![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8804 Schedule A

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8804 Schedule A

for the current year.

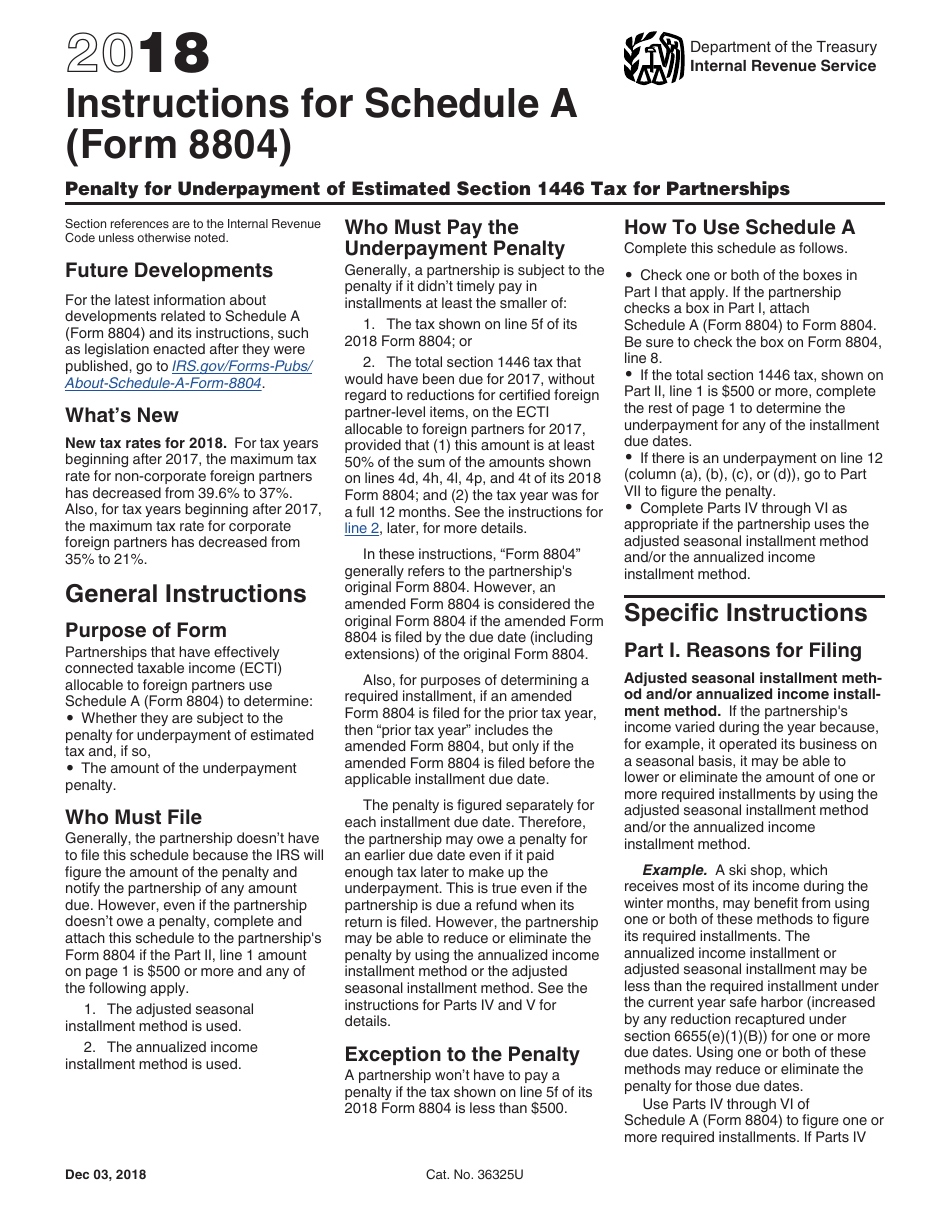

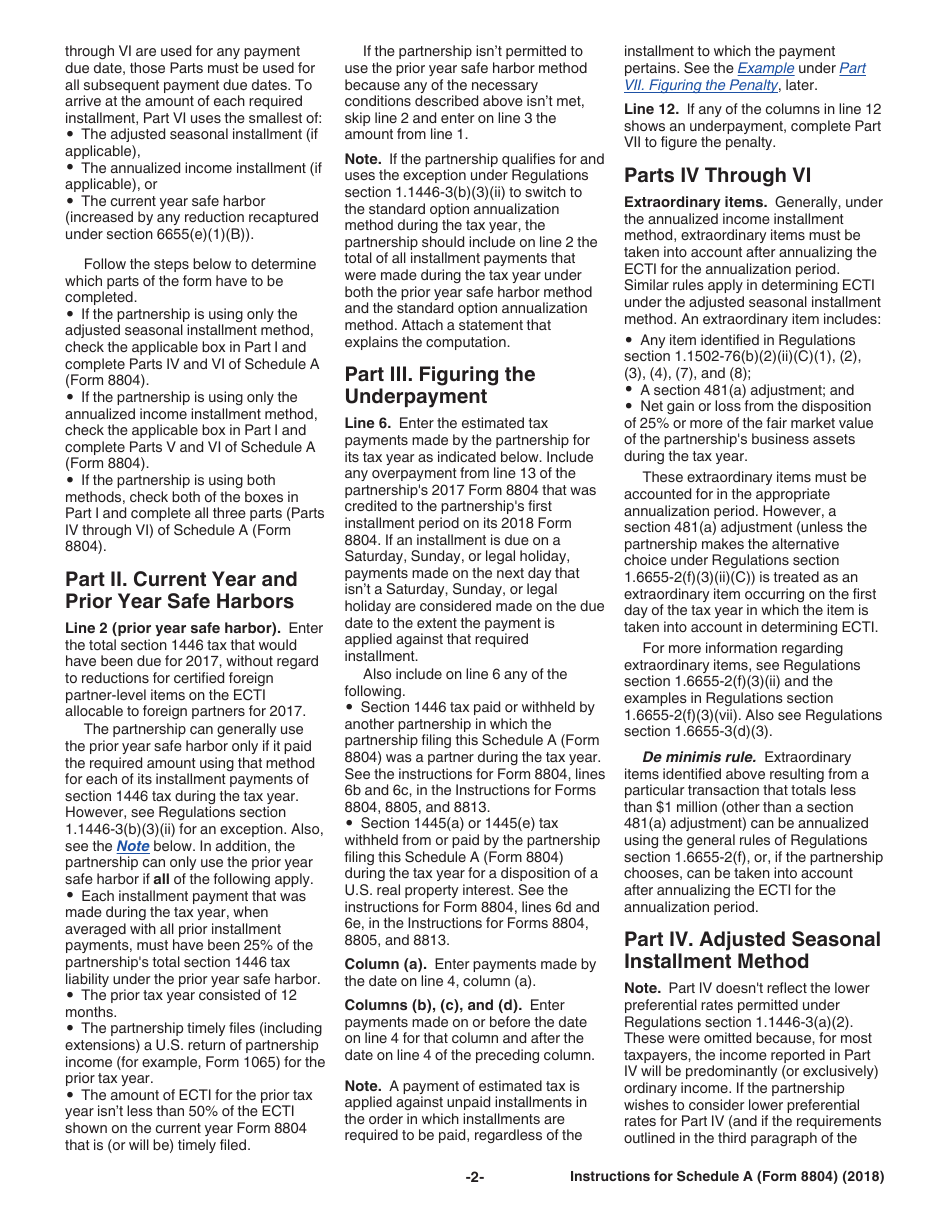

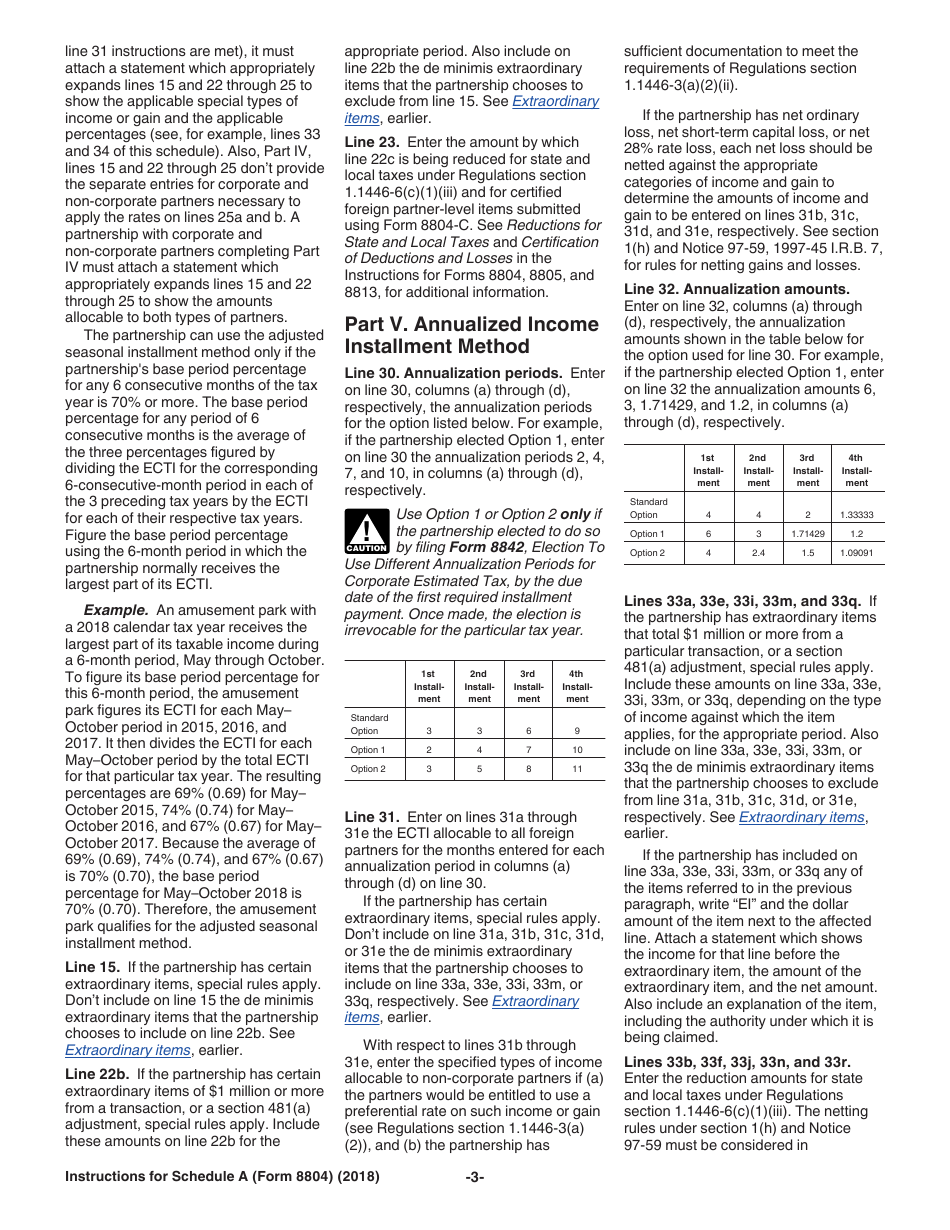

Instructions for IRS Form 8804 Schedule A Penalty for Underpayment of Estimated Section 1446 Tax for Partnerships

This document contains official instructions for IRS Form 8804 Schedule A, Penalty for Underpayment of Estimated Section 1446 Tax for Partnerships - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8804 Schedule A is available for download through this link.

FAQ

Q: What is IRS Form 8804 Schedule A?

A: IRS Form 8804 Schedule A is a form used by partnerships to report the penalty for underpayment of estimated Section 1446 tax.

Q: What is the penalty for underpayment of estimated Section 1446 tax?

A: The penalty for underpayment of estimated Section 1446 tax is a penalty imposed on partnerships that fail to pay the required estimated tax on time.

Q: Who uses IRS Form 8804 Schedule A?

A: Partnerships use IRS Form 8804 Schedule A.

Q: What is Section 1446 tax?

A: Section 1446 tax refers to the withholding tax imposed on foreign partners in a partnership.

Q: What information is required on IRS Form 8804 Schedule A?

A: IRS Form 8804 Schedule A requires the partnership to calculate and report the penalty amount based on underpayment of estimated Section 1446 tax.

Q: Is IRS Form 8804 Schedule A mandatory for all partnerships?

A: No, IRS Form 8804 Schedule A is only required for partnerships that have underpaid the estimated Section 1446 tax.

Q: What happens if a partnership fails to file IRS Form 8804 Schedule A?

A: If a partnership fails to file IRS Form 8804 Schedule A, they may be subject to penalties and interest on the underpayment of estimated Section 1446 tax.

Q: What is the deadline for filing IRS Form 8804 Schedule A?

A: The deadline for filing IRS Form 8804 Schedule A is typically the same as the deadline for filing the partnership's tax return, which is usually March 15th.

Instruction Details:

- This 4-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 8804 Schedule A Penalty for Underpayment of Estimated Section 1446 Tax for Partnerships

1

2

3

4