![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 800C

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 800C

for the current year.

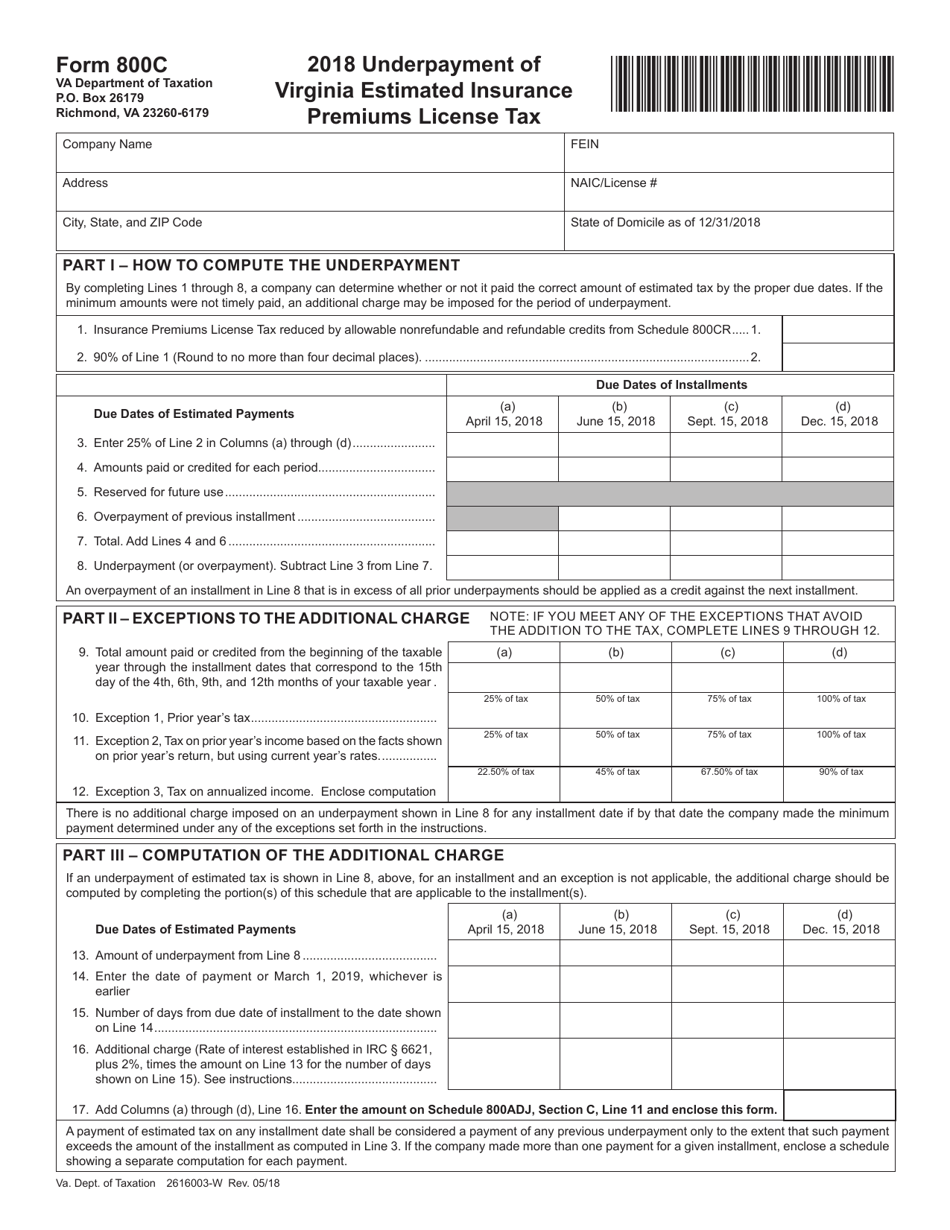

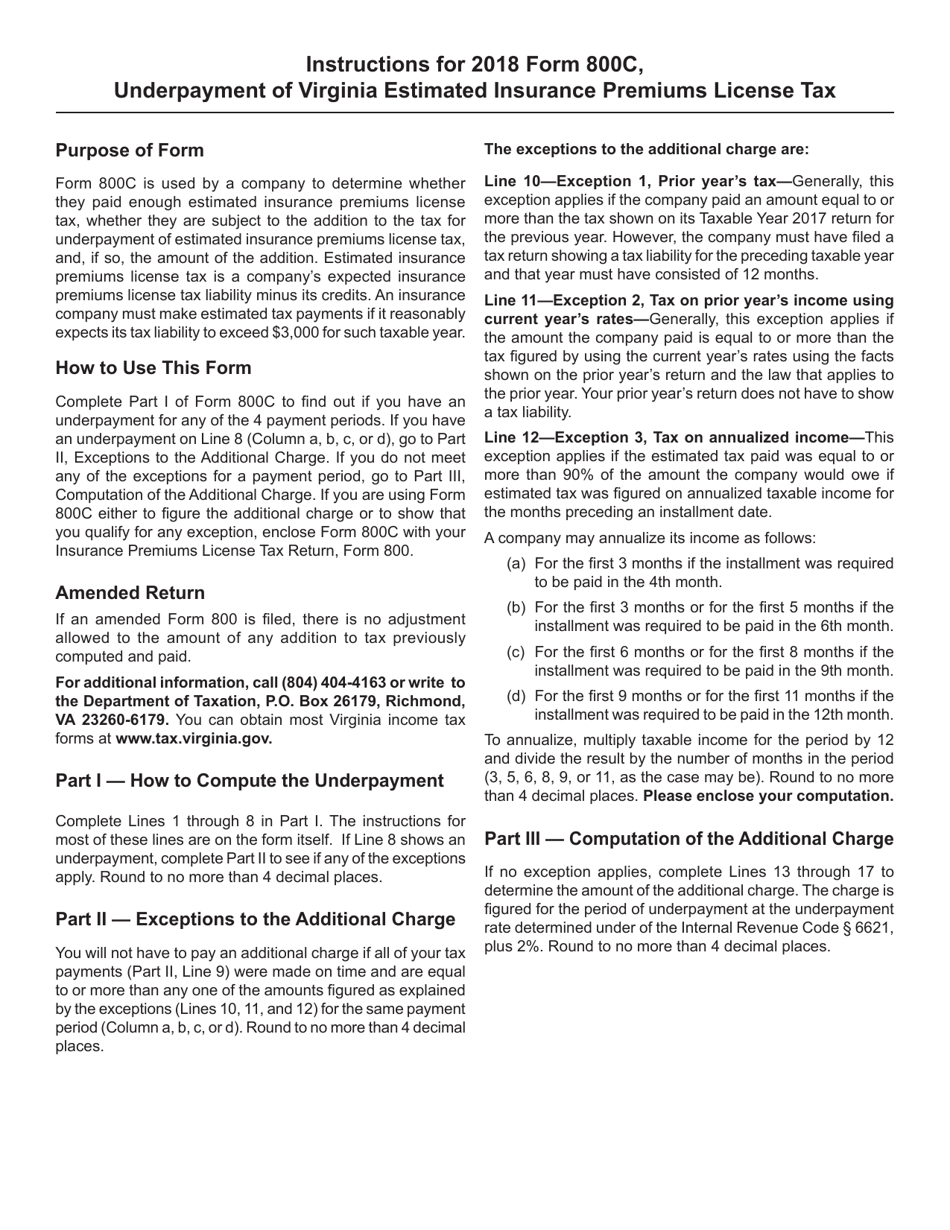

Form 800C Underpayment of Virginia Estimated Insurance Premiums License Tax - Virginia

What Is Form 800C?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 800C?

A: Form 800C is a tax form used in Virginia to report underpayment of estimated insurance premium license tax.

Q: What is the purpose of Form 800C?

A: The purpose of Form 800C is to notify the Virginia Department of Taxation about underpayment of estimated insurance premium license tax.

Q: Who needs to file Form 800C?

A: Anyone who underpaid their estimated insurance premium license tax in Virginia needs to file Form 800C.

Q: What is the penalty for underpaying the insurance premium license tax?

A: The penalty for underpaying the insurance premium license tax in Virginia is 6% per year, compounded daily.

Q: When is the deadline to file Form 800C?

A: The deadline to file Form 800C is the same as the deadline for filing the annual insurance premium license tax return, which is usually May 1st.

Q: Are there any exceptions or exemptions for filing Form 800C?

A: There are no specific exceptions or exemptions mentioned for filing Form 800C. If you underpaid the tax, you are required to file the form.

Q: What should I do if I made an underpayment of the insurance premium license tax?

A: If you made an underpayment of the insurance premium license tax in Virginia, you should promptly file Form 800C and pay any additional tax owed.

Q: Is there any penalty for late filing of Form 800C?

A: There is no specific mention of a penalty for late filing of Form 800C. However, it is always best to file the form and pay any additional tax owed as soon as possible.

Form Details:

- Released on May 1, 2018;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 800C by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.

Download Form 800C Underpayment of Virginia Estimated Insurance Premiums License Tax - Virginia

1

2