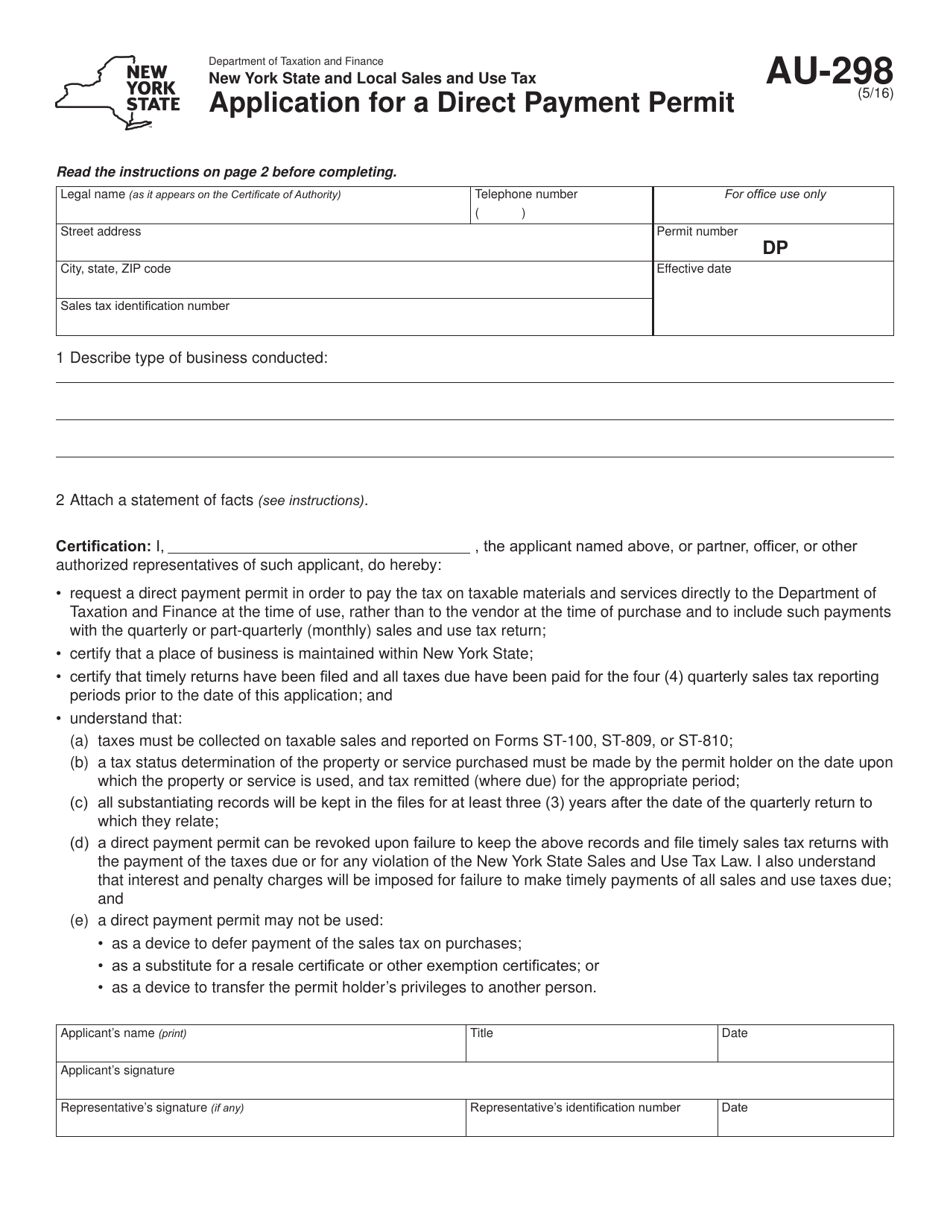

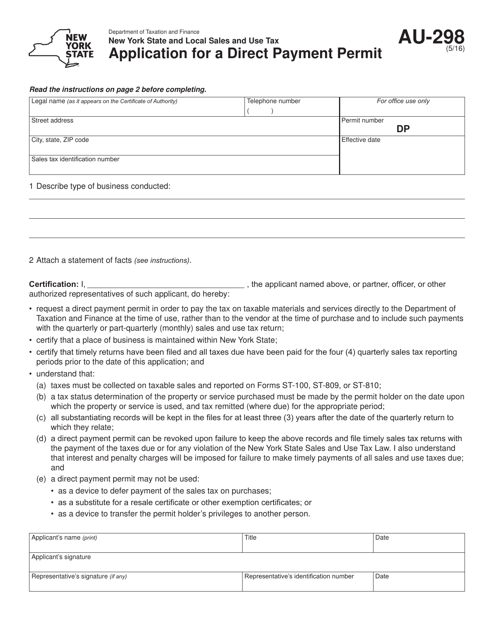

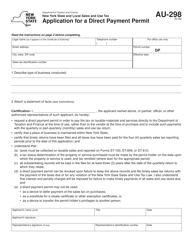

Form AU-298 Application for a Direct Payment Permit - New York

What Is Form AU-298?

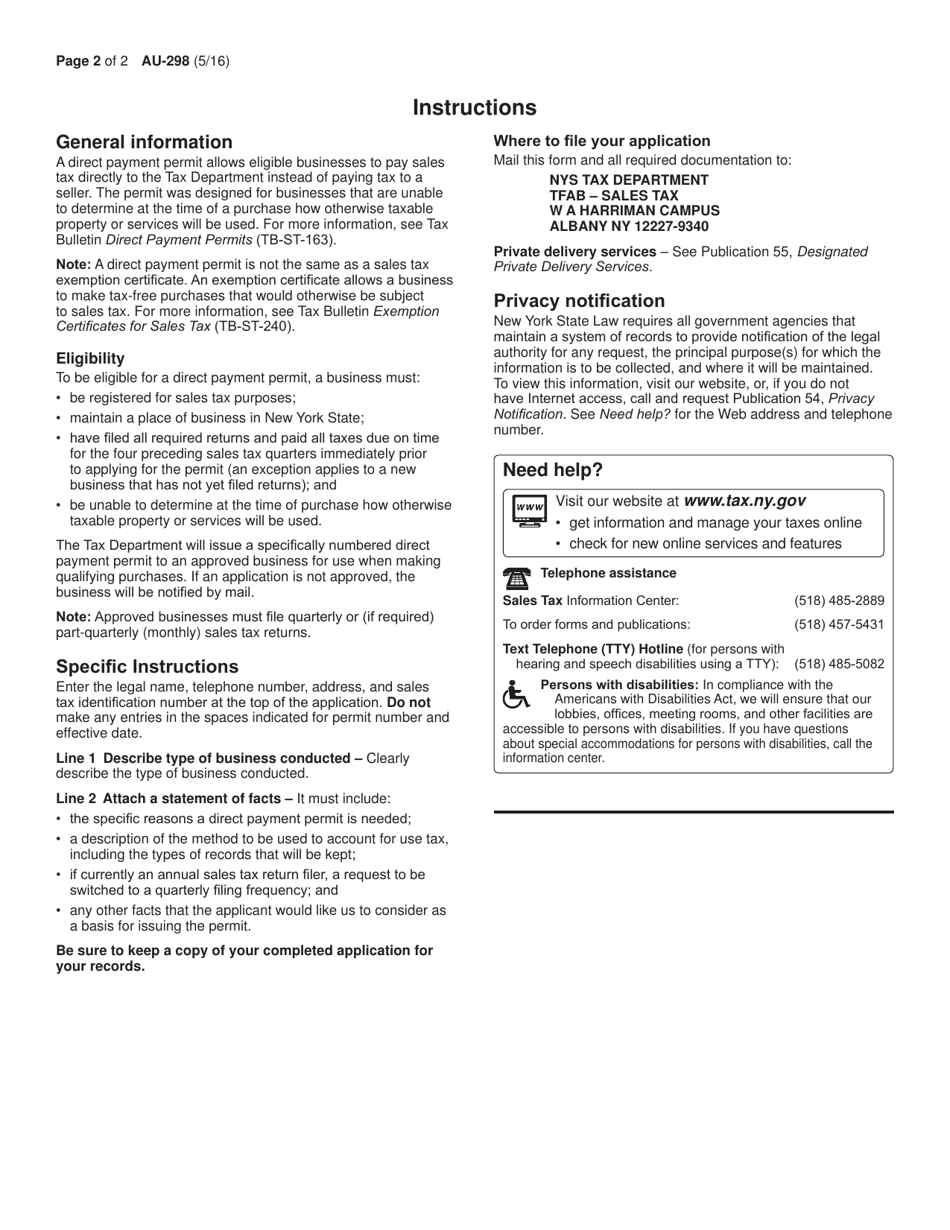

This is a legal form that was released by the New York State Department of Taxation and Finance - a government authority operating within New York. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is form AU-298?

A: Form AU-298 is the Application for a Direct Payment Permit in New York.

Q: What is a Direct Payment Permit?

A: A Direct Payment Permit is a permit that allows businesses to pay sales tax directly to the New York State Department of Taxation and Finance, instead of paying it to their vendors.

Q: Who is eligible to apply for a Direct Payment Permit?

A: Businesses that make frequent purchases of taxable property or services for their own use or consumption, and have a good compliance record, may be eligible to apply for a Direct Payment Permit.

Q: What are the benefits of having a Direct Payment Permit?

A: Having a Direct Payment Permit allows businesses to directly pay sales tax to the state, which can simplify the reporting and payment process. It also ensures that the businesses can claim credit or refund for the tax paid on purchases.

Q: Is there a fee for applying for a Direct Payment Permit?

A: No, there is no fee for applying for a Direct Payment Permit.

Q: How long does it take to receive a Direct Payment Permit?

A: The processing time for Direct Payment Permit applications can vary, but it generally takes several weeks to receive a permit.

Q: Are there any obligations or requirements for businesses with a Direct Payment Permit?

A: Yes, businesses with a Direct Payment Permit are required to keep detailed records of their purchases and report their sales and use tax liabilities accurately.

Form Details:

- Released on May 1, 2016;

- The latest edition provided by the New York State Department of Taxation and Finance;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form AU-298 by clicking the link below or browse more documents and templates provided by the New York State Department of Taxation and Finance.

Download Form AU-298 Application for a Direct Payment Permit - New York

1

2