![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1118

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1118

for the current year.

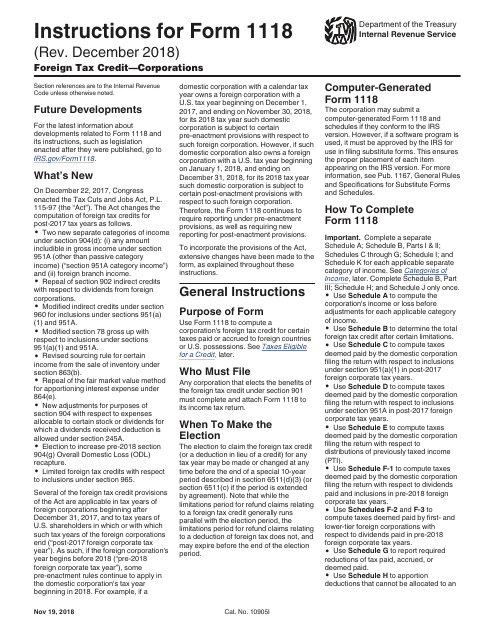

Instructions for IRS Form 1118 Foreign Tax Credit - Corporations

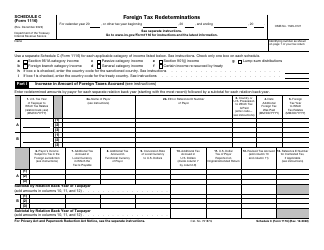

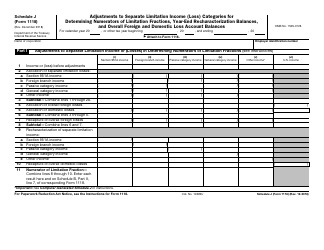

This document contains official instructions for IRS Form 1118 , Foreign Tax Credit - Corporations - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1118 Schedule J is available for download through this link.

FAQ

Q: What is IRS Form 1118?

A: IRS Form 1118 is a form that corporations use to claim a foreign tax credit.

Q: Who needs to file IRS Form 1118?

A: Corporations that are eligible to claim a foreign tax credit must file IRS Form 1118.

Q: What is the purpose of filing IRS Form 1118?

A: The purpose of filing IRS Form 1118 is to calculate and claim a credit for foreign taxes paid or accrued by a corporation.

Q: What information is required to complete IRS Form 1118?

A: To complete IRS Form 1118, you will need information about the amount of foreign taxes paid or accrued, as well as certain financial and ownership information.

Q: When is the deadline to file IRS Form 1118?

A: The deadline to file IRS Form 1118 is generally the same as the deadline for filing the corporation's income tax return. It is typically due on the 15th day of the 3rd month after the end of the corporation's tax year.

Q: Are there any penalties for not filing IRS Form 1118?

A: Yes, there can be penalties for failing to file IRS Form 1118 or for filing it incorrectly. It is important to ensure that the form is filed accurately and on time.

Q: Can I e-file IRS Form 1118?

A: No, currently IRS Form 1118 cannot be e-filed. It must be filed on paper and submitted through mail.

Q: Is there a separate IRS Form 1118 for individuals?

A: No, IRS Form 1118 is specifically for corporations. Individuals cannot use this form to claim a foreign tax credit.

Instruction Details:

- This 17-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17