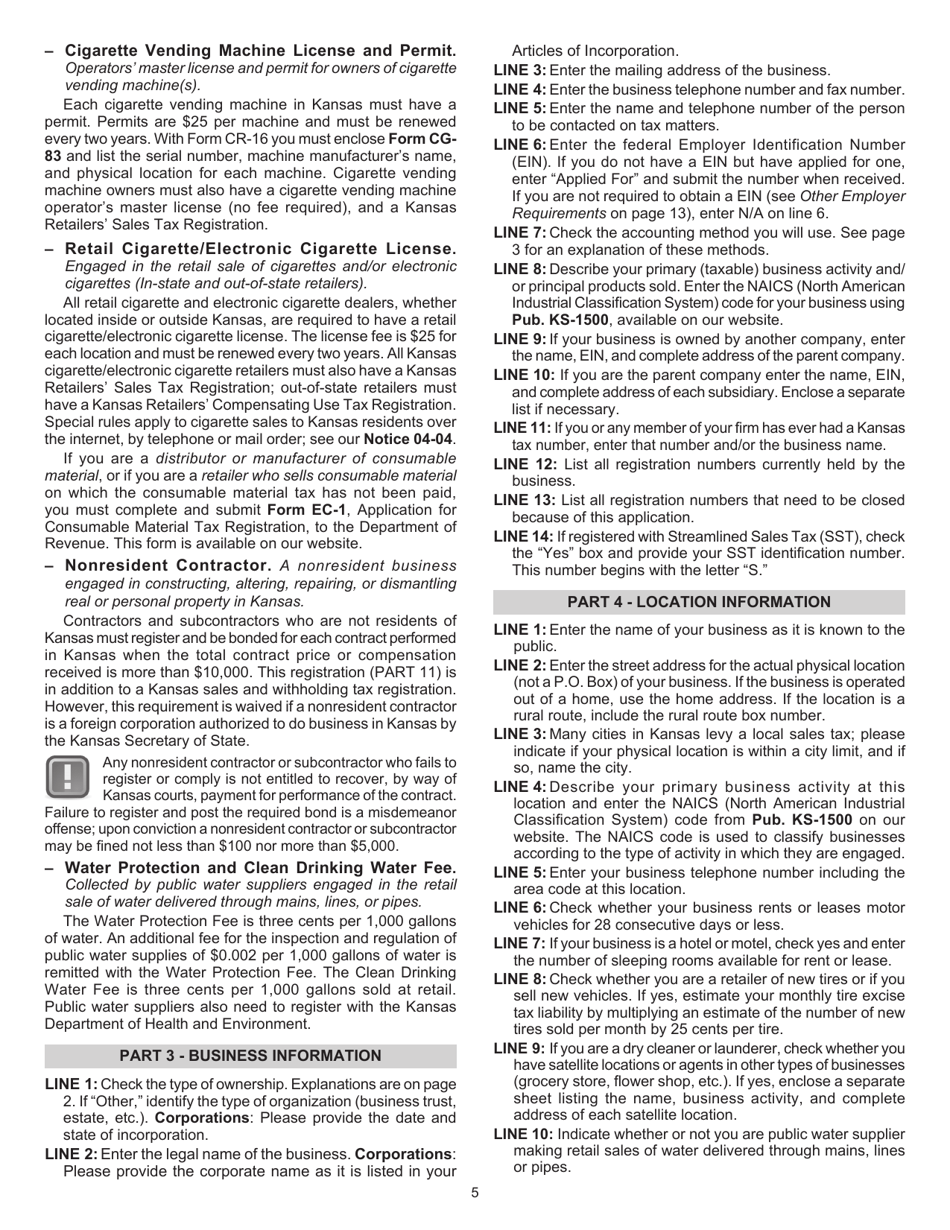

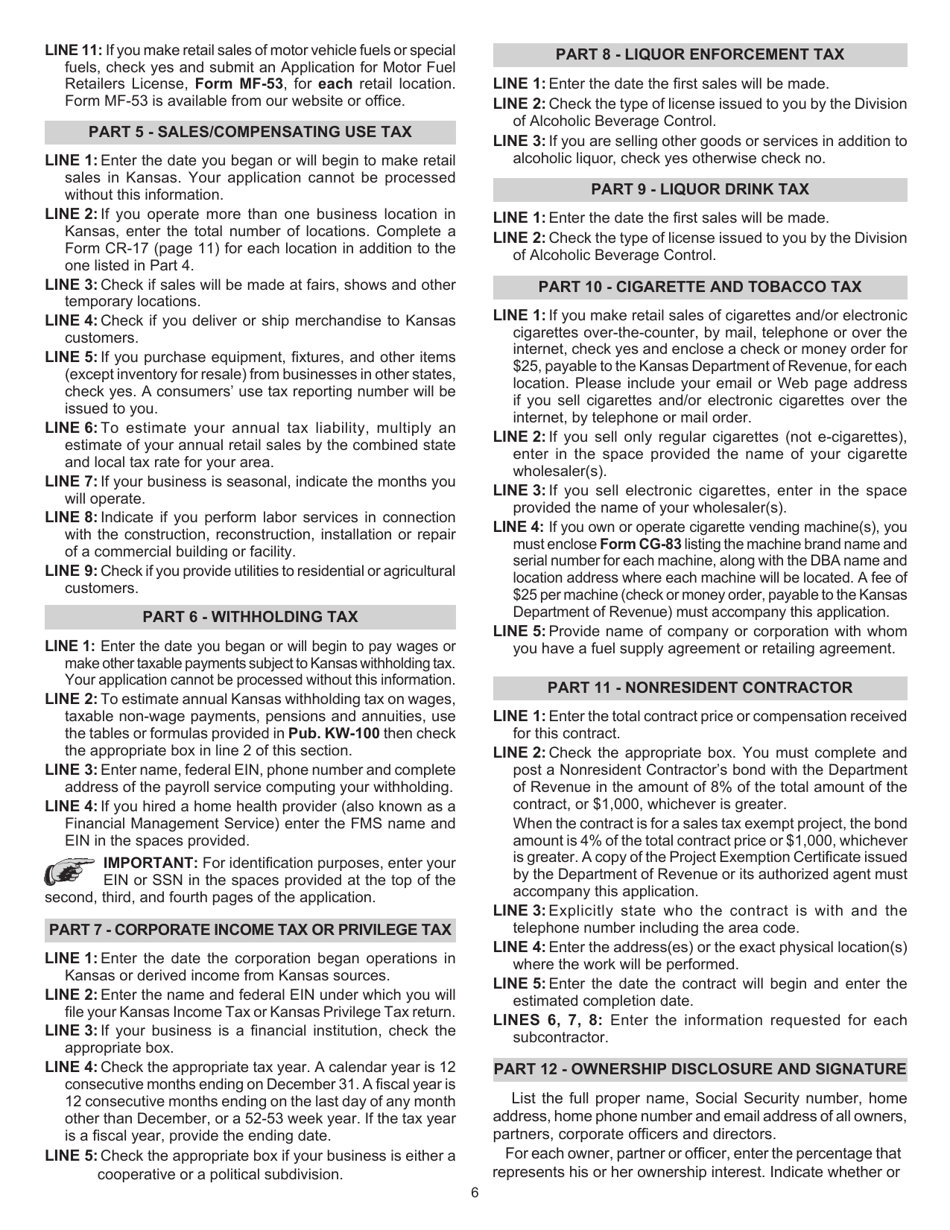

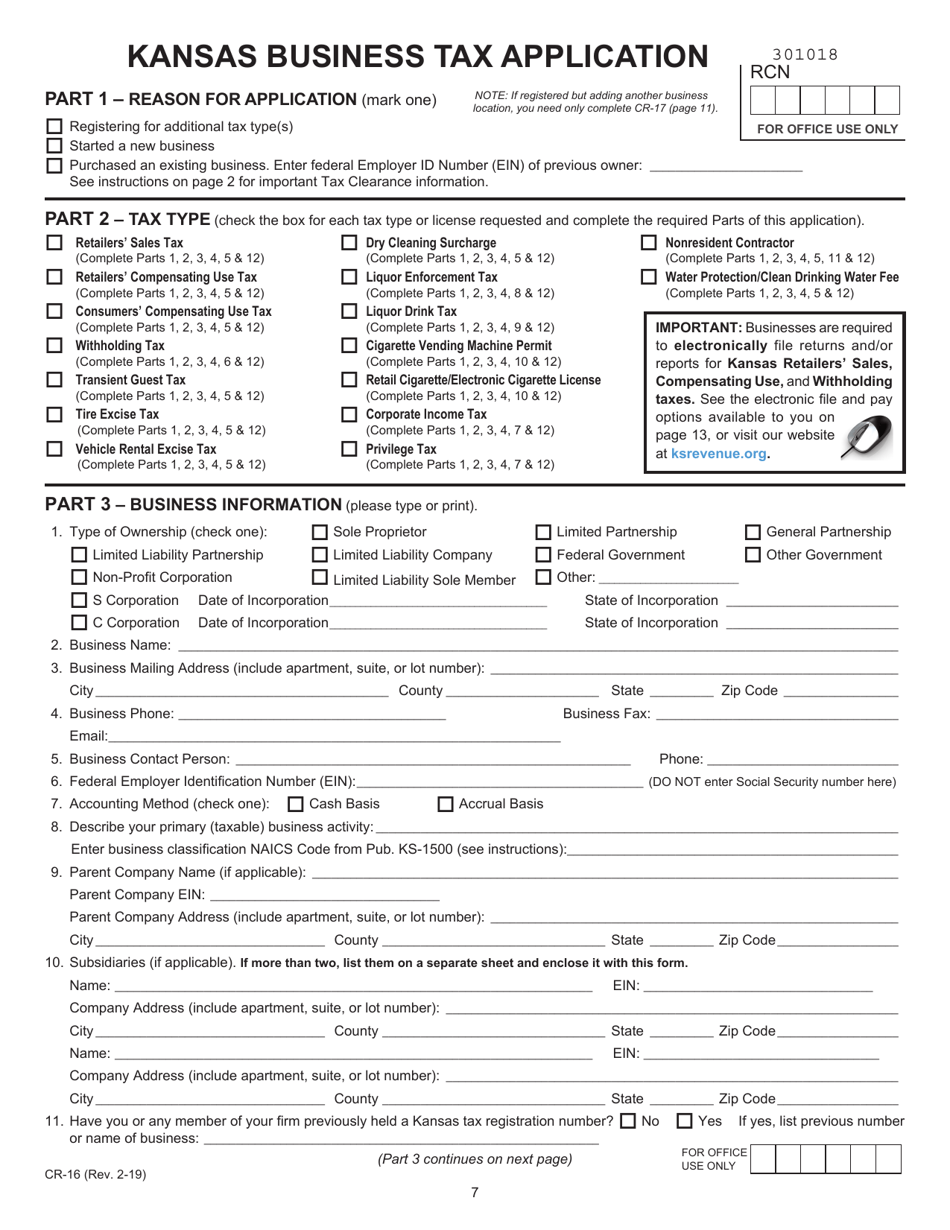

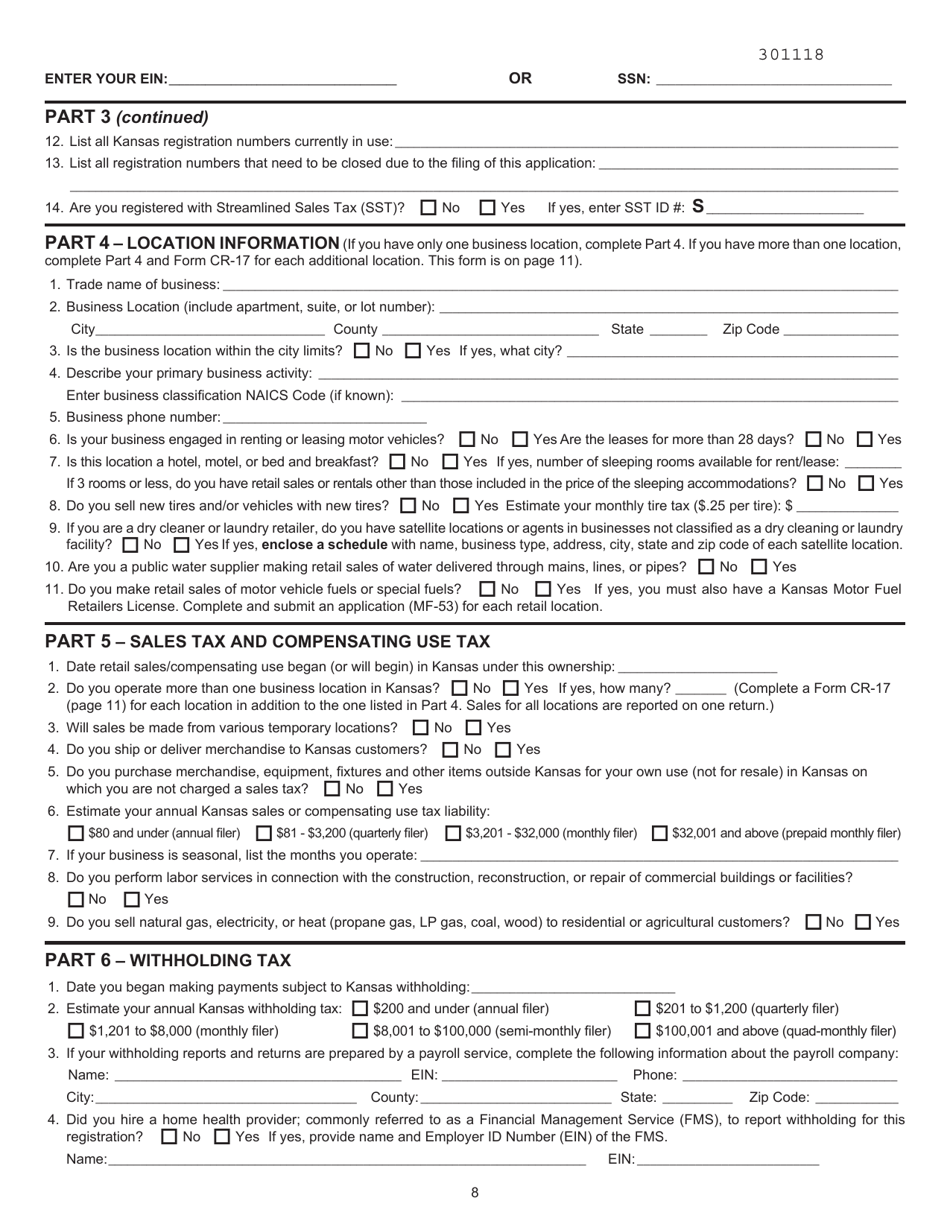

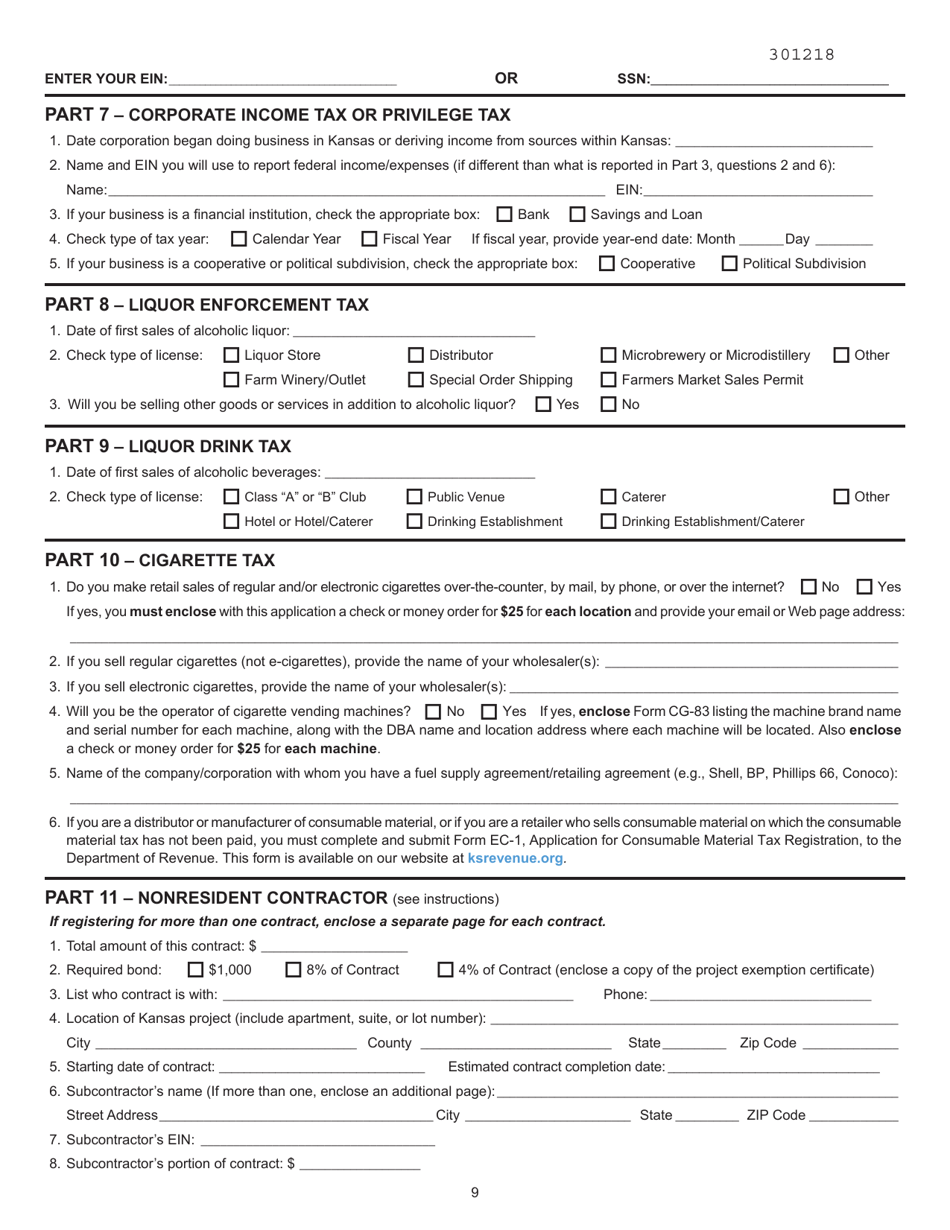

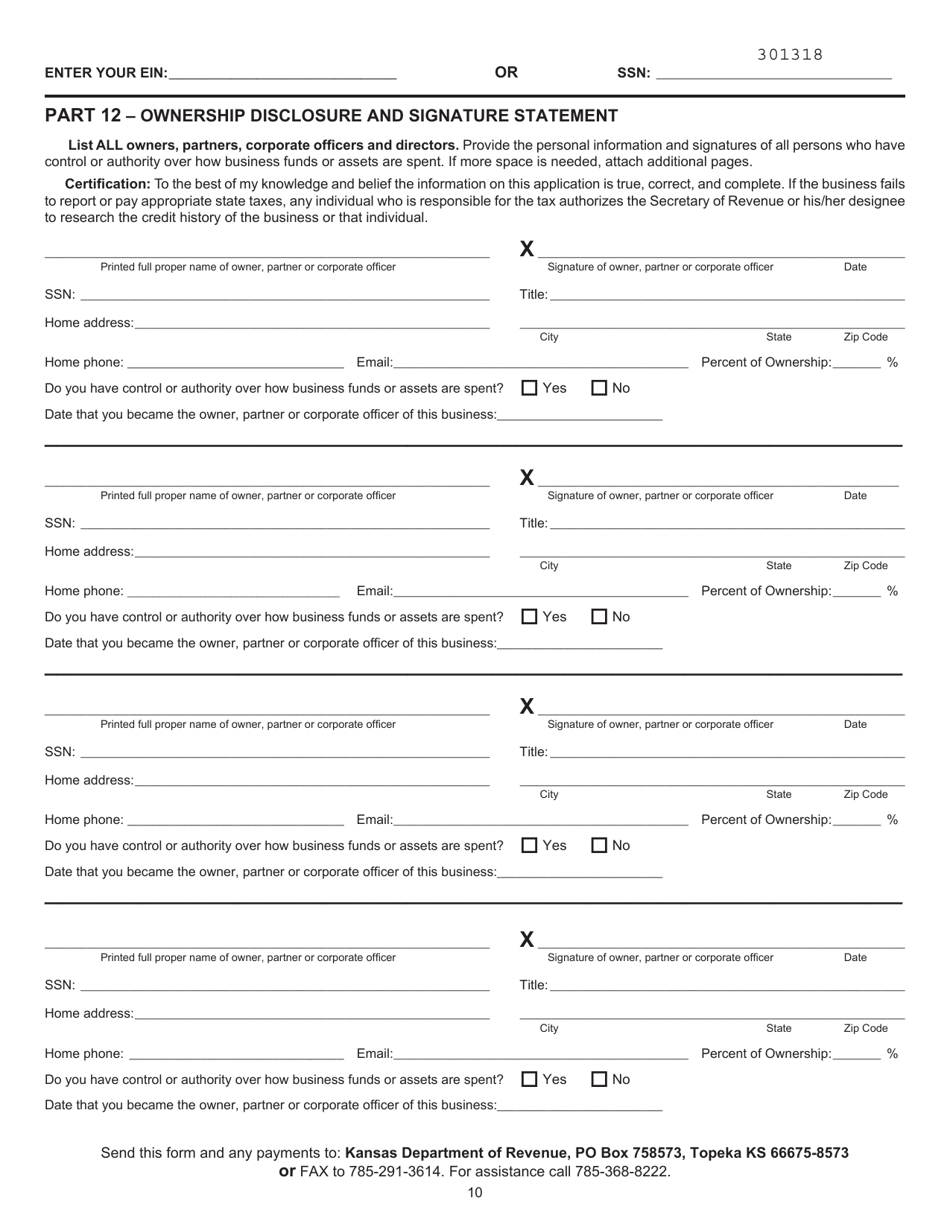

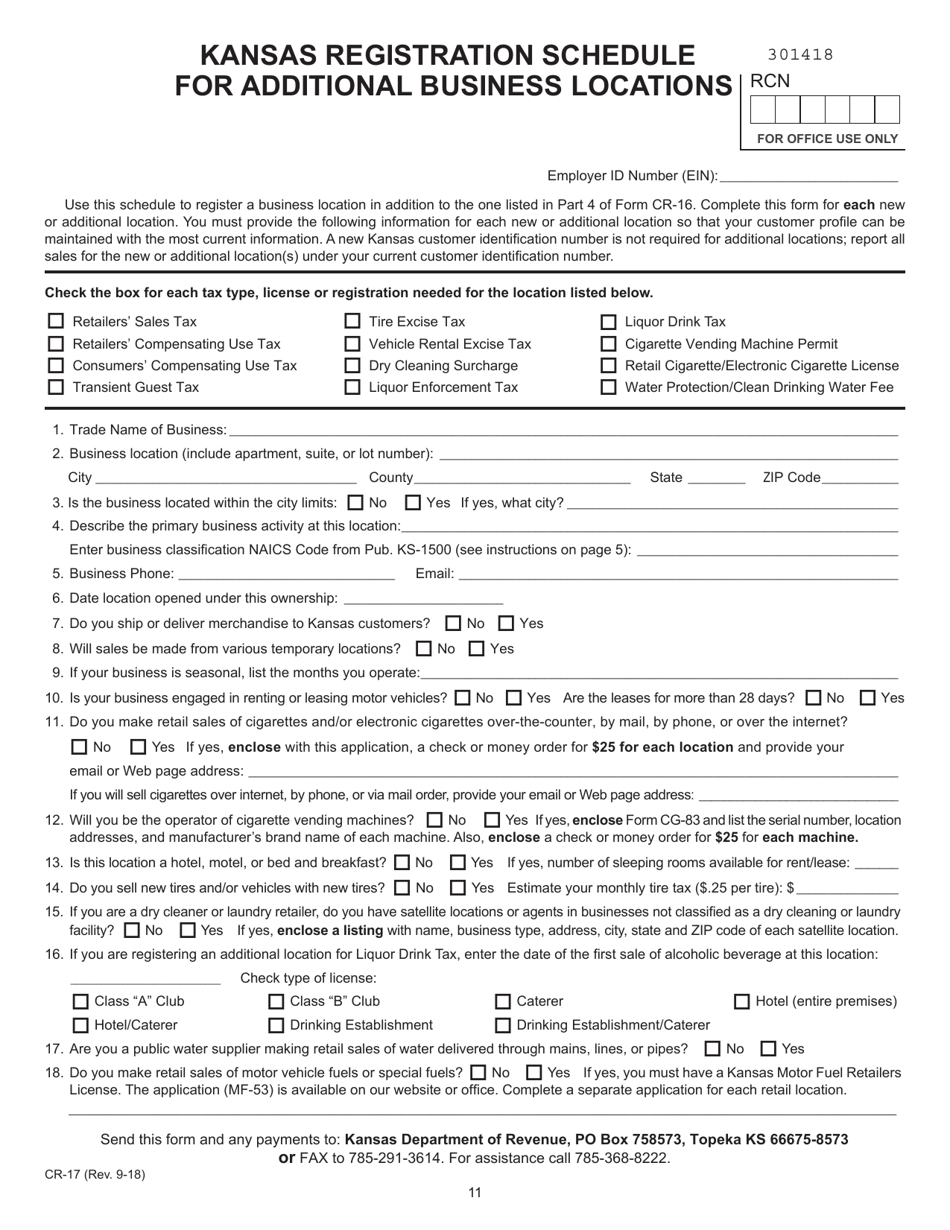

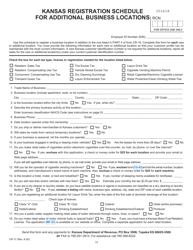

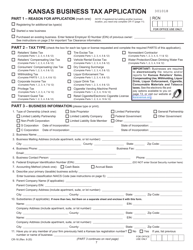

Form CR-1216 Kansas Business Tax Application Packet - Kansas

What Is Form CR-1216?

This is a legal form that was released by the Kansas Department of Revenue - a government authority operating within Kansas. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CR-1216?

A: Form CR-1216 is the Kansas Business Tax Application Packet.

Q: What is the purpose of Form CR-1216?

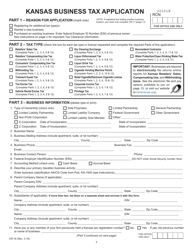

A: The purpose of Form CR-1216 is to apply for various business taxes in Kansas.

Q: What taxes can be applied for using Form CR-1216?

A: Form CR-1216 can be used to apply for sales tax, withholding tax, food service tax, liquor enforcement tax, tire fee, and several other taxes in Kansas.

Q: Is Form CR-1216 specific to Kansas?

A: Yes, Form CR-1216 is specific to the state of Kansas.

Q: Are there any fees associated with submitting Form CR-1216?

A: Some tax applications submitted using Form CR-1216 may require a fee. The specific fees depend on the type of tax being applied for.

Q: Are there any supporting documents required with Form CR-1216?

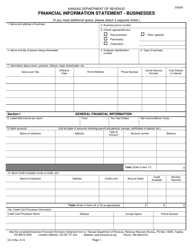

A: Yes, depending on the type of tax application, you may need to submit additional documents such as financial statements, proof of identification, or registration certificates.

Q: What is the deadline to submit Form CR-1216?

A: The deadline to submit Form CR-1216 depends on the type of tax being applied for. It is important to refer to the instructions provided with the form or check with the Kansas Department of Revenue for specific deadlines.

Q: Can I apply for multiple taxes using one Form CR-1216?

A: Yes, you can apply for multiple taxes using one Form CR-1216 if they are applicable to your business.

Form Details:

- Released on February 1, 2019;

- The latest edition provided by the Kansas Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CR-1216 by clicking the link below or browse more documents and templates provided by the Kansas Department of Revenue.

Download Form CR-1216 Kansas Business Tax Application Packet - Kansas

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16