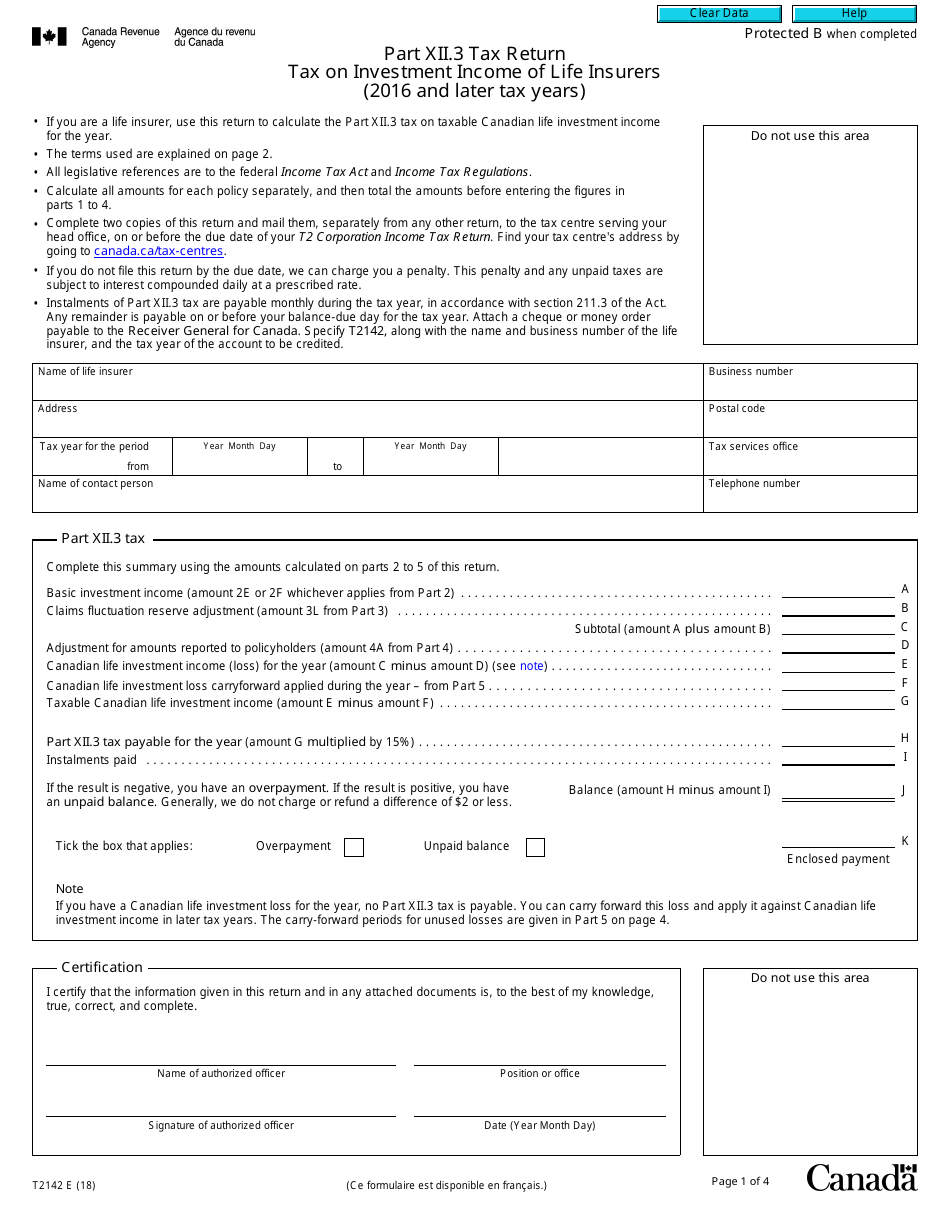

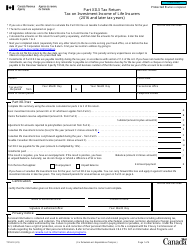

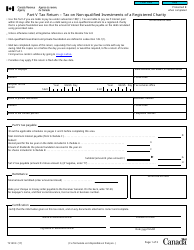

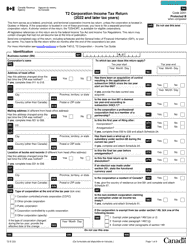

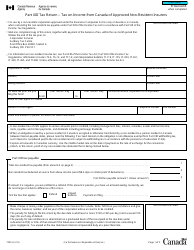

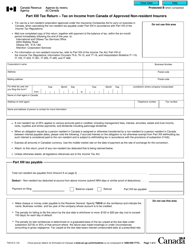

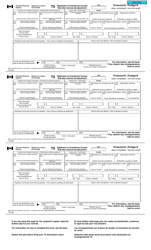

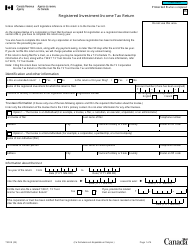

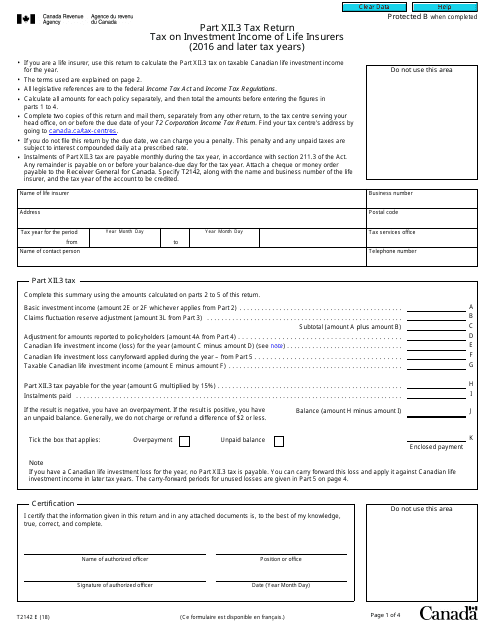

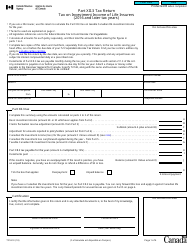

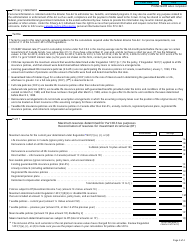

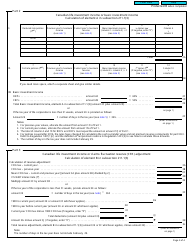

Form T2142 Part XII.3 Tax Return Tax on Investment Income of Life Insurers (2016 and Later Tax Years) - Canada

Fill PDF Online

Fill out online for free

without registration or credit card

Form T2142 or the "Form T2142 Part Xii.3 "tax Return Tax On Investment Income Of Life Insurers (2016 And Later Tax Years)" - Canada" is a form issued by the Canadian Revenue Agency .

Download a PDF version of the Form T2142 down below or find it on the Canadian Revenue Agency Forms website.

Download Form T2142 Part XII.3 Tax Return Tax on Investment Income of Life Insurers (2016 and Later Tax Years) - Canada

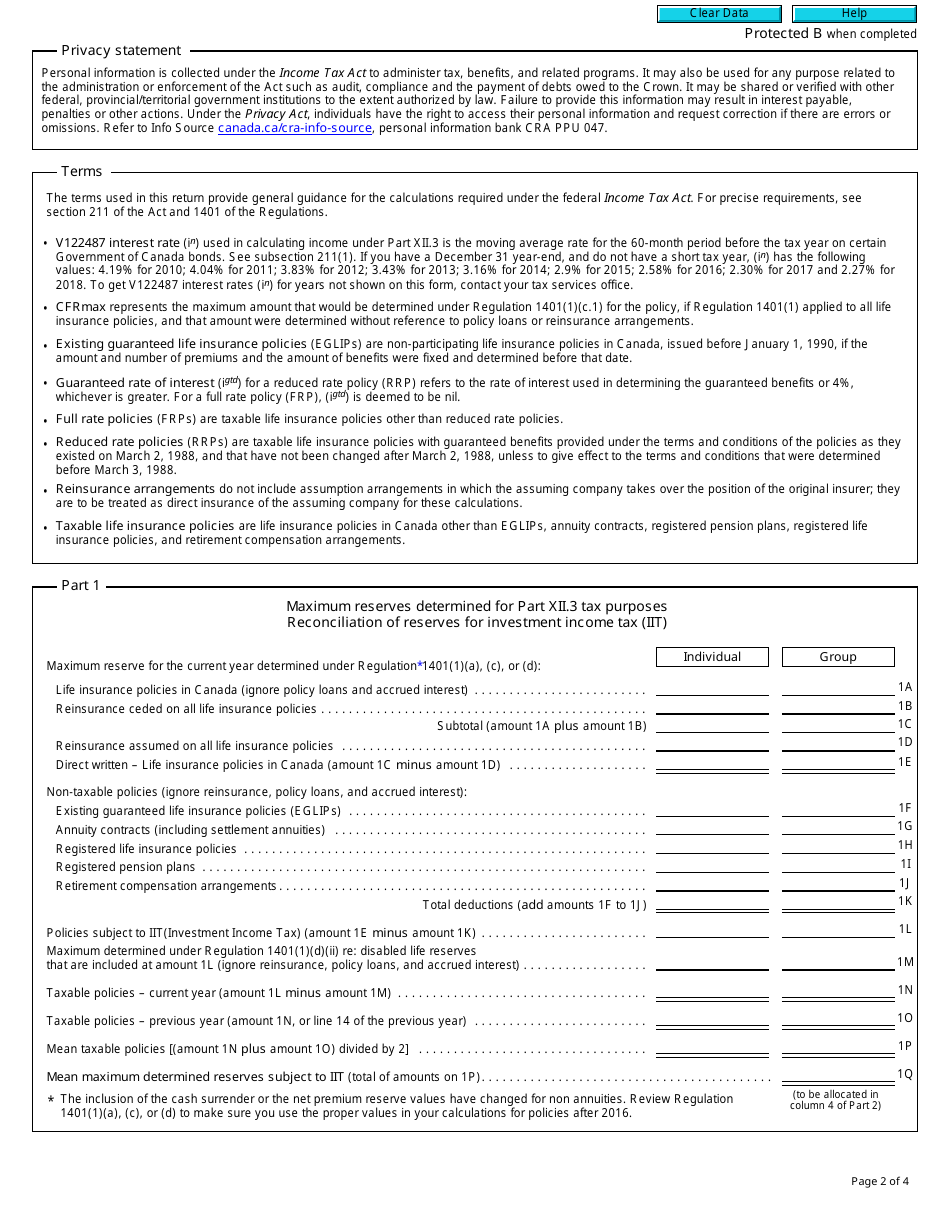

1

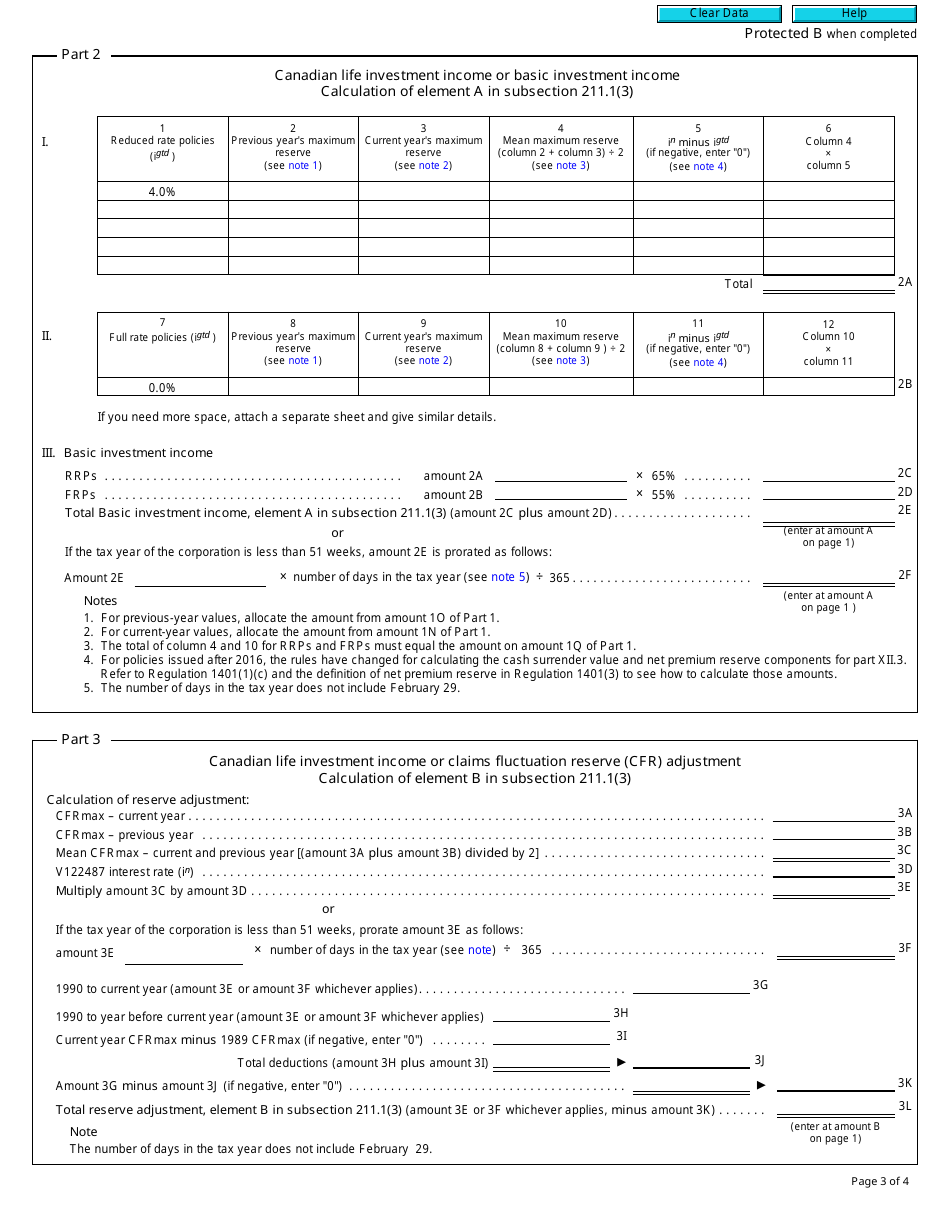

2

3

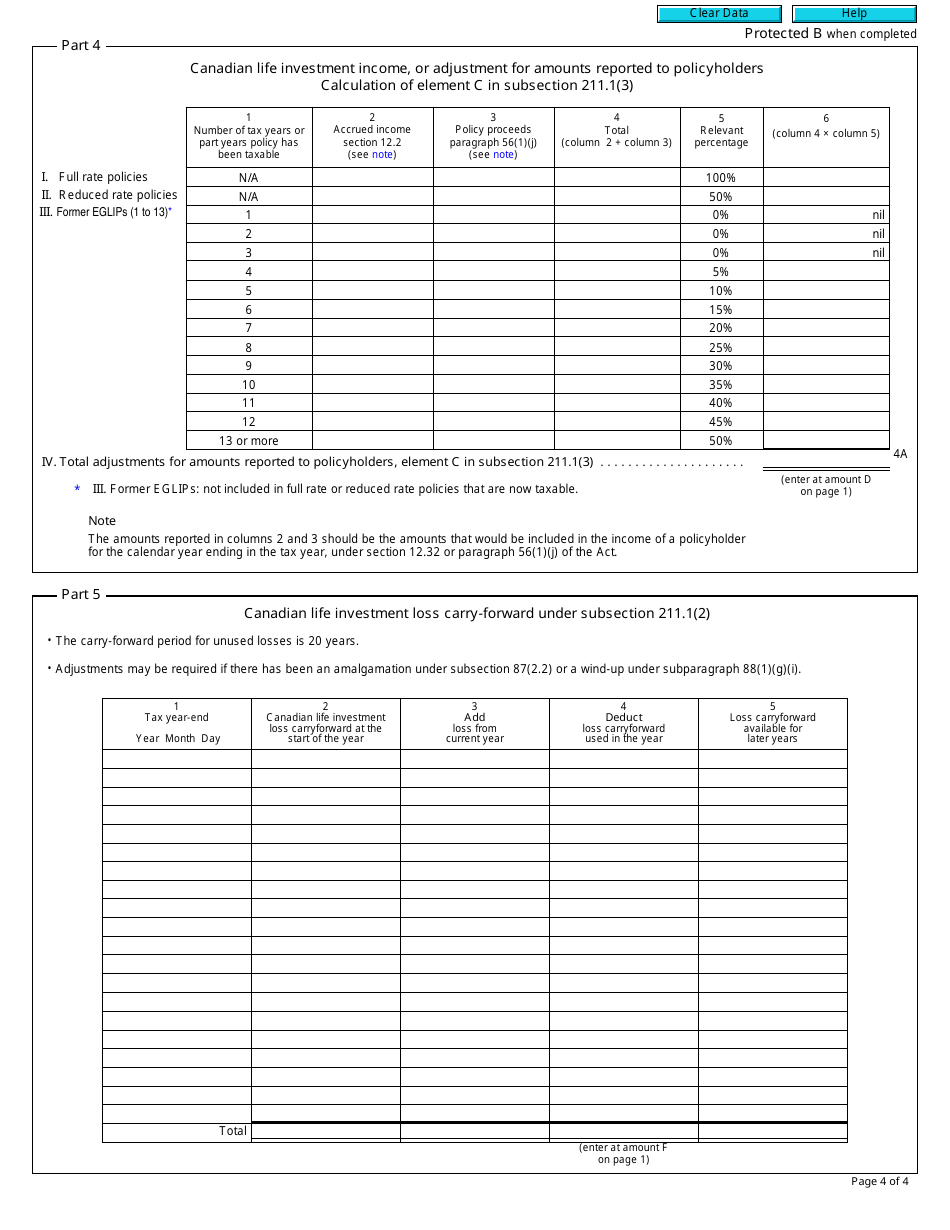

4