![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1040 Schedule J

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1040 Schedule J

for the current year.

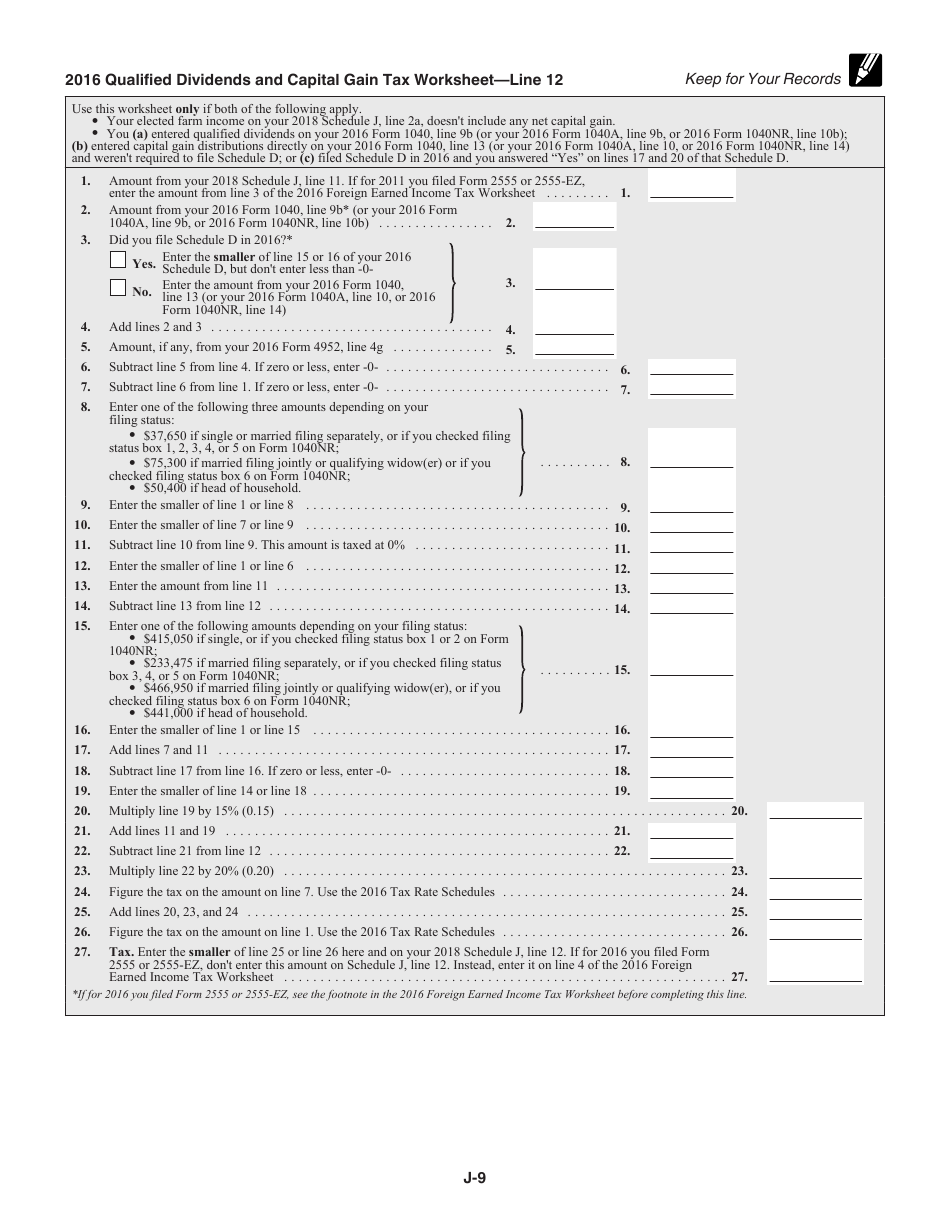

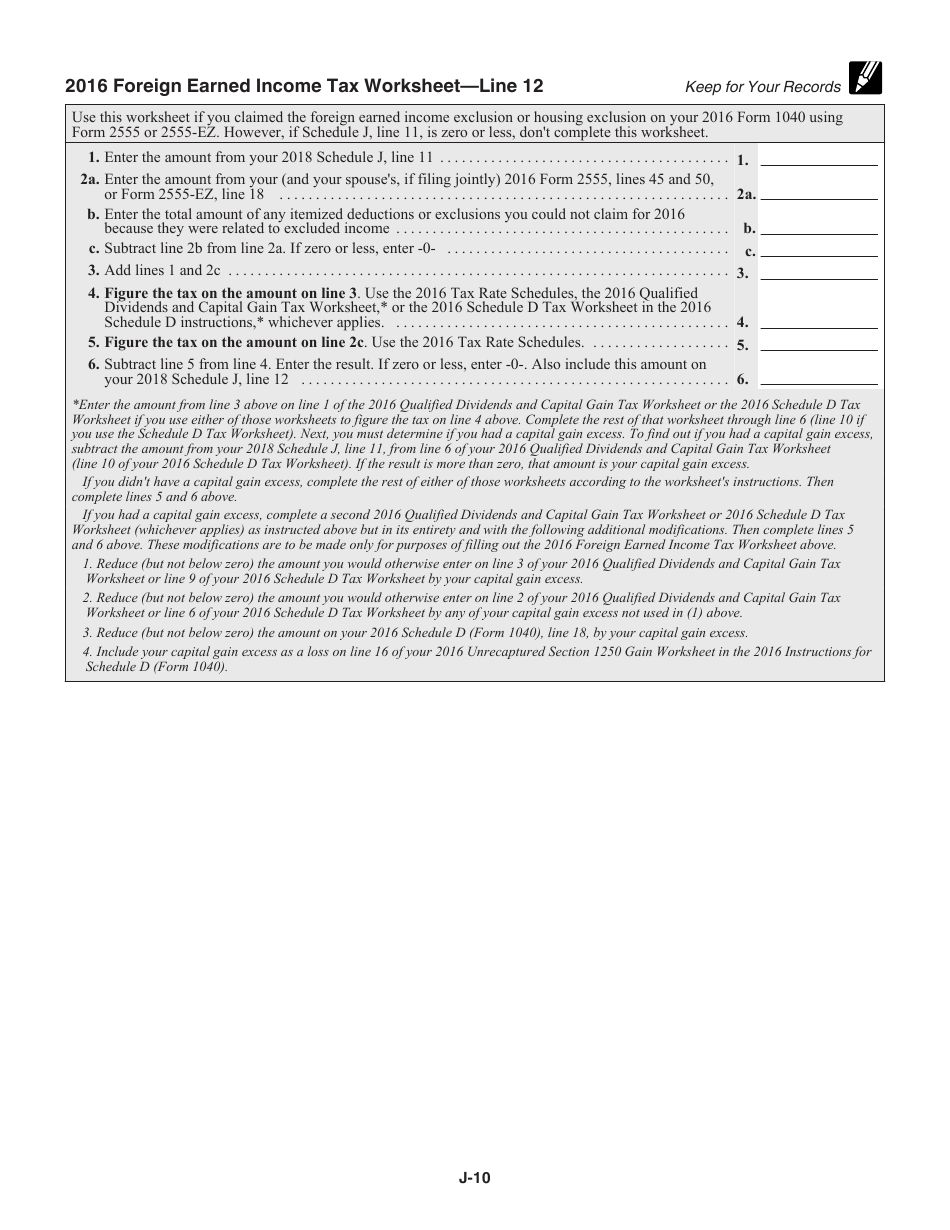

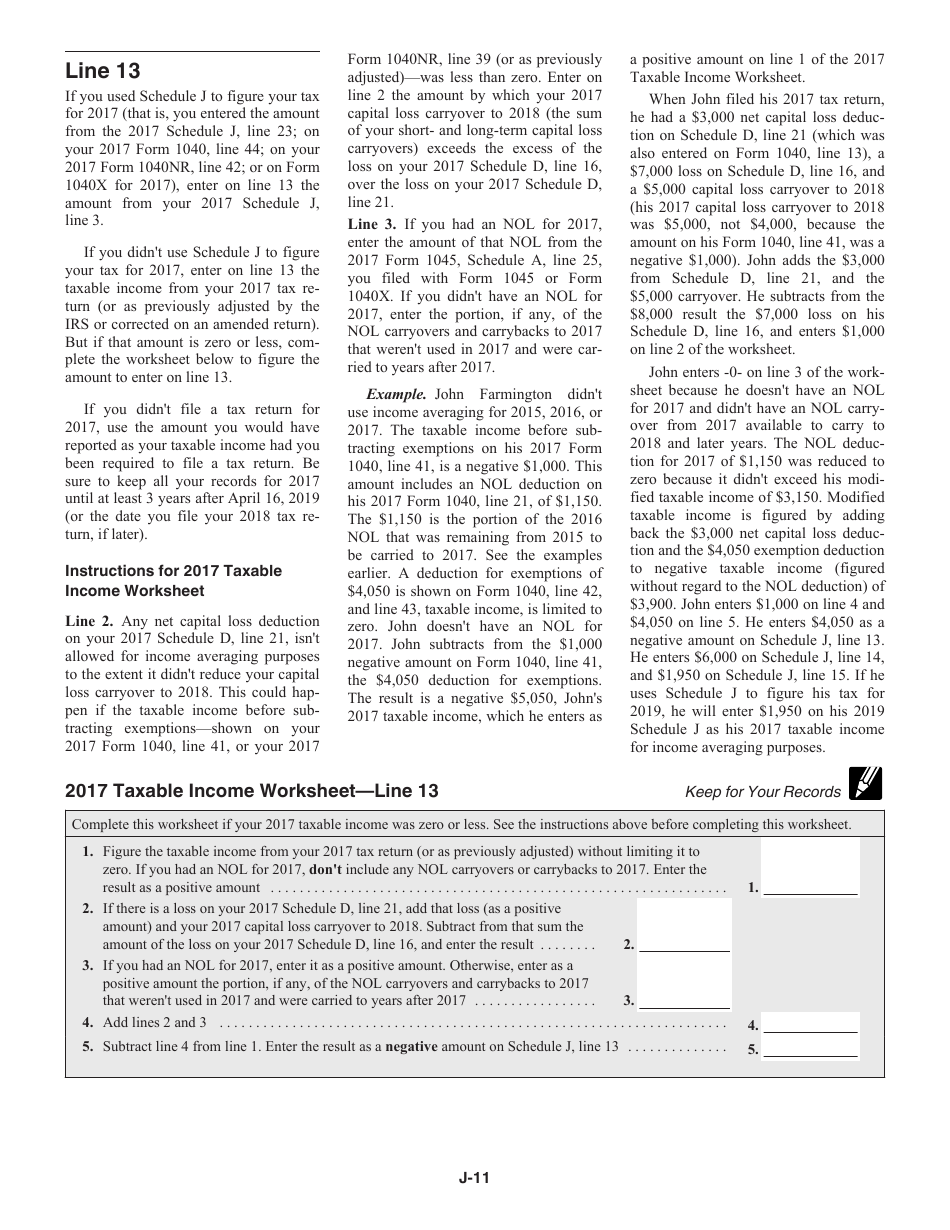

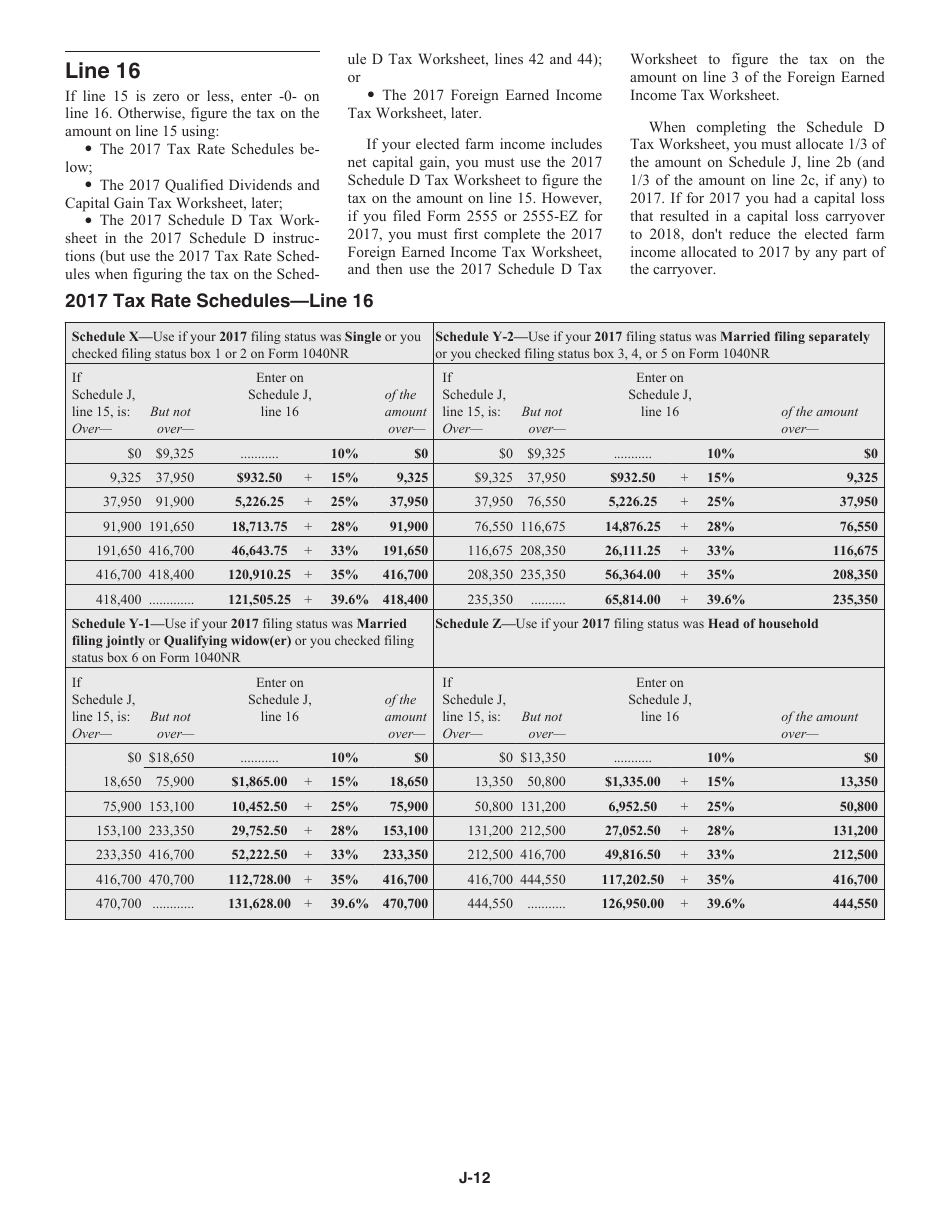

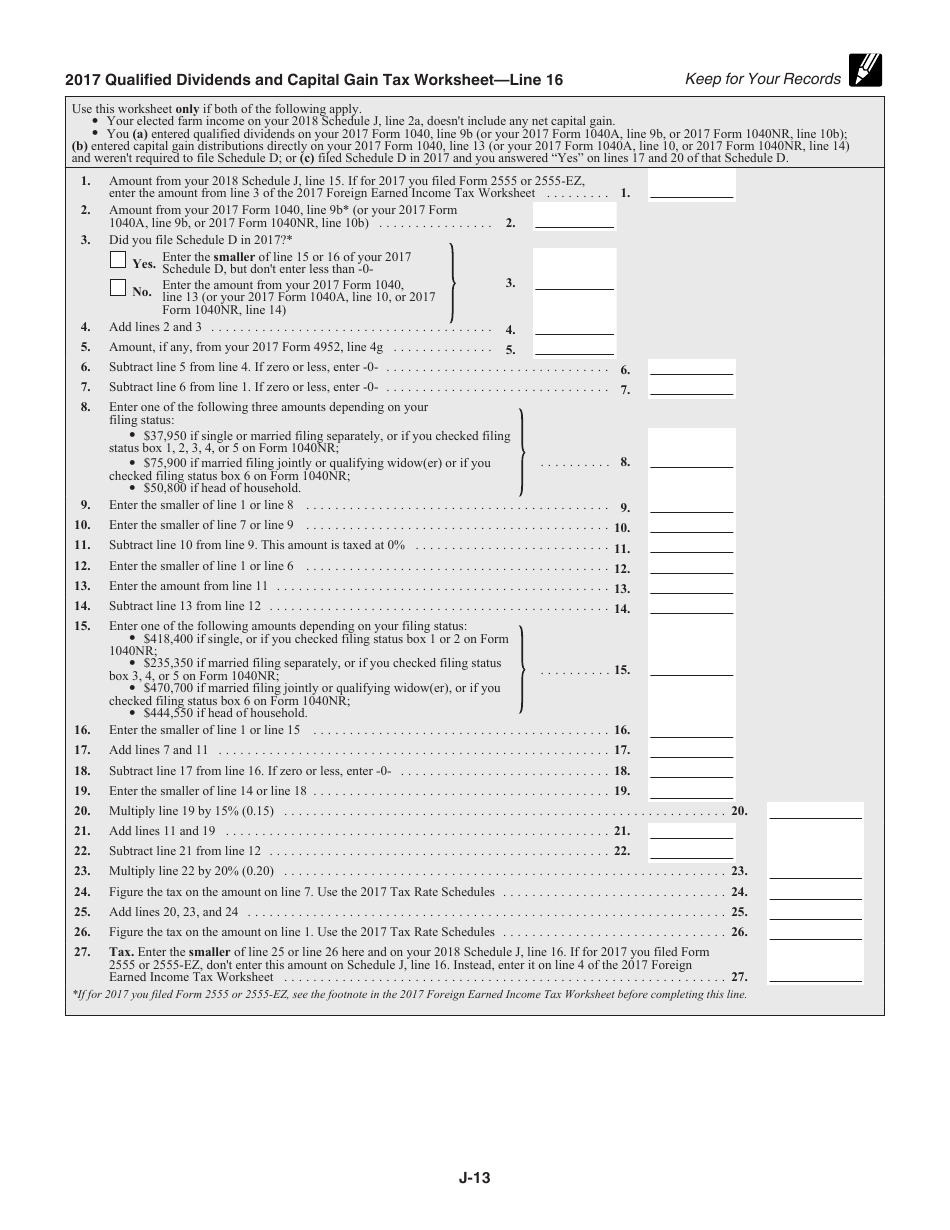

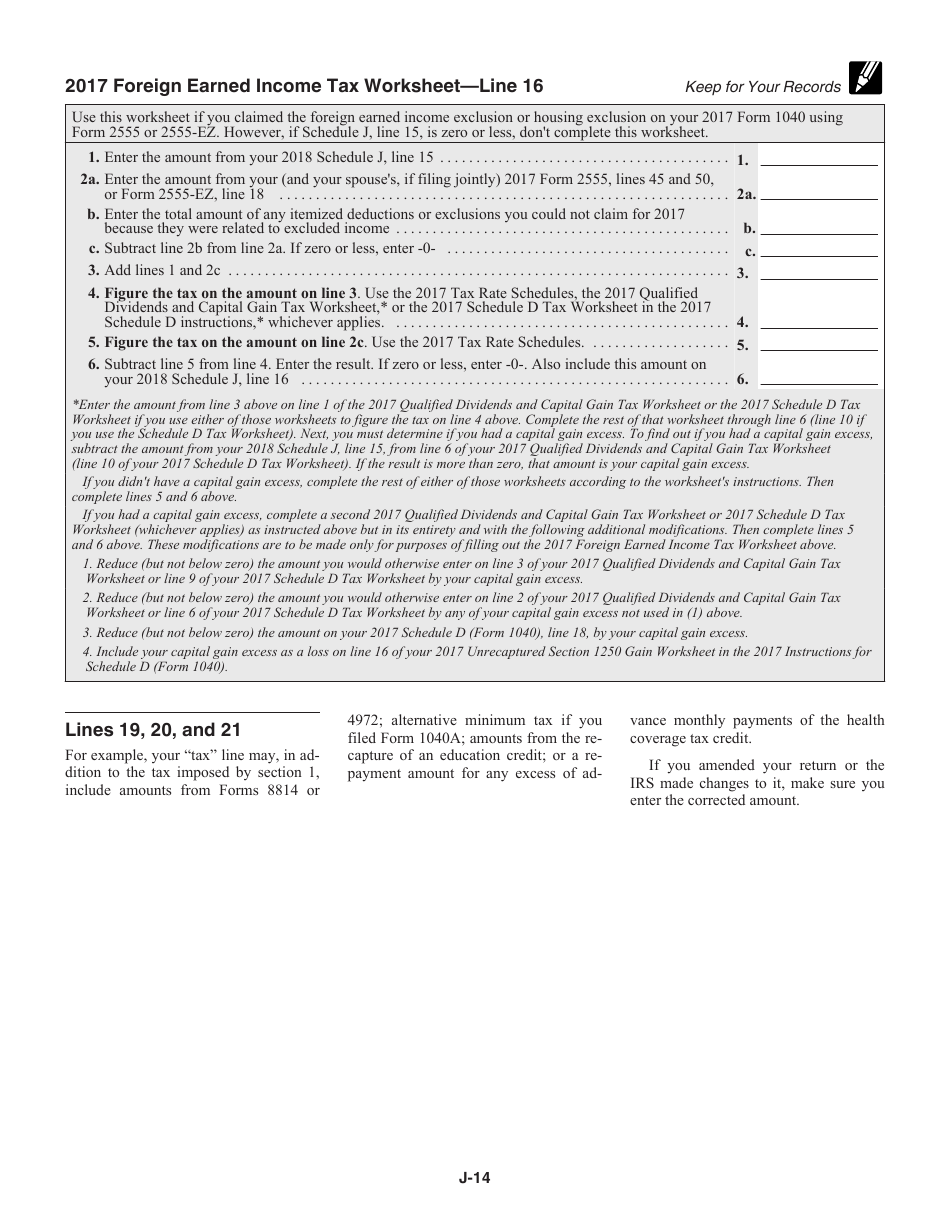

Instructions for IRS Form 1040 Schedule J Income Averaging for Farmers and Fishermen

This document contains official instructions for IRS Form 1040 Schedule J, Income Averaging for Farmers and Fishermen - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1040 Schedule J is available for download through this link.

FAQ

Q: What is IRS Form 1040 Schedule J?

A: IRS Form 1040 Schedule J is a tax form specifically for farmers and fishermen to average their income.

Q: Who can use IRS Form 1040 Schedule J?

A: Farmers and fishermen can use IRS Form 1040 Schedule J.

Q: What is income averaging?

A: Income averaging allows farmers and fishermen to spread out their income over several years, reducing their overall tax liability.

Q: Why would farmers and fishermen use income averaging?

A: Farmers and fishermen may use income averaging to account for fluctuations in their income from year to year.

Q: How does income averaging work?

A: Income averaging works by calculating the average income over a chosen period of time, and then taxing that average income instead of the actual income for each year.

Q: What is the benefit of income averaging?

A: The benefit of income averaging is that it can help reduce the tax burden for farmers and fishermen during years of high income.

Q: Are there any limitations or restrictions for income averaging?

A: Yes, there are limitations and restrictions for income averaging, such as specific eligibility requirements and certain income types that cannot be averaged.

Instruction Details:

- This 14-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 1040 Schedule J Income Averaging for Farmers and Fishermen

1

2

3

4

5

6

7

8

9

10

11

12

13

14