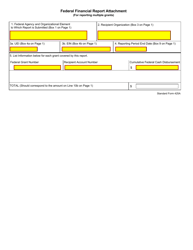

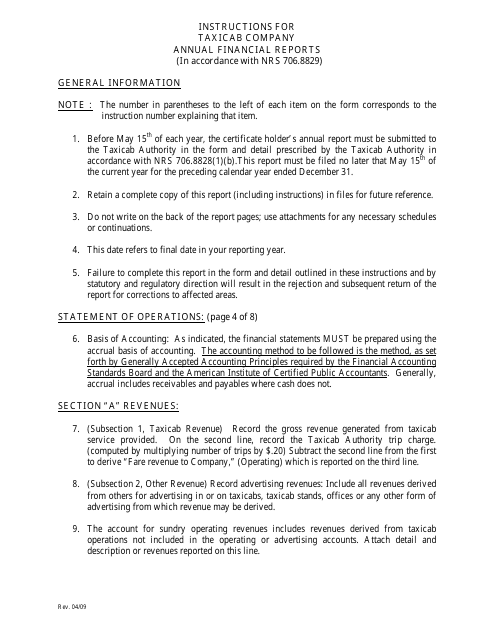

Annual Financial Report Form - Nevada

Annual Financial Report Form is a legal document that was released by the Nevada Department of Business and Industry - a government authority operating within Nevada.

FAQ

Q: What is the Annual Financial Report Form?

A: The Annual Financial Report Form is a form that needs to be filled out by certain organizations in Nevada to report their financial information.

Q: Who needs to fill out the Annual Financial Report Form?

A: Certain organizations in Nevada, such as non-profit organizations and political action committees, need to fill out the Annual Financial Report Form.

Q: What information needs to be reported on the Annual Financial Report Form?

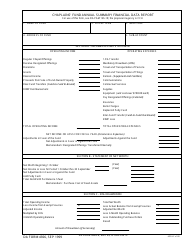

A: The form requires organizations to report their income, expenses, assets, and liabilities.

Q: When is the deadline to submit the Annual Financial Report Form?

A: The deadline to submit the Annual Financial Report Form varies depending on the organization, but generally falls within a few months after the end of the fiscal year.

Q: What happens if an organization fails to submit the Annual Financial Report Form?

A: Failure to submit the form may result in penalties or legal consequences for the organization.

Q: Is the Annual Financial Report Form confidential?

A: The Annual Financial Report Form is considered public record and can be accessed by the public.

Form Details:

- Released on April 1, 2009;

- The latest edition currently provided by the Nevada Department of Business and Industry;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of the form by clicking the link below or browse more documents and templates provided by the Nevada Department of Business and Industry.

Download Annual Financial Report Form - Nevada

1

2

3

4

5

6

7

8

9

10

11

12

13