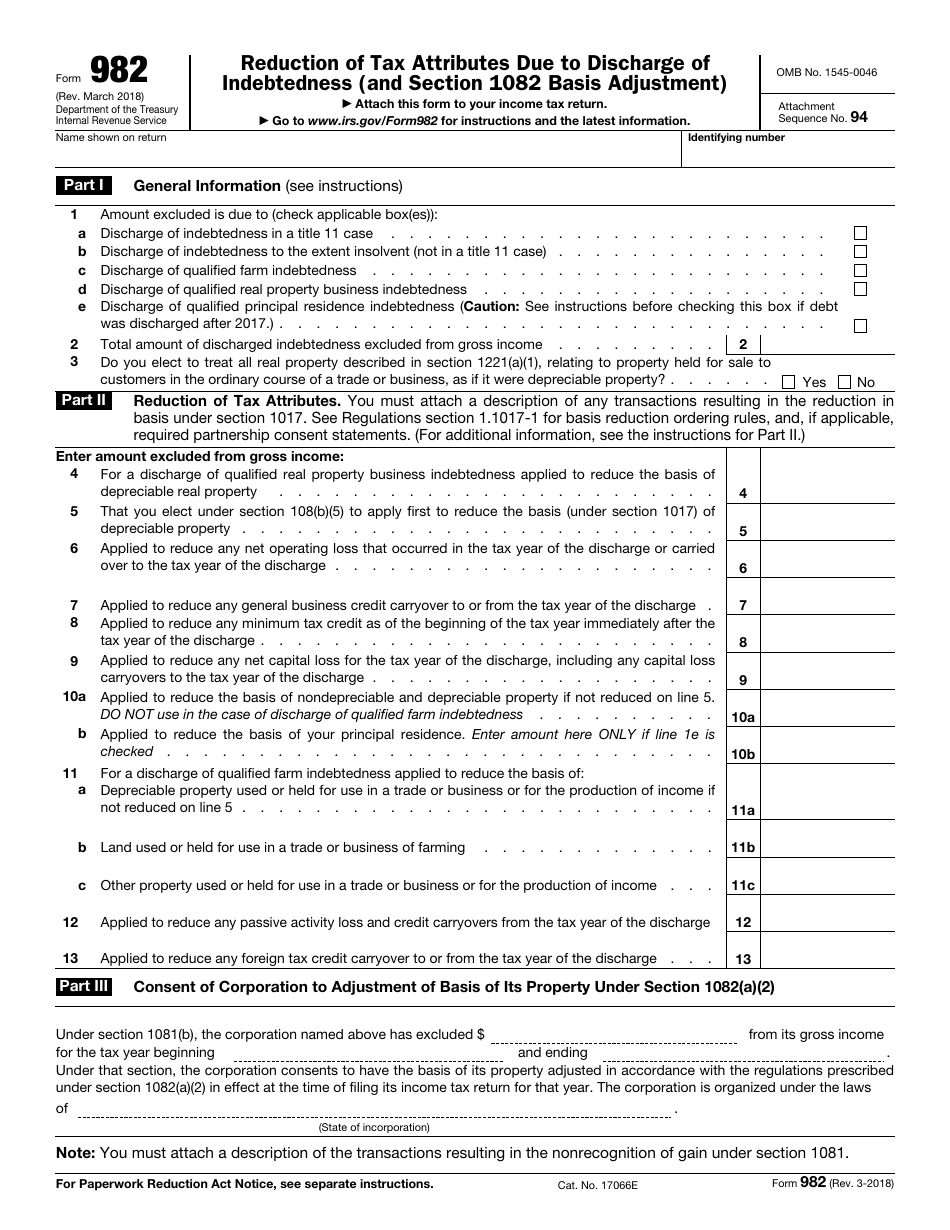

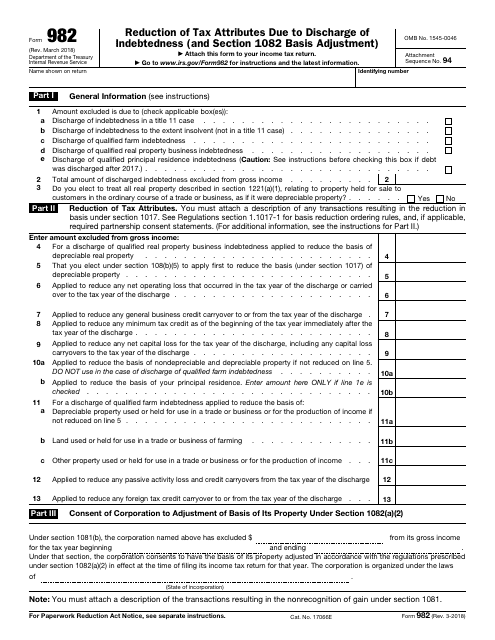

IRS Form 982 Reduction of Tax Attributes Due to Discharge of Indebtedness (And Section 1082 Basis Adjustment)

What Is IRS Form 982?

IRS Form 982, Reduction of Tax Attributes Due to Discharge of Indebtedness (and Section 1082 Basis Adjustment) , is a formal instrument used by taxpayers to explain to fiscal authorities why certain debts should not be taken into account as a part of their income.

Alternate Names:

- Form 982 Insolvency Worksheet;

- Tax Form 982.

If you believe you qualify for the exclusions outlined in the text of the form, you can postpone your tax obligations and prevent extra tax liability. Remember that the approved request will not imply the cancellation of debt or lack of responsibility to pay taxes - the calculations you include in the statement will simply delay the payments you will eventually have to deal with.

This document was released by the Internal Revenue Service (IRS) on March 1, 2018 , rendering previous editions of the form obsolete. You can download an IRS Form 982 fillable version through the link below.

When Must a Taxpayer Prepare Form 982?

Fill out and submit IRS Form 982 if you want to exclude certain debts from your income in order to lower your tax liability for a particular tax period. This option is only available for a few categories of taxpayers - you incurred debts conducting your farming business, your insolvency was formally recognized, or the debts accumulated because of you purchasing, building, or improving the place you reside in most of the time.

Ensure you comply with requirements established for taxpayers that are allowed to file this document and take advantage of economic benefits offered by tax organs - the discharge of indebtedness must take place before 2026 and you meet the threshold for taxpayers that describe indebtedness related to their main residential property ($750,000 or $375,000 if you are filing tax returns separately from your spouse).

Form 982 Instructions

Follow these Form 982 Instructions to figure out how much discharged indebtedness can be excluded from your income:

-

Write down your name and the taxpayer identification number . Note that the name you indicate in this document has to match the one listed on your tax return.

-

Specify the reason behind excluding the amount you later record in the form - you may confirm the discharge was approved by judicial authorities, took place during your insolvency, happened due to indebtedness directly connected to the farming trade, applied to lower the purchase price of the real estate that depreciated in value, or occurred because of indebtedness secured by the real property you use as your main residence. Enter the total amount of indebtedness and certify your decision to consider all real estate that will be sold to clients as assets eligible for depreciation treatment.

-

Clarify how tax attributes on Form 982 will be reduced . There are separate fields for various types of reduction - for instance, you have an opportunity to lower the carryover, reduce the basis of the land you utilize for your farming, or lower the depreciable assets' basis. Some taxpayers are entitled to claim a foreign tax credit imposed on them by foreign countries which also gives them the possibility to apply the reduction to the credit carryover.

-

Provide the consent of your entity to adjust the basis of your assets in line with current regulations and the conditions listed in writing . Indicate the amount excluded from your income, enter when the tax period began and ended, and record the state where your company was registered. Make sure you prepare and attach a separate statement that elaborates on operations that led to the basis reduction and lists the assets for which the basis was reduced. File this statement alongside your annual income statement that also covers the tax period described in the 982 Tax Form.

Where to Send IRS Form 982?

File IRS 982 when claiming your tax deductions and submitting your federal income tax return. Attach this form to your tax return documents and send them to the same address. Send it to the same address you sent the initial return even if you are filing this form later. The exact address depends on the state you live in. Find the full list of addresses on the IRS website.