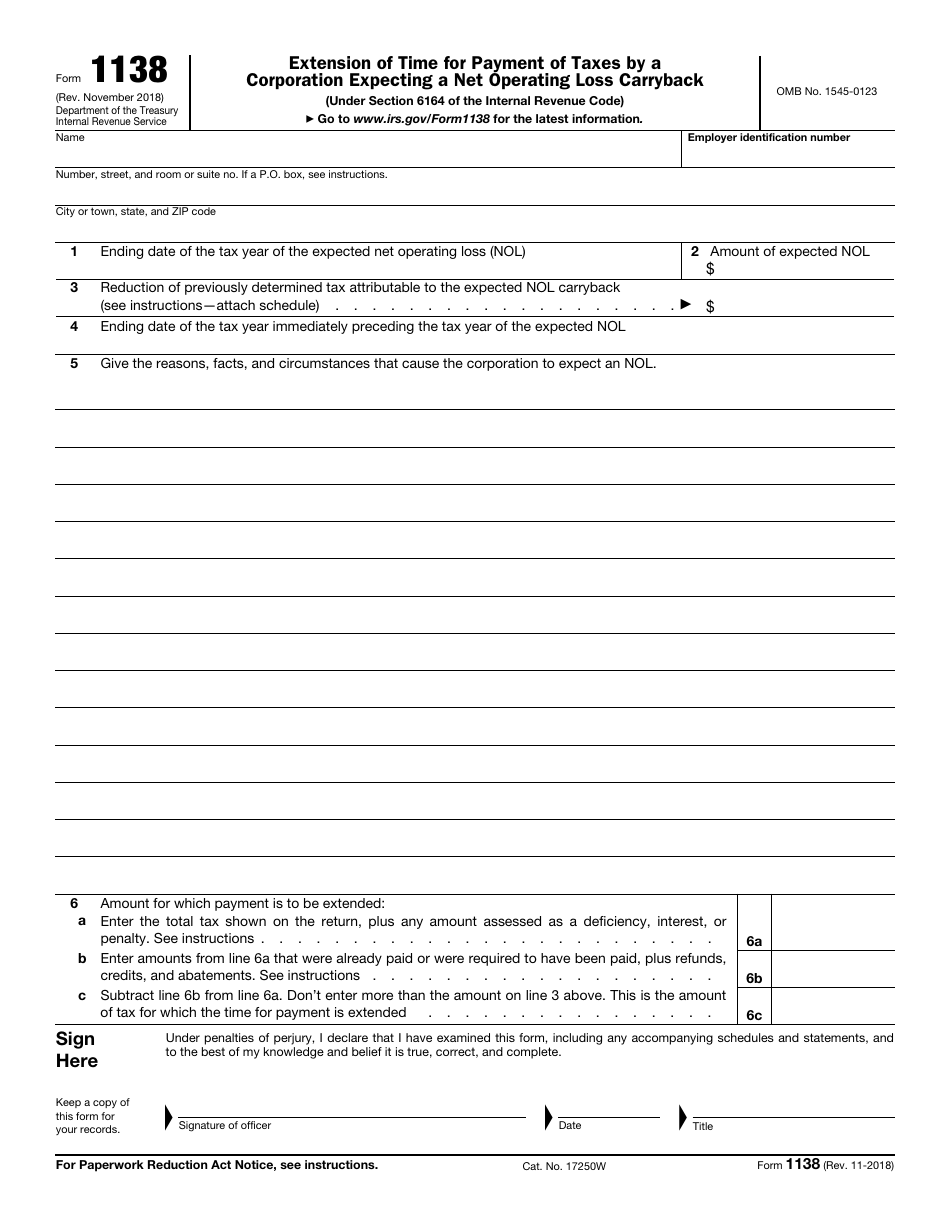

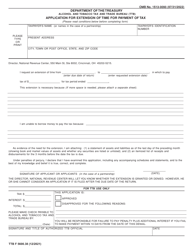

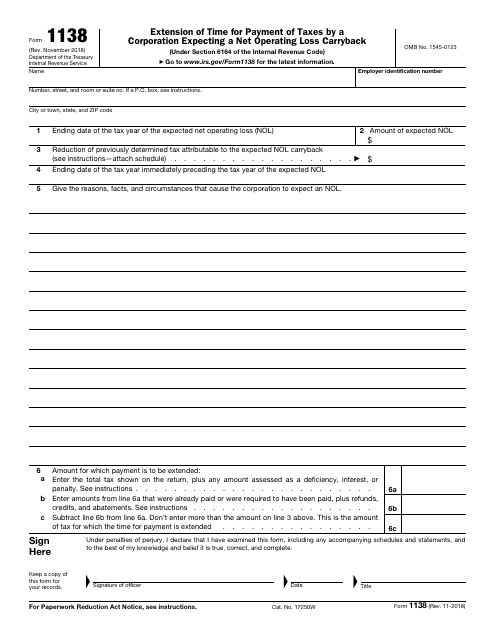

IRS Form 1138 Extension of Time for Payment of Taxes by a Corporation Expecting a Net Operating Loss Carryback

What Is IRS Form 1138?

This is a tax form that was released by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury on November 1, 2018. As of today, no separate filing guidelines for the form are provided by the IRS.

FAQ

Q: What is IRS Form 1138?

A: IRS Form 1138 is a form for corporations to request an extension of time for payment of taxes when expecting a net operating loss carryback.

Q: What is a net operating loss carryback?

A: A net operating loss carryback is a provision that allows corporations to apply their current year's losses to previous years' income, potentially resulting in a tax refund.

Q: Who can use IRS Form 1138?

A: Corporations expecting a net operating loss carryback can use IRS Form 1138 to request an extension of time for payment of taxes.

Q: What is the purpose of filing IRS Form 1138?

A: The purpose of filing IRS Form 1138 is to request additional time to pay taxes when a corporation anticipates receiving a tax refund due to a net operating loss carryback.

Q: How do I file IRS Form 1138?

A: To file IRS Form 1138, corporations must complete the form with the necessary information and submit it to the IRS for approval.

Form Details:

- A 2-page form available for download in PDF;

- Actual and valid for filing 2023 taxes;

- Editable, printable, and free;

- Fill out the form in our online filing application.

Download a fillable version of IRS Form 1138 through the link below or browse more documents in our library of IRS Forms.

Download IRS Form 1138 Extension of Time for Payment of Taxes by a Corporation Expecting a Net Operating Loss Carryback

1

2