![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 93

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 93

for the current year.

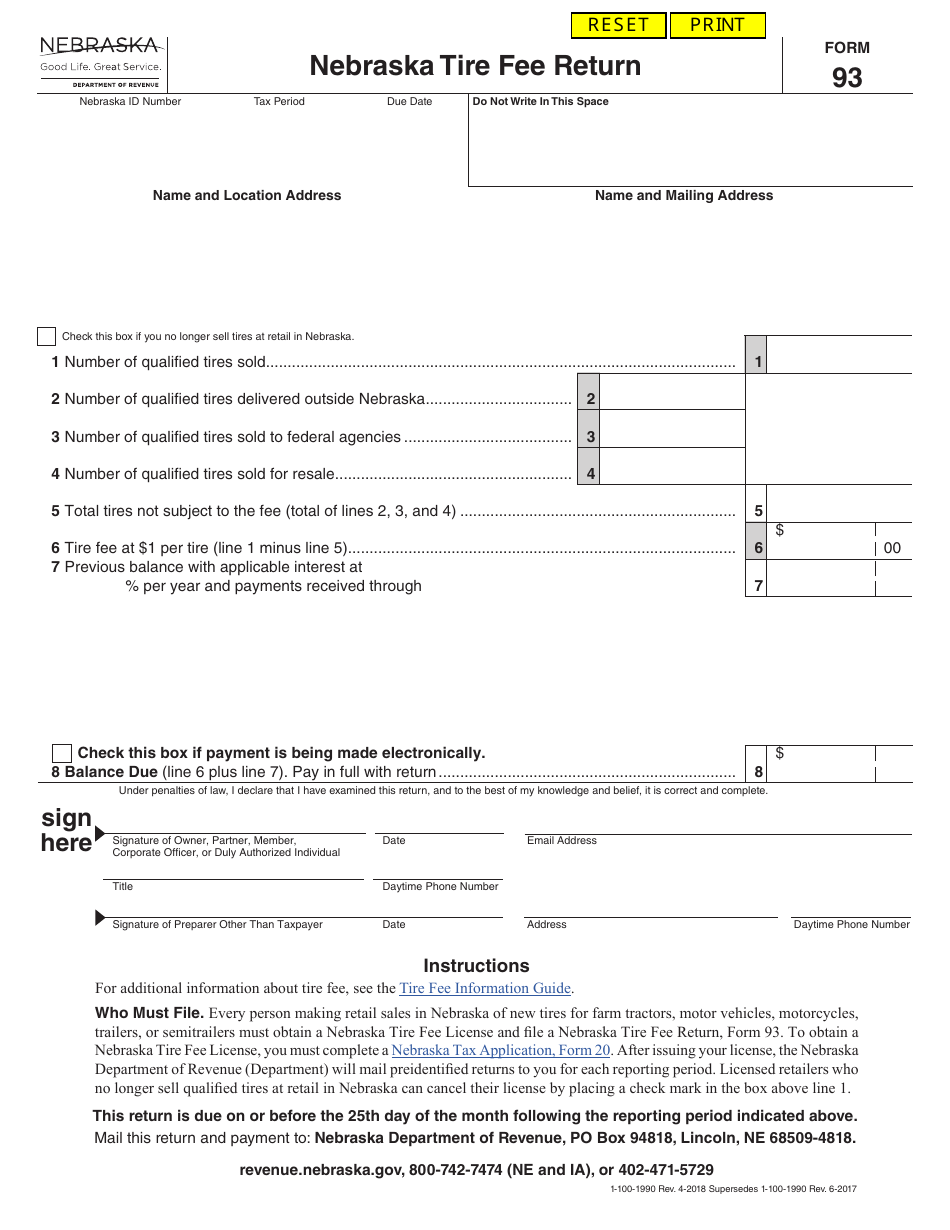

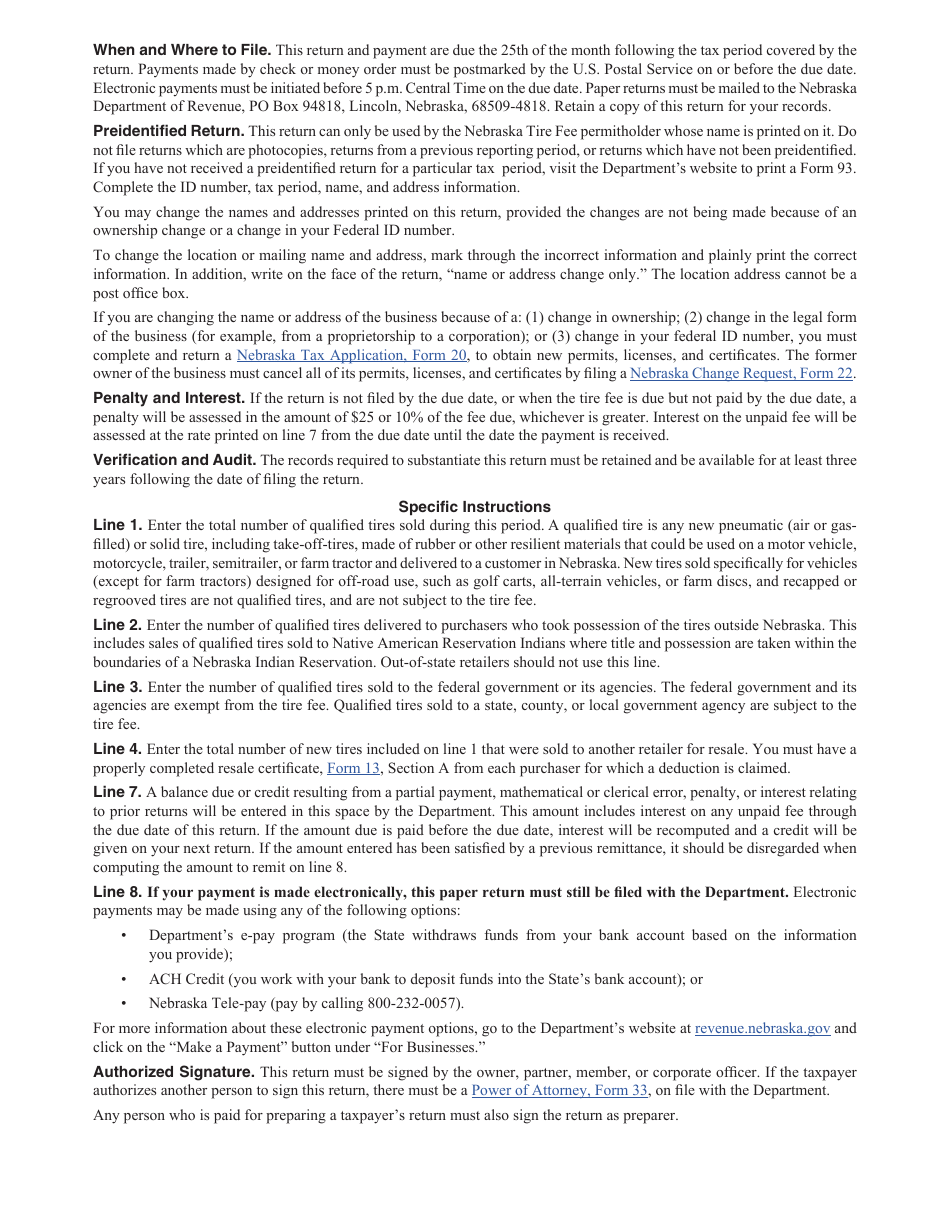

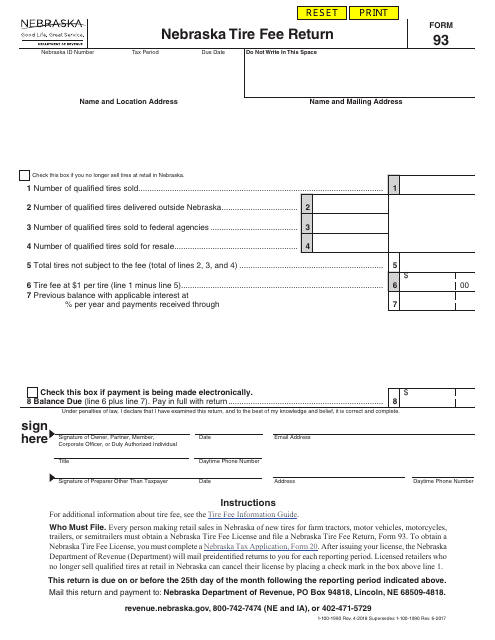

Form 93 Nebraska Tire Fee Return - Nebraska

What Is Form 93?

This is a legal form that was released by the Nebraska Department of Revenue - a government authority operating within Nebraska. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the Form 93 Nebraska Tire Fee Return?

A: The Form 93 Nebraska Tire Fee Return is a document used to report and pay the tire fee owed by retailers in Nebraska.

Q: Who needs to file the Form 93 Nebraska Tire Fee Return?

A: Retailers who sell new tires in Nebraska are required to file the Form 93 Nebraska Tire Fee Return.

Q: How often do I need to file the Form 93 Nebraska Tire Fee Return?

A: The Form 93 Nebraska Tire Fee Return must be filed on a quarterly basis.

Q: What is the purpose of the Nebraska Tire Fee?

A: The Nebraska Tire Fee is collected to support the proper disposal of used tires and to minimize the environmental impact of waste tires.

Form Details:

- Released on April 1, 2018;

- The latest edition provided by the Nebraska Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 93 by clicking the link below or browse more documents and templates provided by the Nebraska Department of Revenue.

Download Form 93 Nebraska Tire Fee Return - Nebraska

1

2