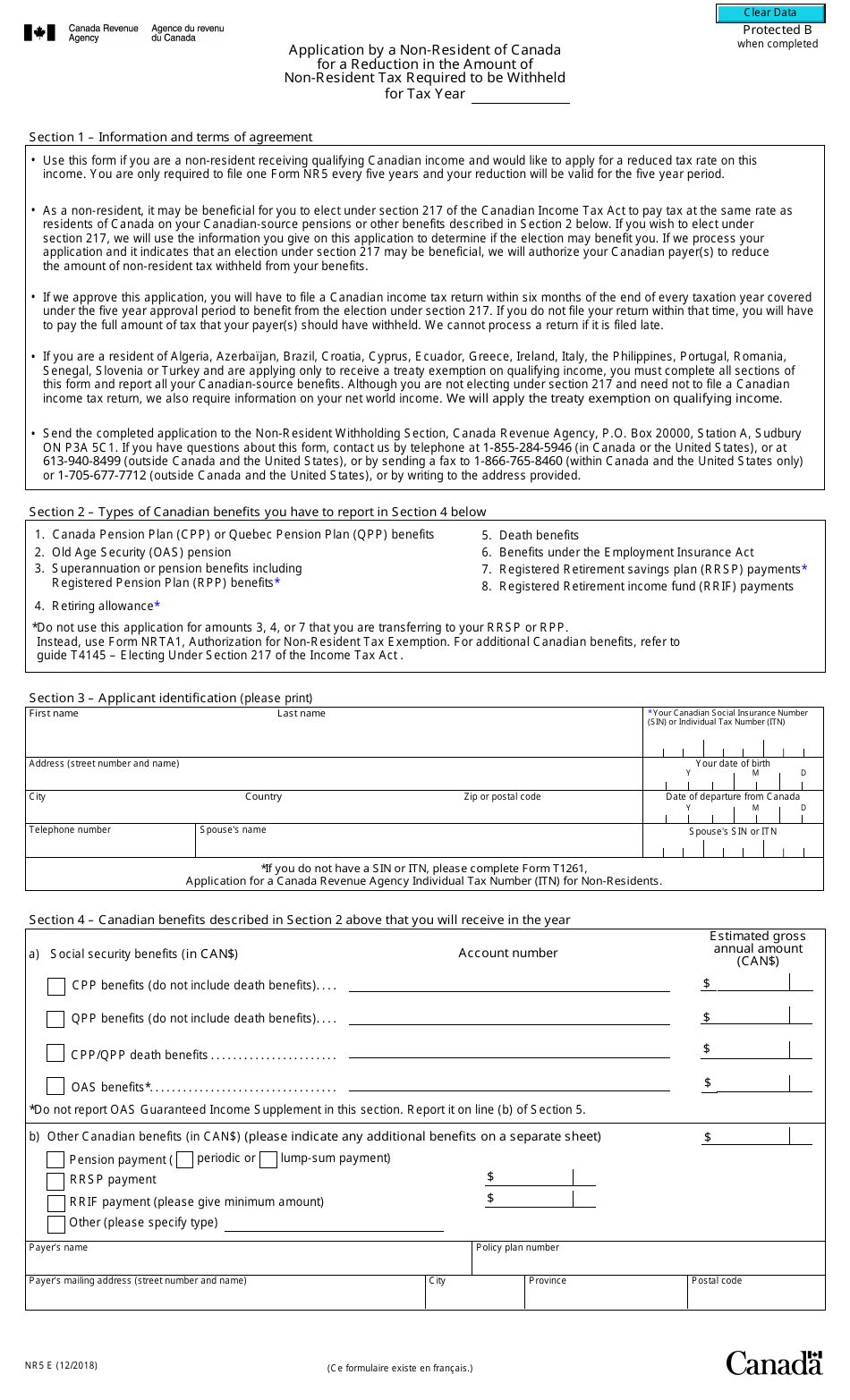

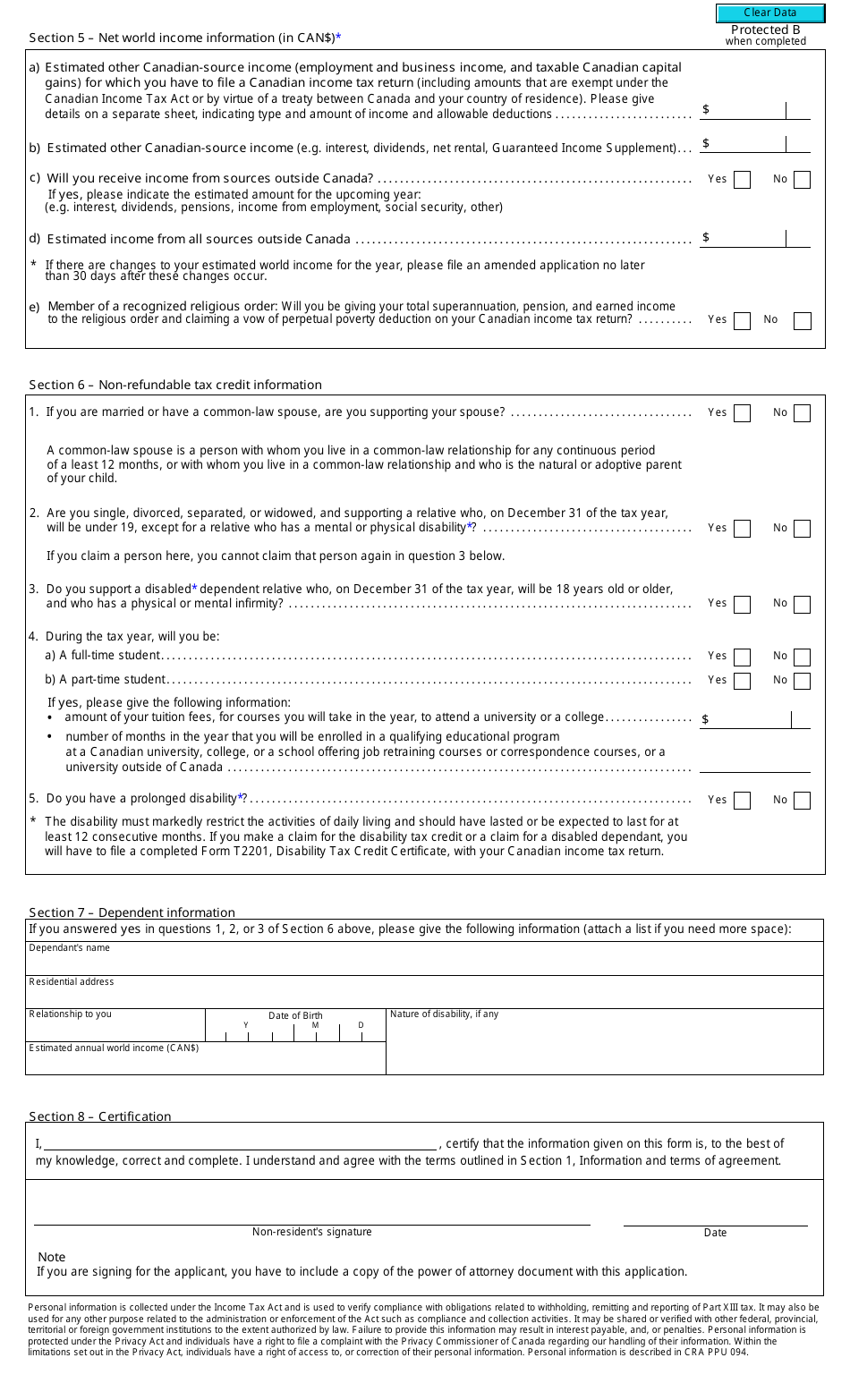

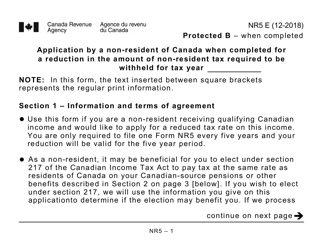

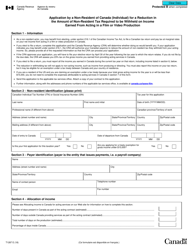

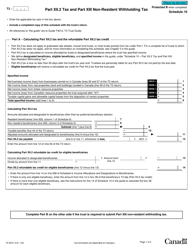

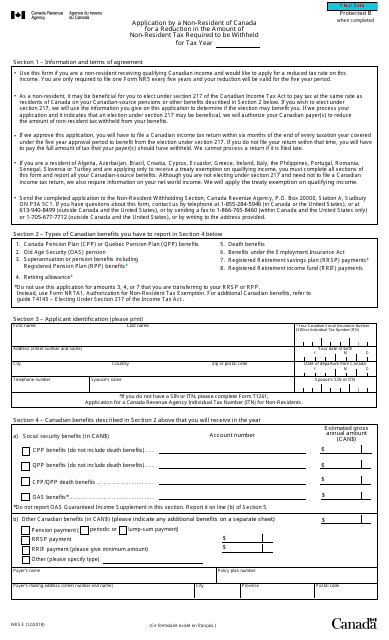

Form NR5 Application by a Non-resident of Canada for a Reduction in the Amount of Non-resident Tax Required to Be Withheld for Tax Year - Canada

Form NR5 is used by non-residents of Canada who want to apply for a reduction in the amount of non-resident tax required to be withheld for the tax year. This reduction is based on a tax treaty between Canada and the non-resident's country of residence. By submitting Form NR5, non-residents can potentially have less tax withheld from their Canadian income.

The non-resident of Canada files the Form NR5 application.

FAQ

Q: What is Form NR5?

A: Form NR5 is an application by a non-resident of Canada for a reduction in the amount of non-resident tax required to be withheld for tax year.

Q: Who can use Form NR5?

A: Non-residents of Canada can use Form NR5 to apply for a reduction in the amount of non-resident tax withholding.

Q: What is the purpose of Form NR5?

A: The purpose of Form NR5 is to reduce the amount of non-resident tax required to be withheld from income earned in Canada by non-residents.

Q: What information is required on Form NR5?

A: Form NR5 requires information such as the taxpayer's name, address, country of residence, and details about the income to be earned in Canada.

Q: Is there a deadline for submitting Form NR5?

A: Yes, Form NR5 should be submitted to the CRA before the first payment of income subject to non-resident tax withholding is made.

Q: Can Form NR5 be used for multiple tax years?

A: No, a separate Form NR5 must be submitted for each tax year.

Q: What happens after submitting Form NR5?

A: The CRA will review the application and determine the amount of non-resident tax withholding to be reduced.

Q: Are there any exemptions from non-resident tax withholding?

A: Yes, certain exemptions may apply depending on the taxpayer's country of residence and the type of income being earned in Canada. Form NR5 can be used to claim these exemptions.

Download Form NR5 Application by a Non-resident of Canada for a Reduction in the Amount of Non-resident Tax Required to Be Withheld for Tax Year - Canada

1

2