![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 3800

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 3800

for the current year.

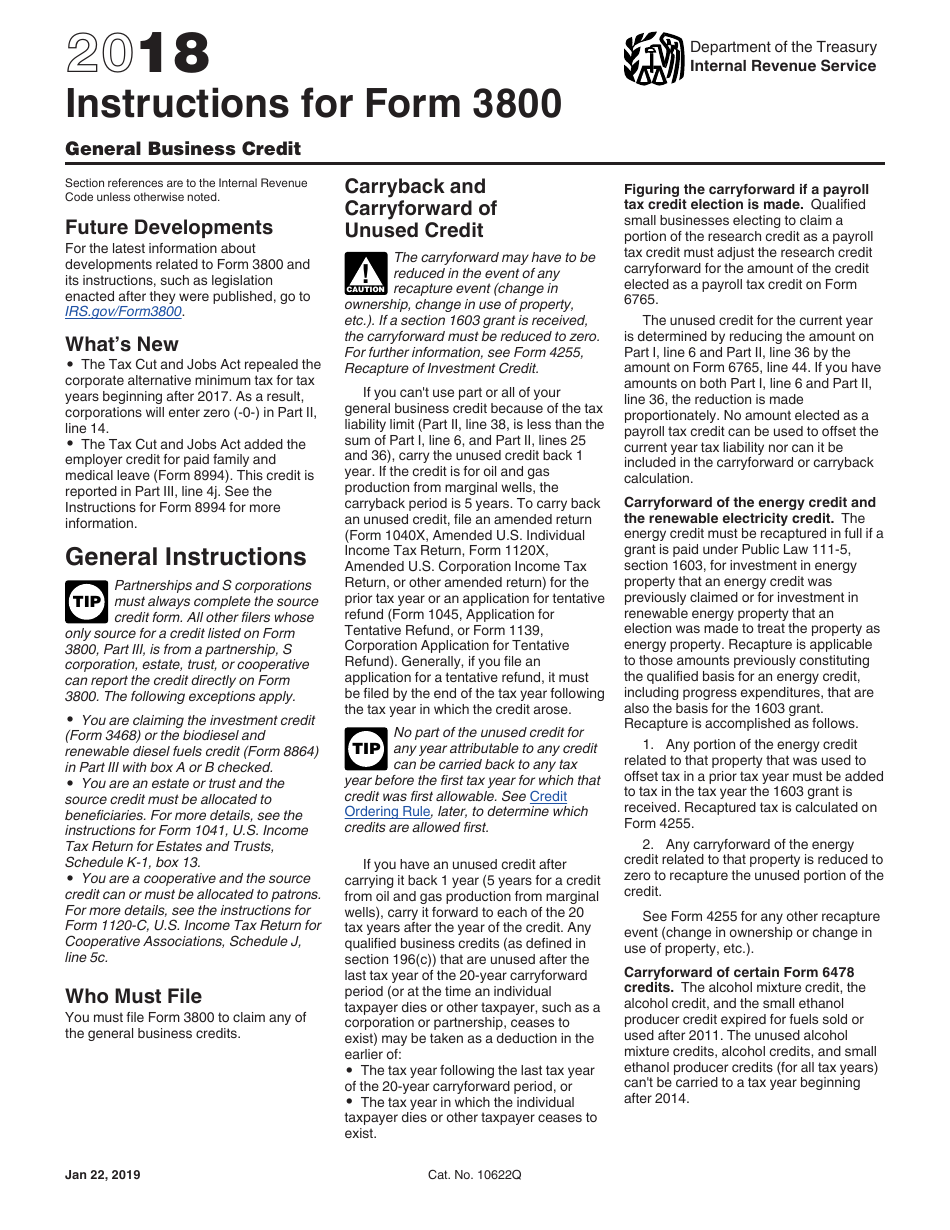

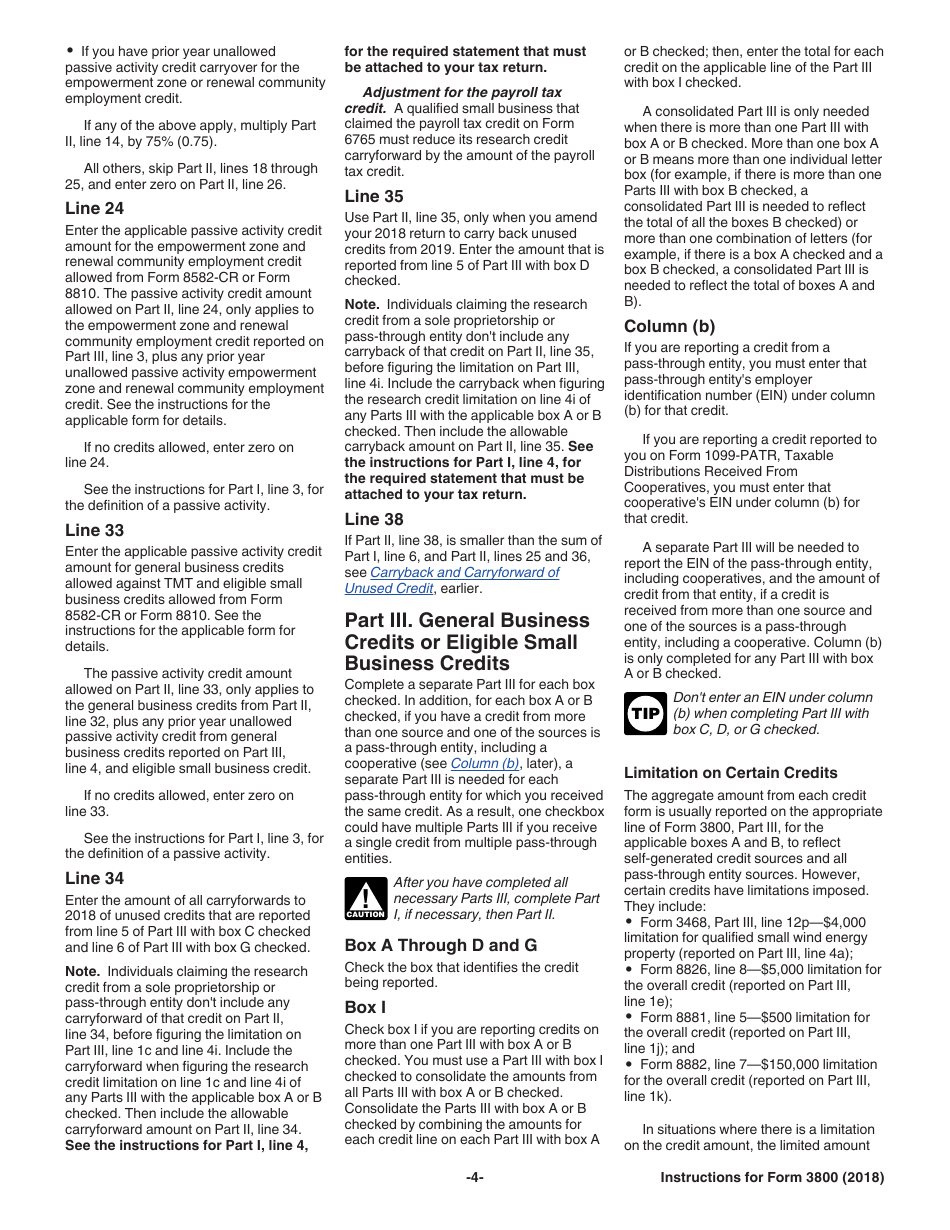

Instructions for IRS Form 3800 General Business Credit

This document contains official instructions for IRS Form 3800 , General Business Credit - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 3800 is available for download through this link.

FAQ

Q: What is IRS Form 3800?

A: IRS Form 3800 is the form used to claim the General Business Credit.

Q: What is the General Business Credit?

A: The General Business Credit is a tax credit that businesses can claim for various activities and expenses.

Q: Who can claim the General Business Credit?

A: Both individuals and businesses can claim the General Business Credit if they meet the eligibility requirements.

Q: What types of credits are included in the General Business Credit?

A: The General Business Credit includes several different credits, such as the Investment Credit and the Work Opportunity Credit.

Q: How do I fill out IRS Form 3800?

A: Filling out IRS Form 3800 requires gathering information about the specific credits you are claiming and calculating the credit amounts.

Q: When is the deadline to file IRS Form 3800?

A: The deadline to file IRS Form 3800 is usually the same as the deadline to file your annual tax return.

Q: Can I claim the General Business Credit if I am self-employed?

A: Yes, self-employed individuals can claim the General Business Credit if they meet the eligibility requirements.

Q: What documentation do I need to support my General Business Credit claim?

A: You should keep all relevant documentation, such as receipts and records, to support your General Business Credit claim in case of an IRS audit.

Q: Can I carry forward unused General Business Credit?

A: Yes, unused General Business Credit can be carried forward to future tax years.

Instruction Details:

- This 6-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5

6