![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form R-210NRA

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form R-210NRA

for the current year.

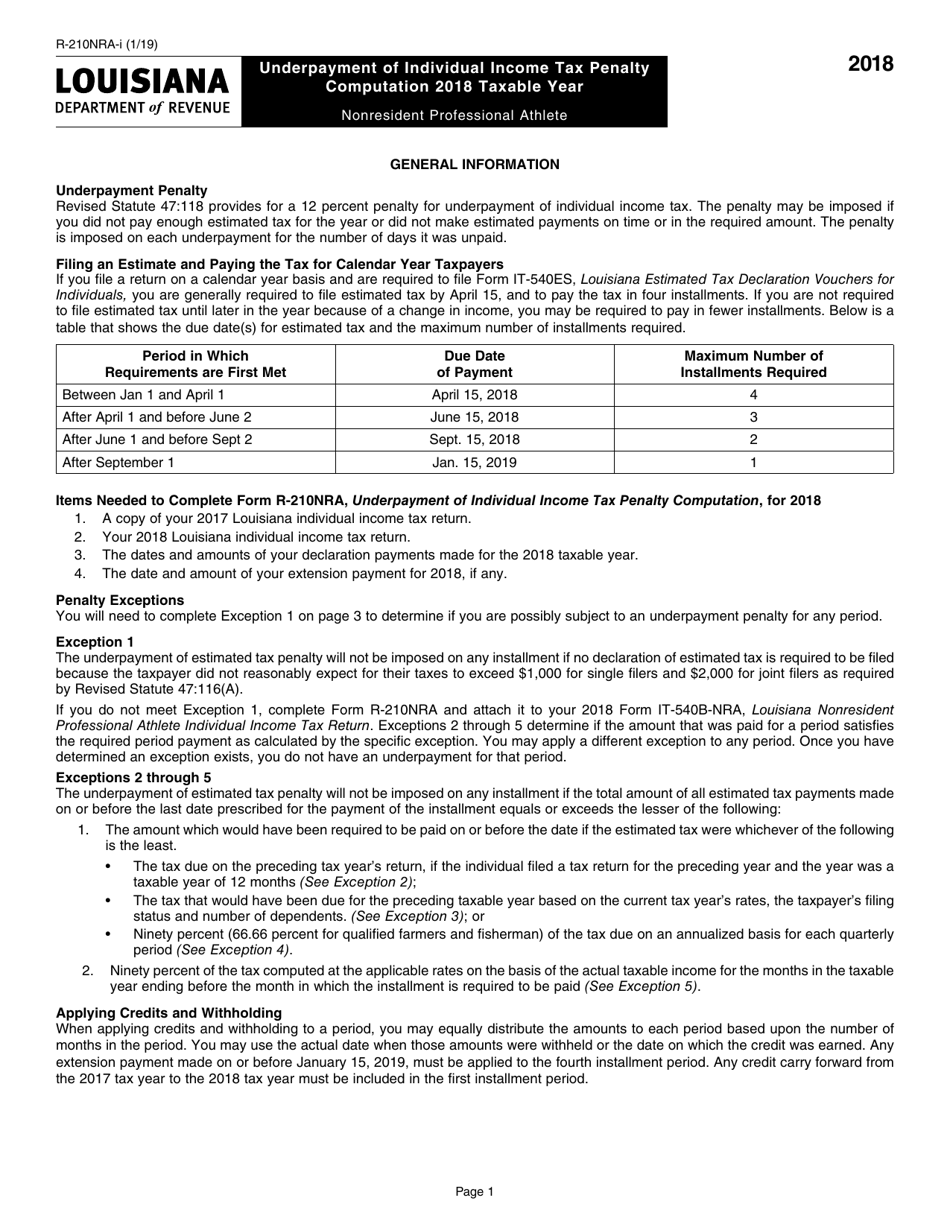

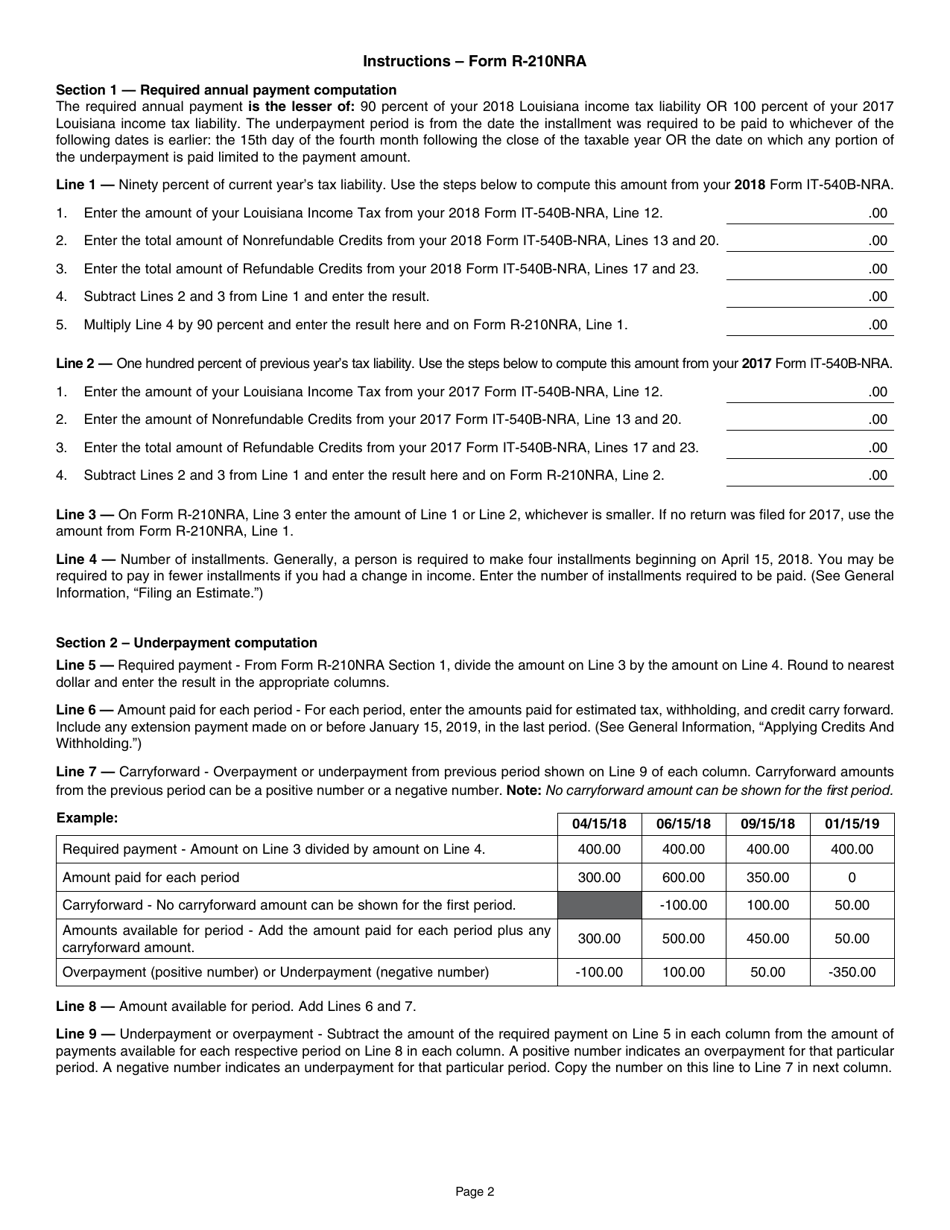

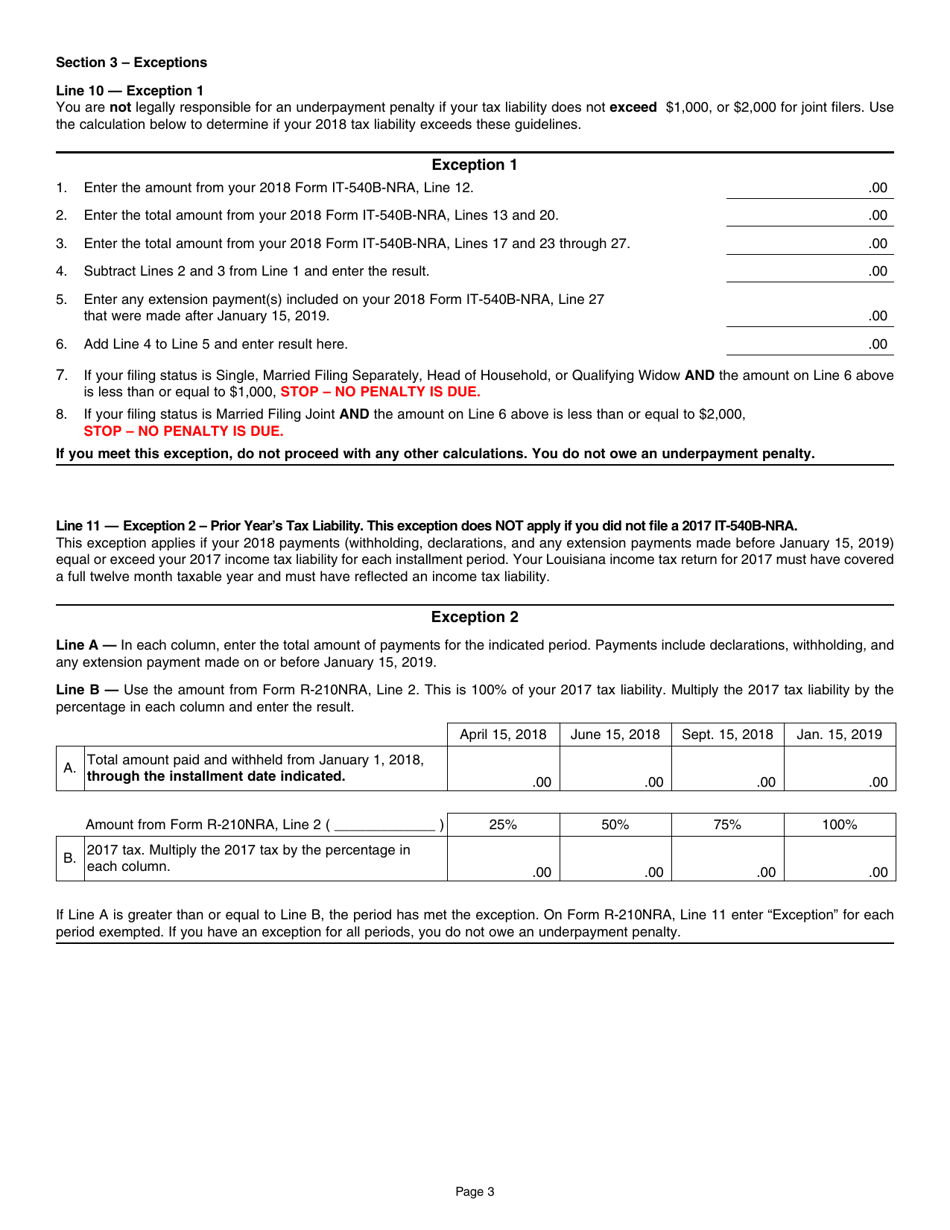

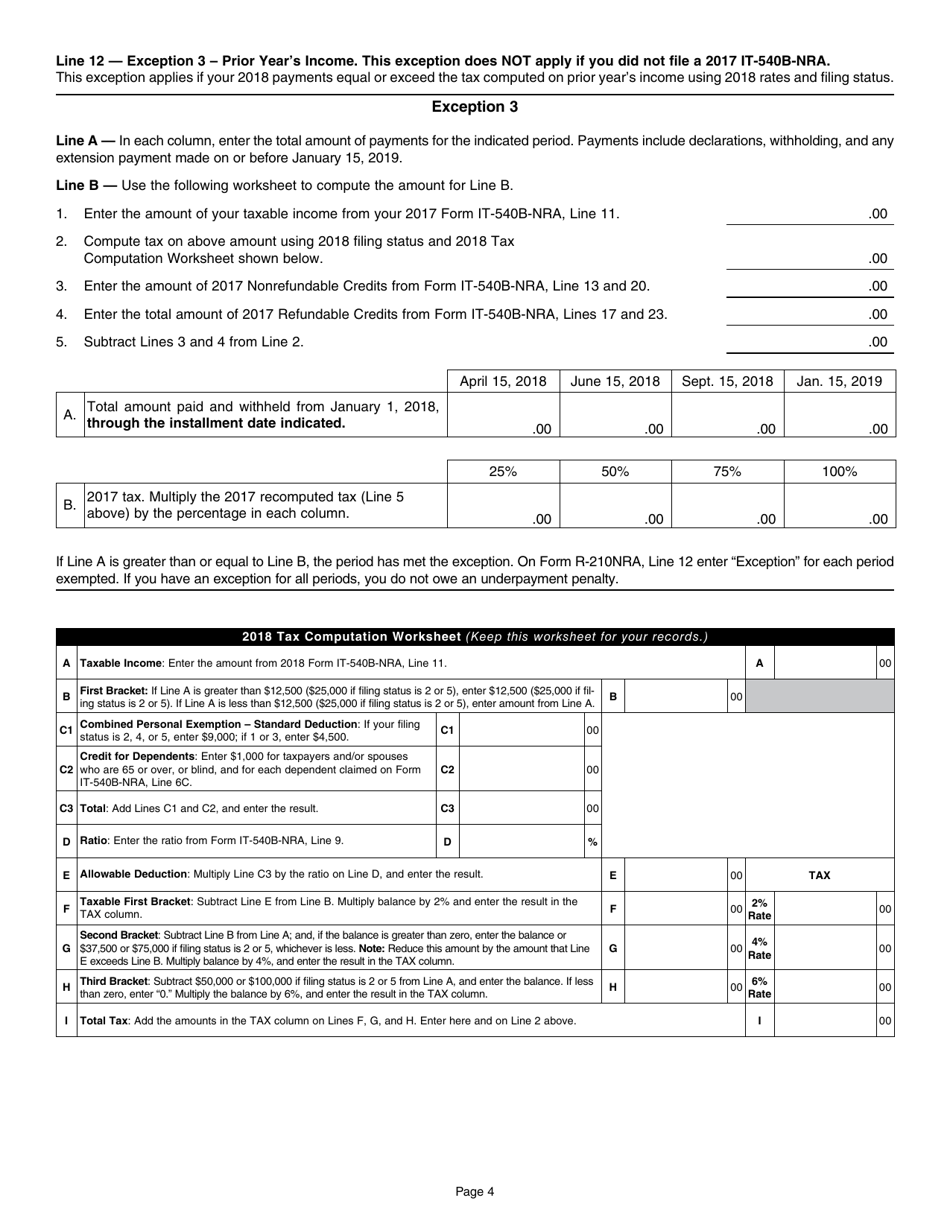

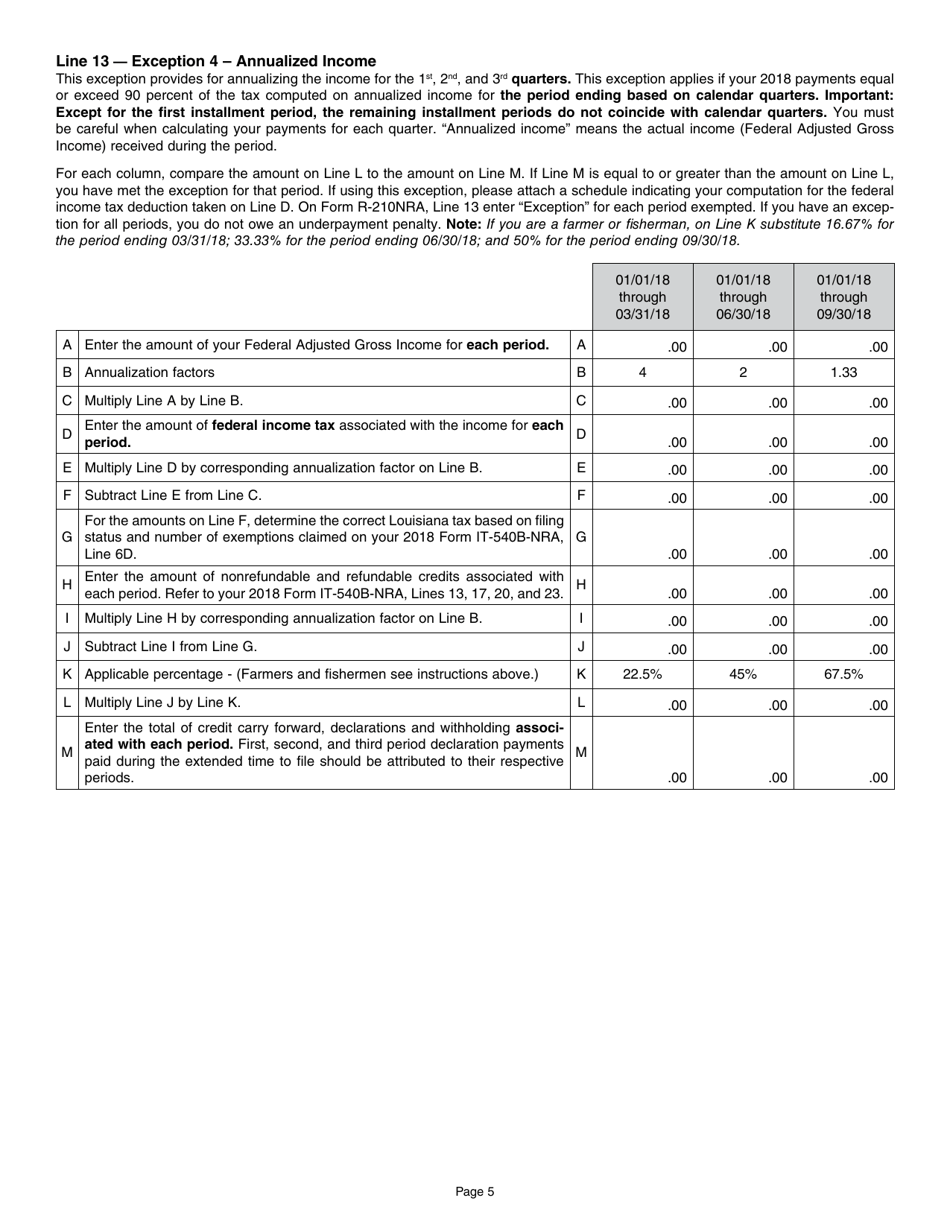

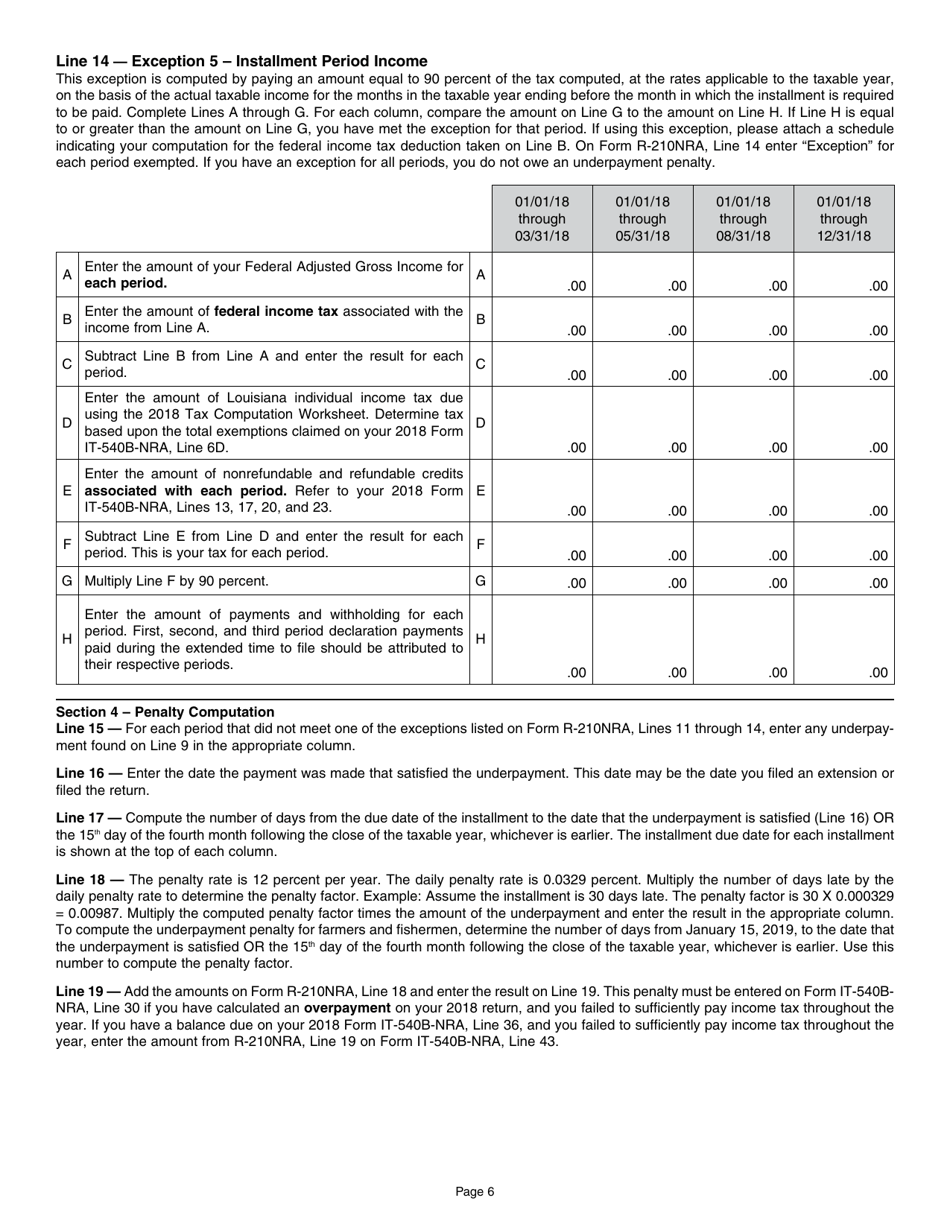

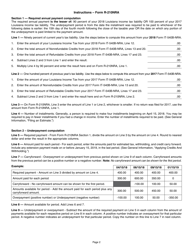

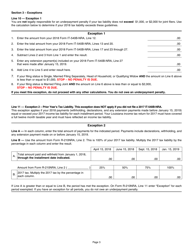

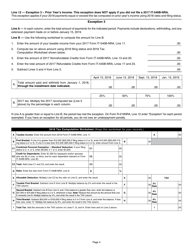

Instructions for Form R-210NRA Underpayment of Individual Income Tax Penalty - Louisiana

This document contains official instructions for Form R-210NRA , Underpayment of Individual Income Tax Penalty - a form released and collected by the Louisiana Department of Revenue. An up-to-date fillable Form R-210NRA is available for download through this link.

FAQ

Q: What is Form R-210NRA?

A: Form R-210NRA is a form used in Louisiana to calculate the underpayment of individual income tax penalty.

Q: Who is required to file Form R-210NRA?

A: Form R-210NRA is specifically for nonresident individuals who owe income tax in Louisiana.

Q: What is the underpayment of individual income tax penalty?

A: The underpayment of individual income tax penalty is a penalty imposed for not paying enough income tax throughout the year.

Q: How do I calculate the underpayment penalty?

A: You can use Form R-210NRA to calculate the underpayment penalty. The form provides instructions on how to do so.

Q: Is Form R-210NRA only for nonresidents?

A: Yes, Form R-210NRA is specifically for nonresident individuals who owe income tax in Louisiana.

Instruction Details:

- This 6-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Louisiana Department of Revenue.

Download Instructions for Form R-210NRA Underpayment of Individual Income Tax Penalty - Louisiana

1

2

3

4

5

6