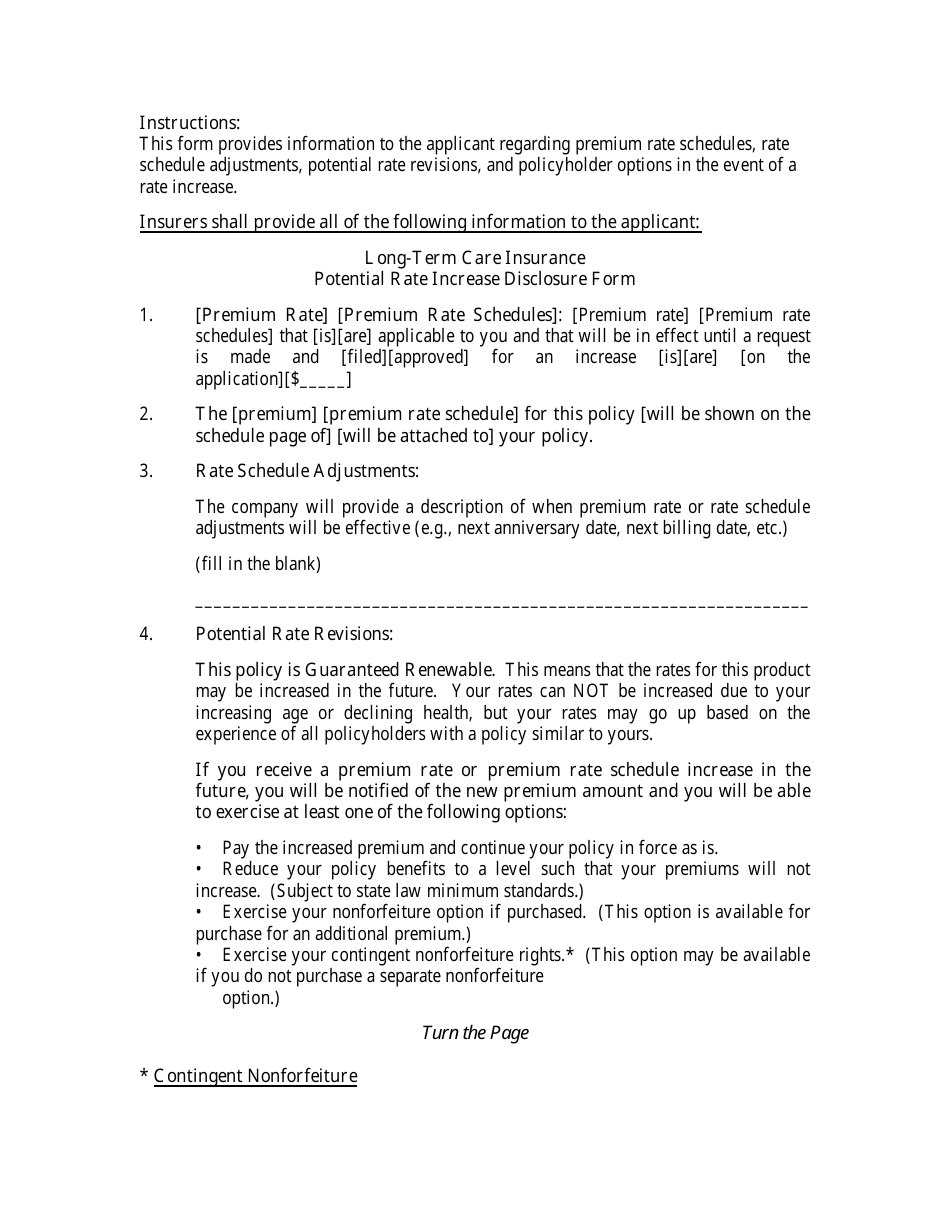

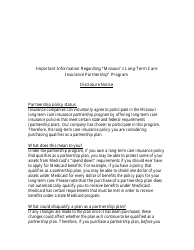

Form LTC-F Long-Term Care Insurance Potential Rate Increase Disclosure Form - Missouri

What Is Form LTC-F?

This is a legal form that was released by the Missouri Department of Commerce and Insurance - a government authority operating within Missouri. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the Form LTC-F?

A: The Form LTC-F is the Long-Term Care Insurance Potential Rate Increase Disclosure Form.

Q: What is the purpose of the Form LTC-F?

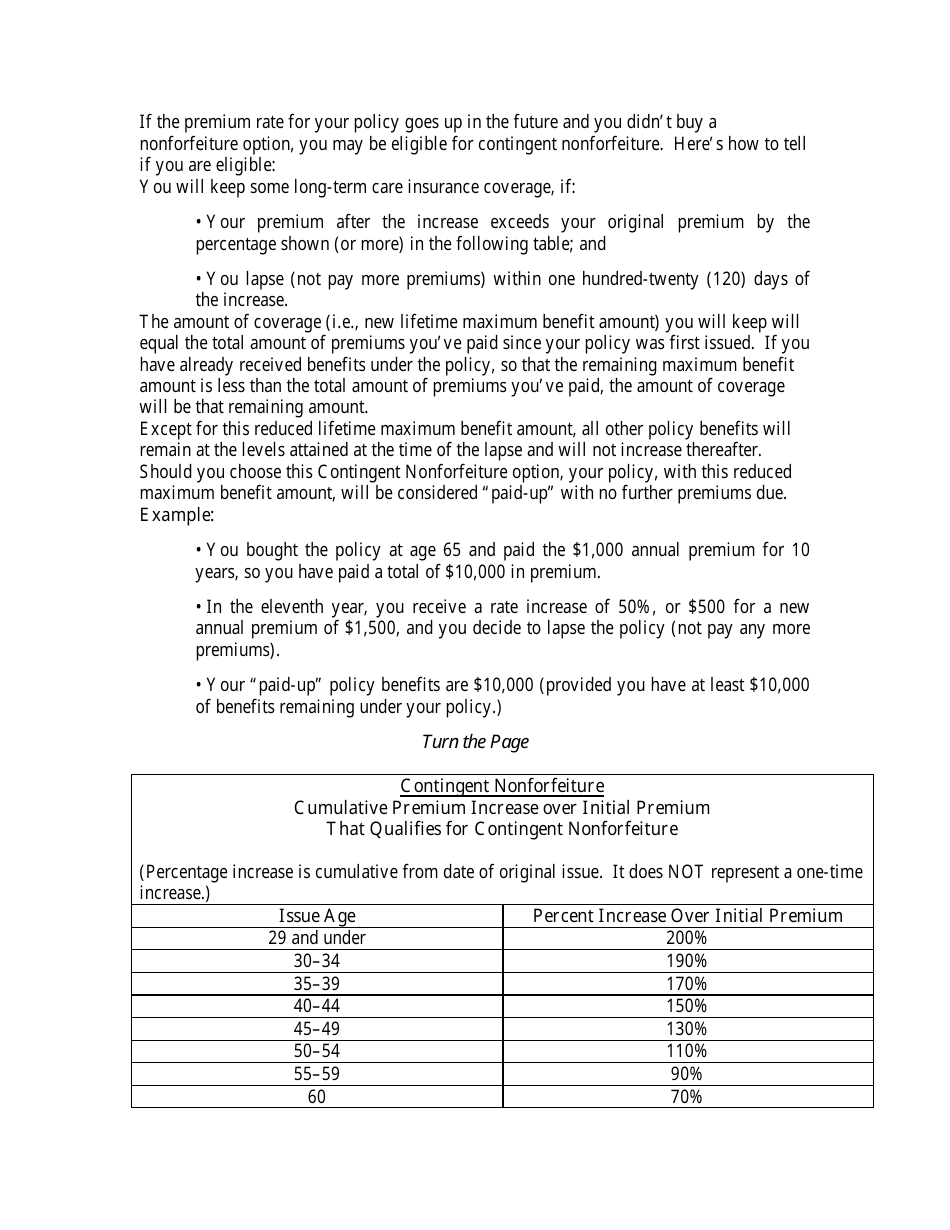

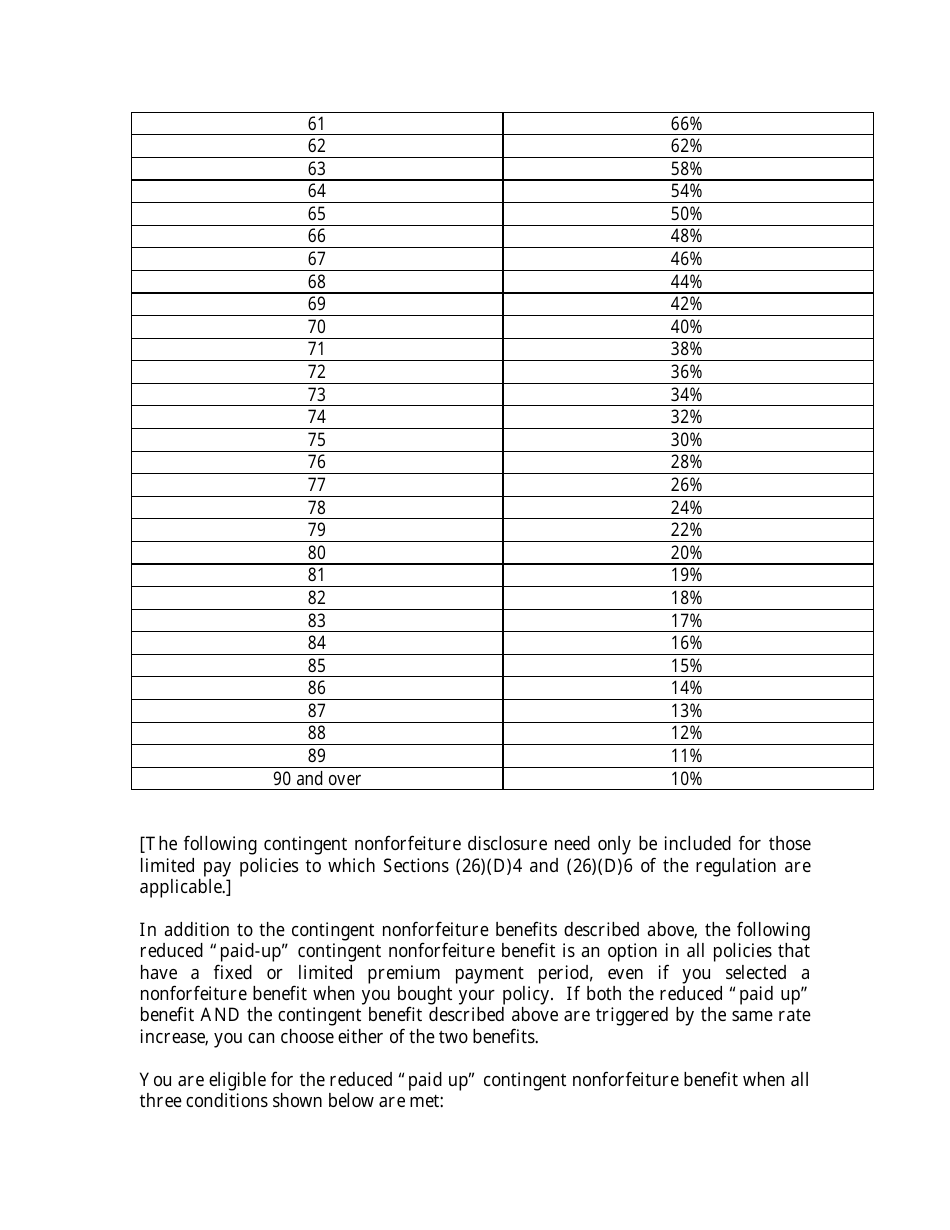

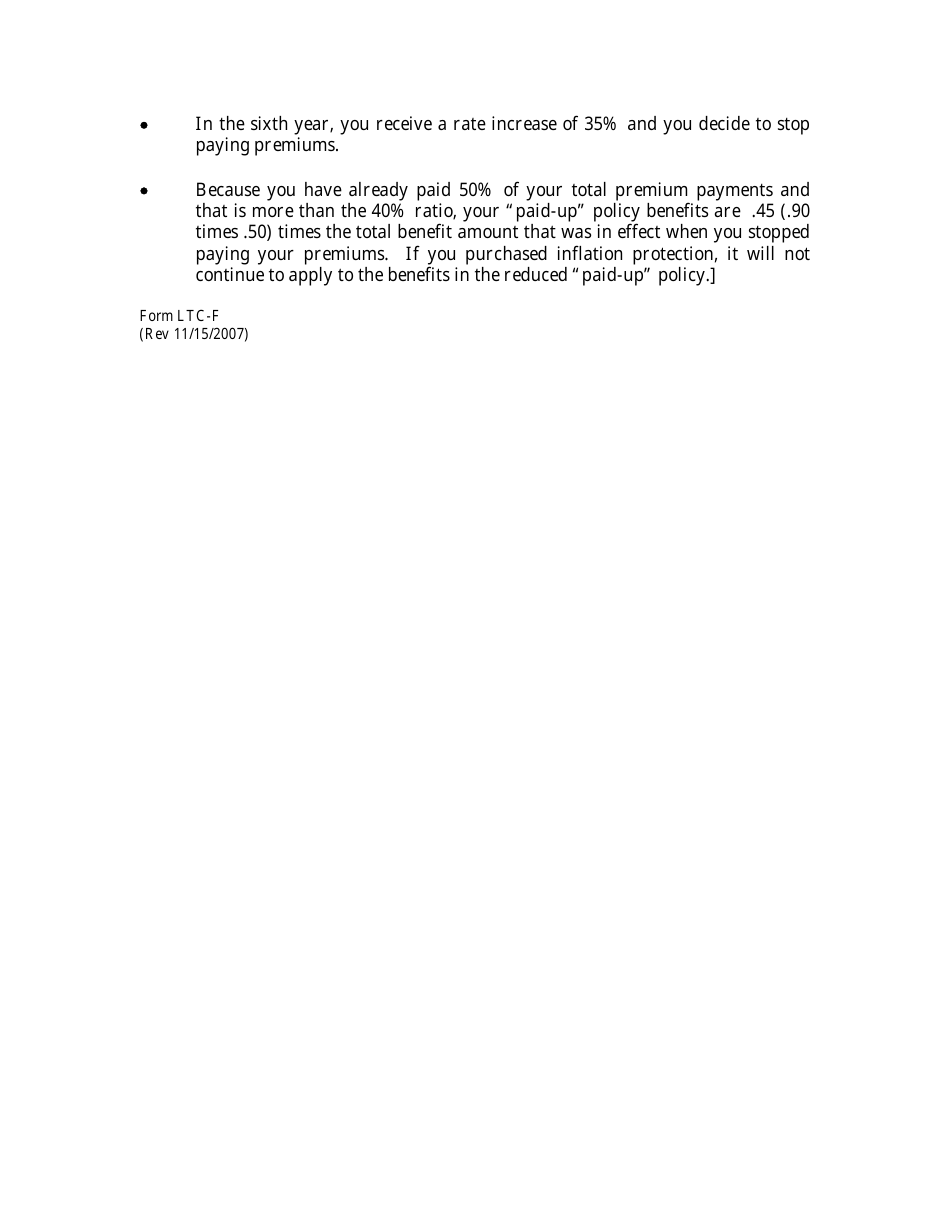

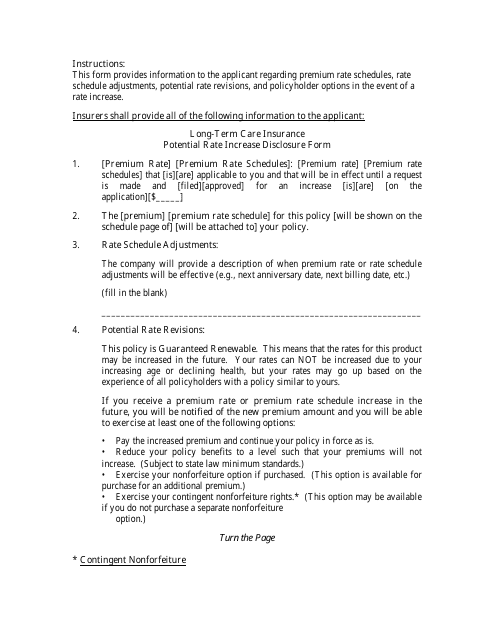

A: The purpose of the Form LTC-F is to provide information about potential rate increases for long-term care insurance in Missouri.

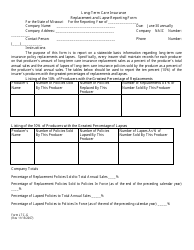

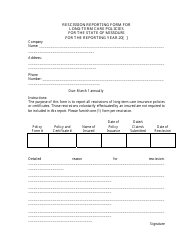

Q: Who is required to complete the Form LTC-F?

A: Insurance companies offering long-term care insurance in Missouri are required to complete the Form LTC-F.

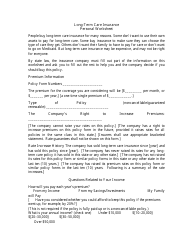

Q: What information does the Form LTC-F provide?

A: The Form LTC-F provides information about potential rate increases for long-term care insurance policies, including the factors that may affect future premium rates.

Q: Why is it important to have a disclosure form like Form LTC-F?

A: Having a disclosure form like Form LTC-F is important because it helps consumers understand the potential rate increases for long-term care insurance and make informed decisions about their coverage.

Q: Are insurance companies legally required to fill out the Form LTC-F?

A: Yes, insurance companies offering long-term care insurance in Missouri are legally required to fill out the Form LTC-F.

Form Details:

- Released on November 15, 2007;

- The latest edition provided by the Missouri Department of Commerce and Insurance;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form LTC-F by clicking the link below or browse more documents and templates provided by the Missouri Department of Commerce and Insurance.

Download Form LTC-F Long-Term Care Insurance Potential Rate Increase Disclosure Form - Missouri

1

2

3

4

5