![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2 Schedule 27

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form T2 Schedule 27

for the current year.

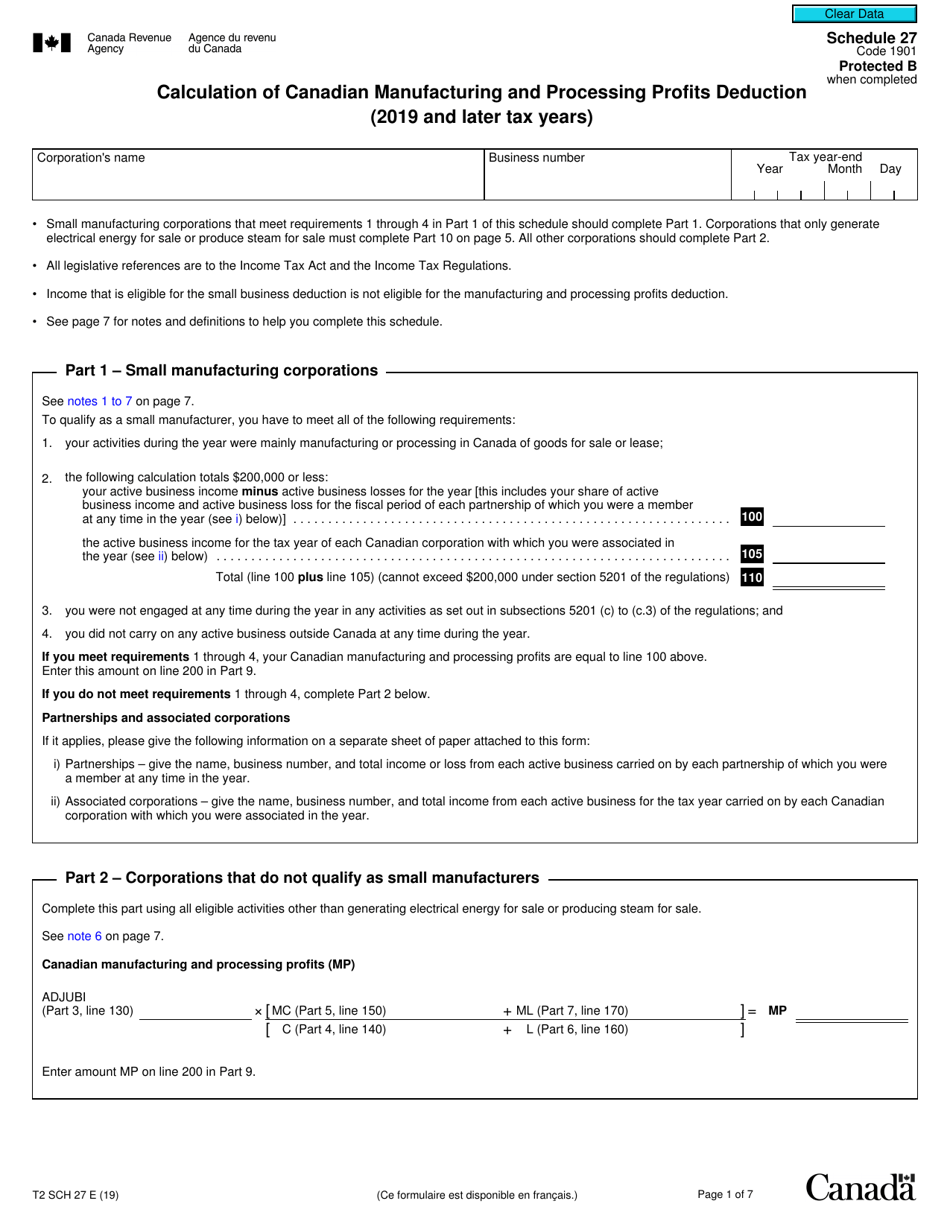

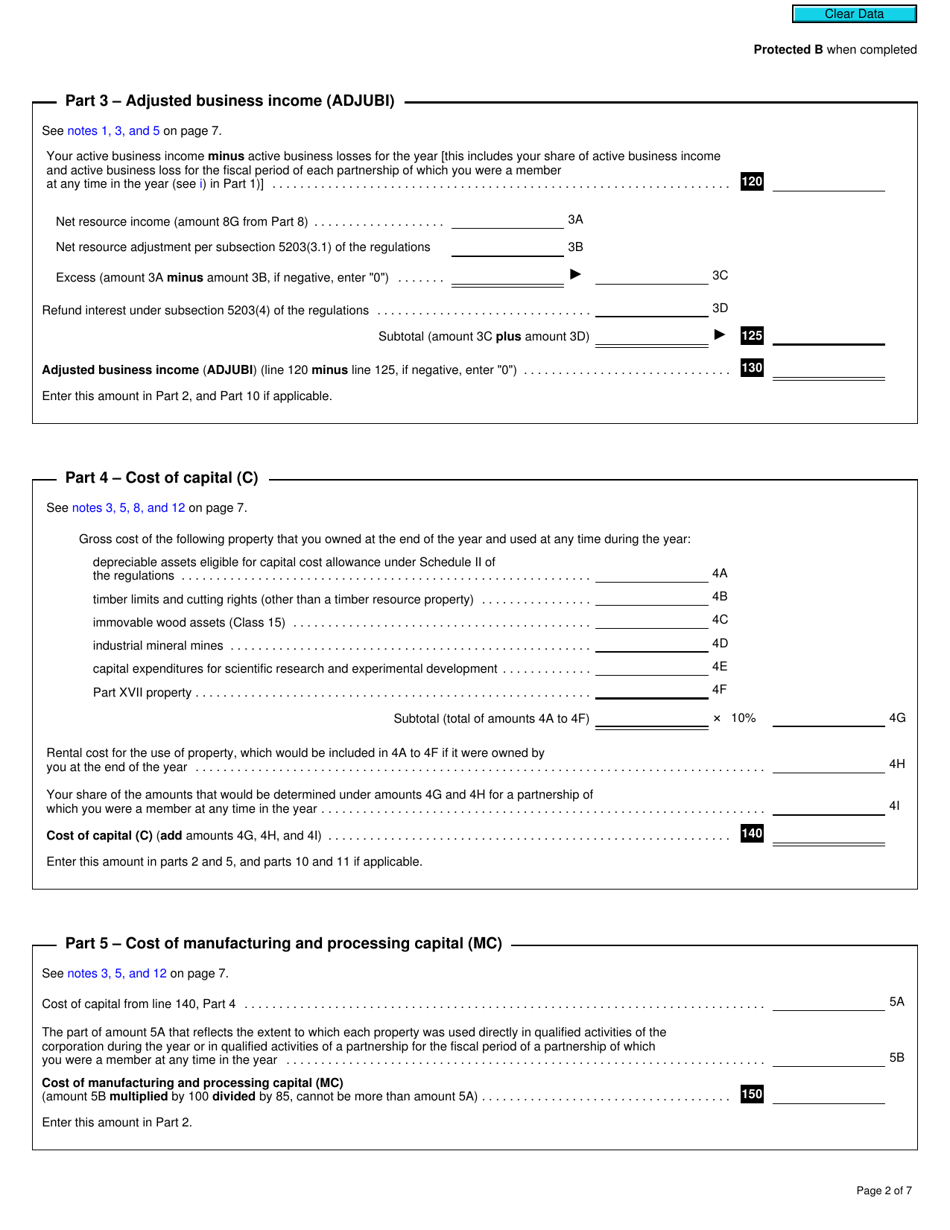

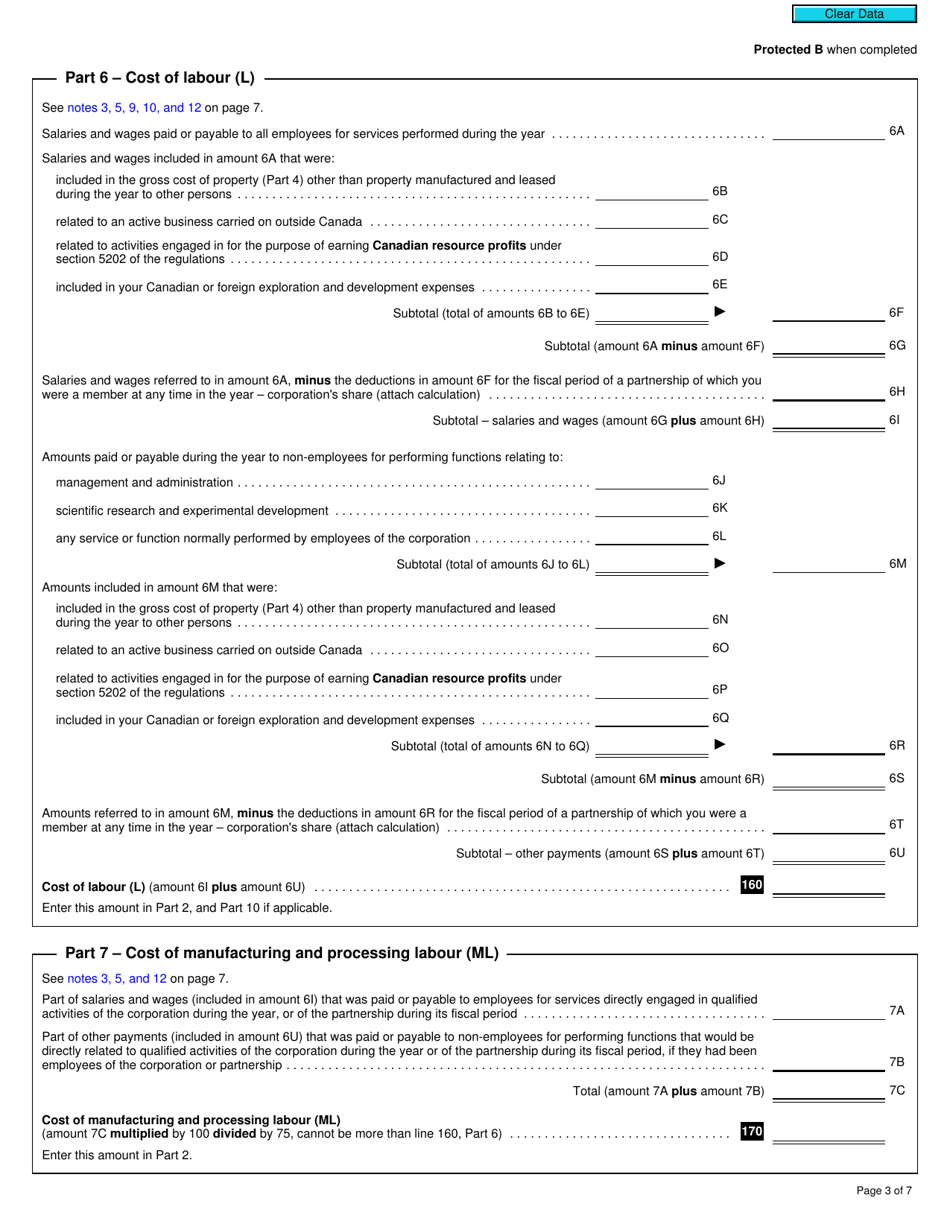

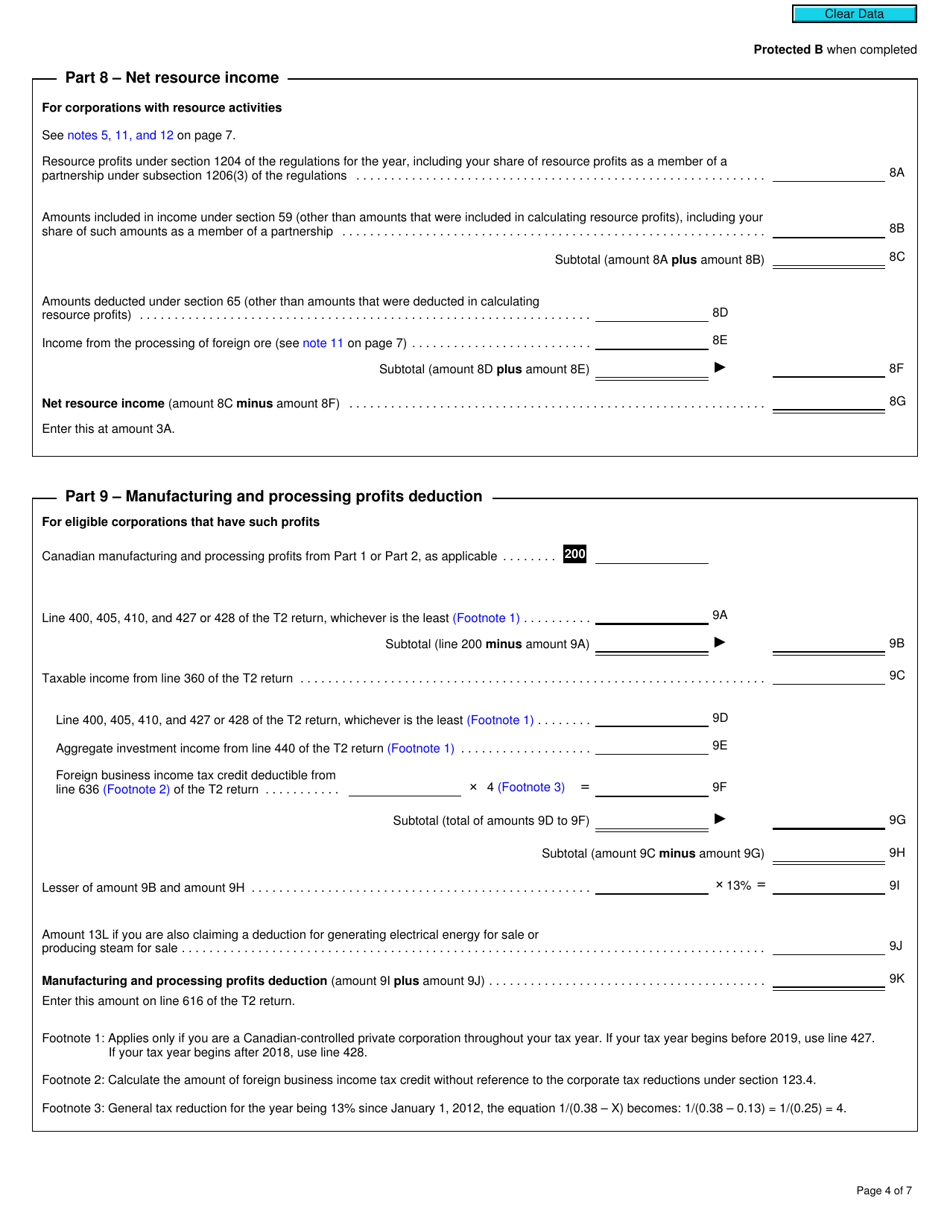

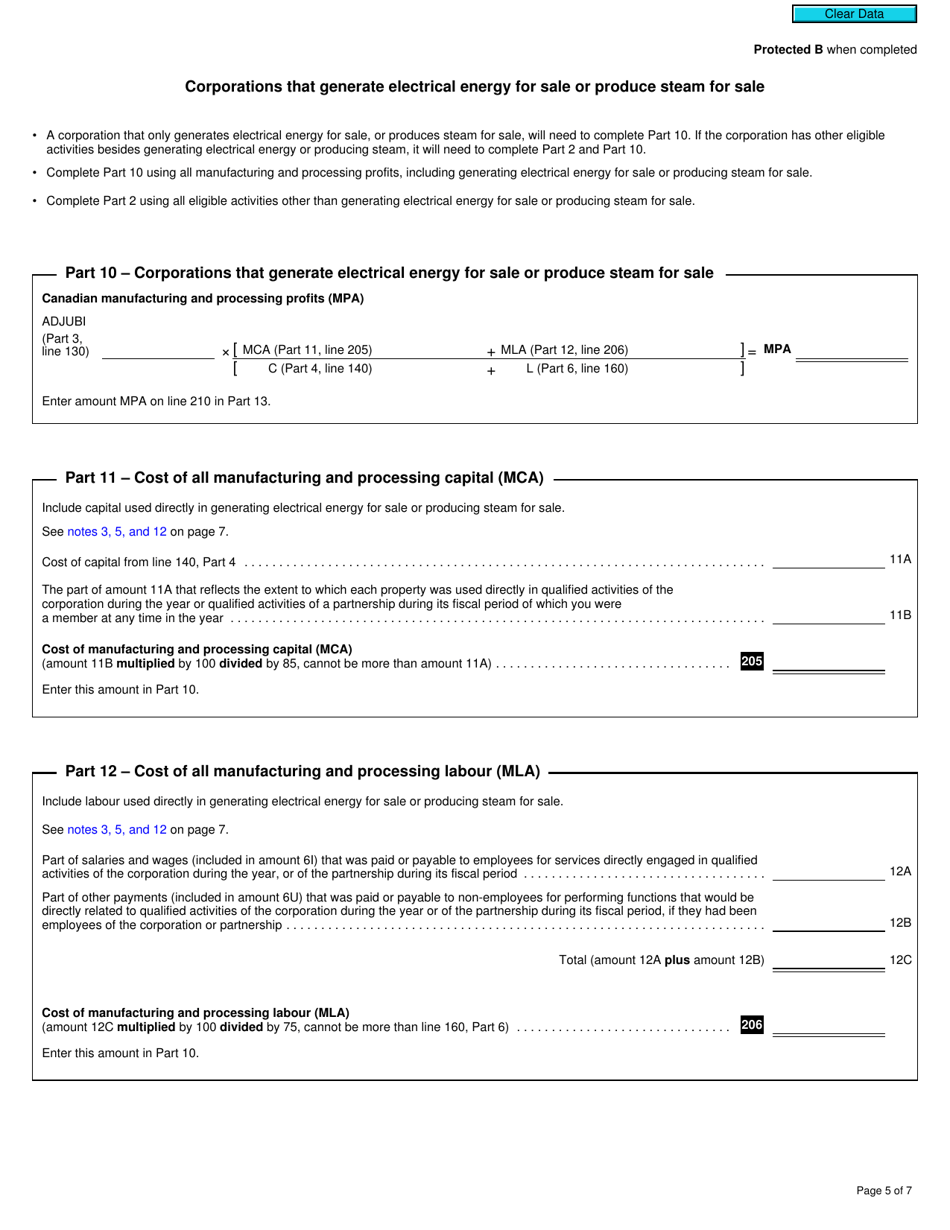

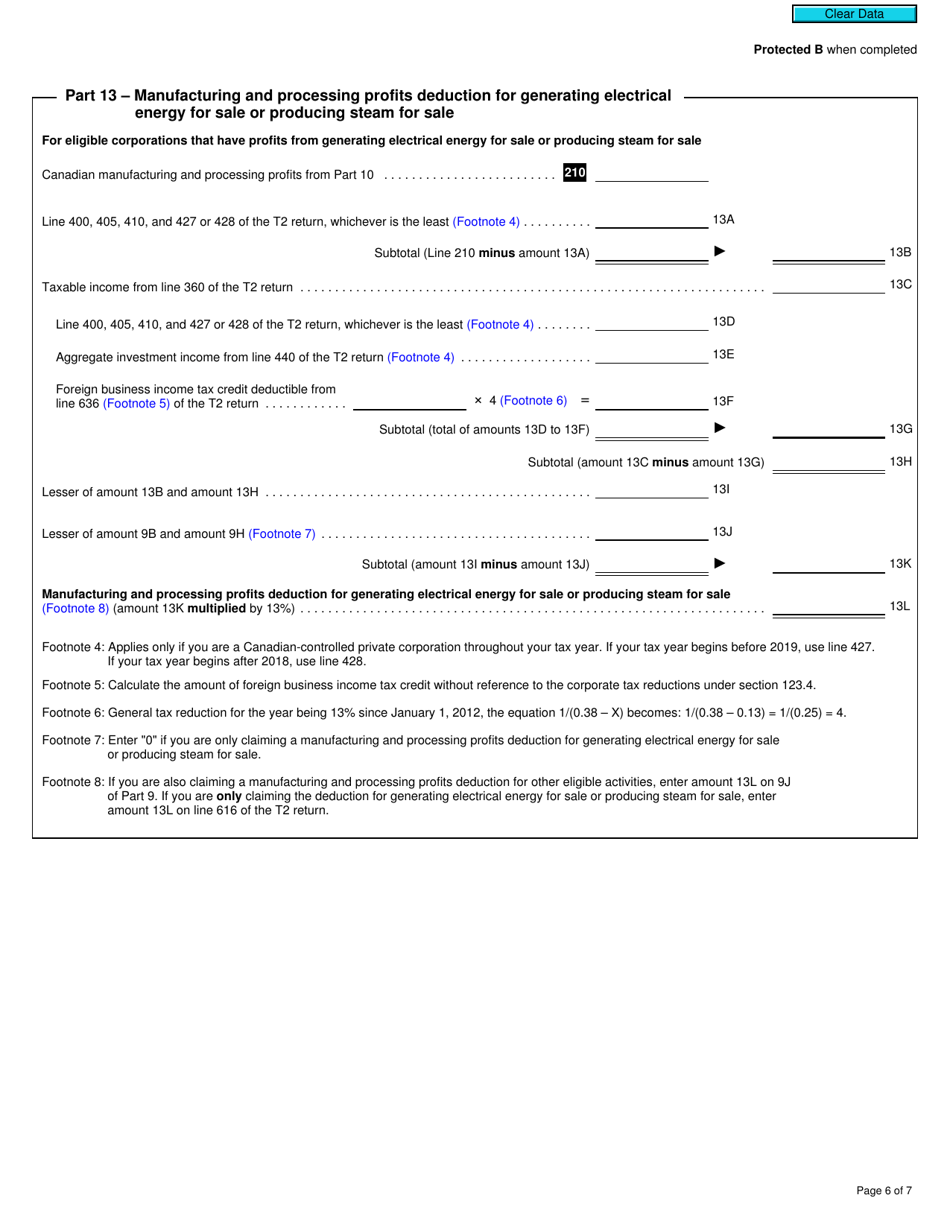

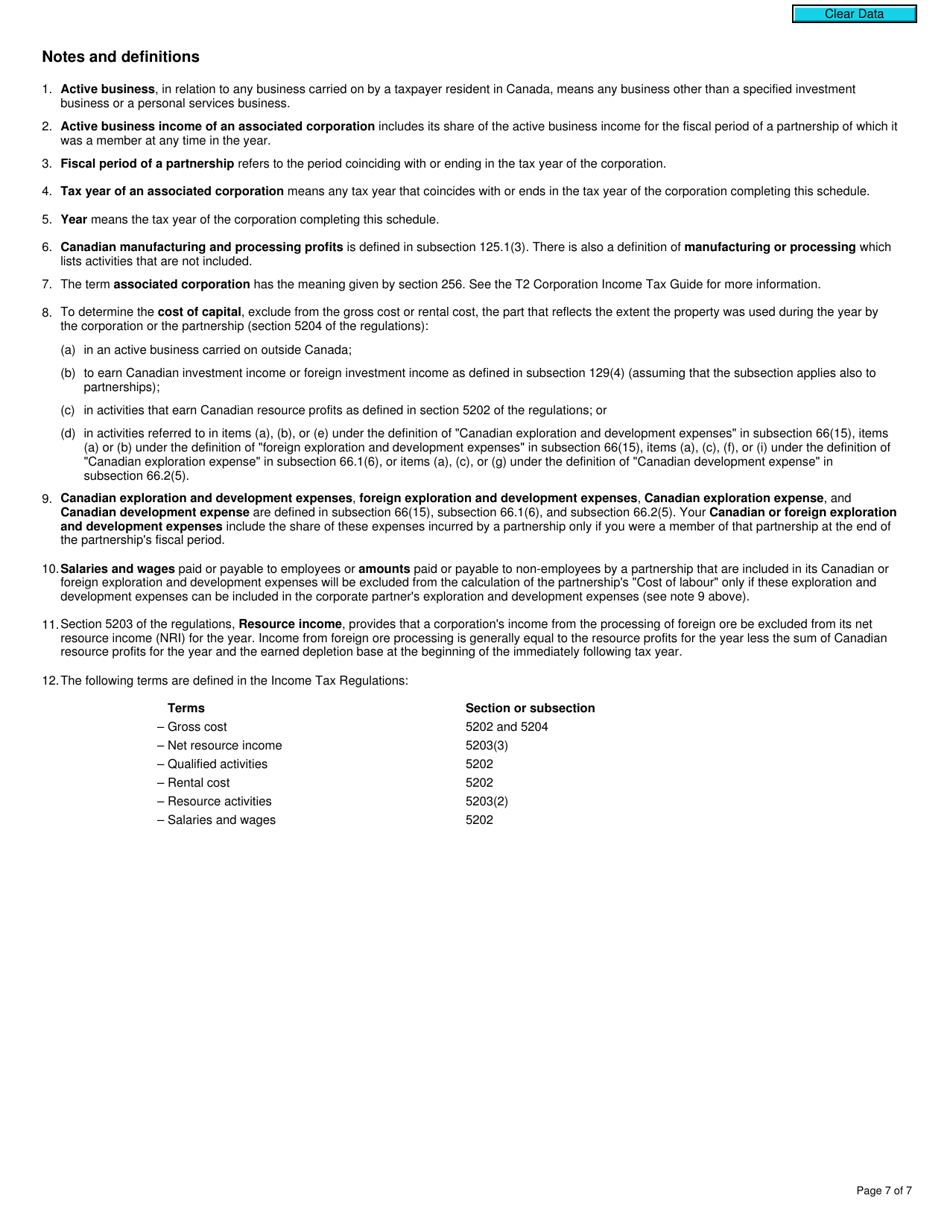

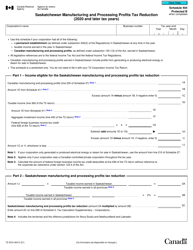

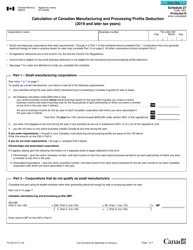

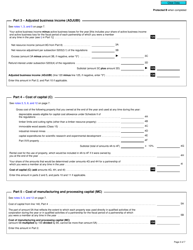

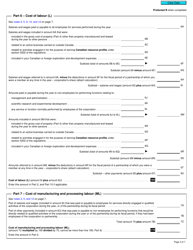

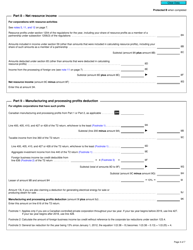

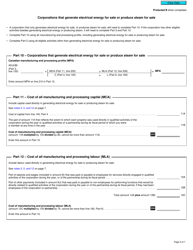

Form T2 Schedule 27 Calculation of Canadian Manufacturing and Processing Profits Deduction (2019 and Later Tax Years) - Canada

Form T2 Schedule 27 Calculation of Canadian Manufacturing and Processing Profits Deduction (2019 and Later Tax Years) in Canada is used by corporations to calculate their manufacturing and processing profits deduction for tax purposes.

The Form T2 Schedule 27 is filed by Canadian corporations that want to claim the Manufacturing and Processing Profits Deduction.

FAQ

Q: What is Form T2 Schedule 27?

A: Form T2 Schedule 27 is used to calculate the Canadian Manufacturing and Processing Profits Deduction.

Q: What is the Canadian Manufacturing and Processing Profits Deduction?

A: It is a tax deduction available to Canadian corporations engaged in manufacturing or processing activities.

Q: Who is eligible for the deduction?

A: Canadian corporations engaged in manufacturing or processing activities are eligible for the deduction.

Q: How is the deduction calculated?

A: The deduction is calculated based on a percentage of the corporation's income from manufacturing or processing activities.

Q: Are there any limitations or restrictions on the deduction?

A: Yes, there are certain limitations and restrictions on the deduction, which are outlined in the tax laws and regulations.

Q: Is Form T2 Schedule 27 only for tax year 2019 and later?

A: Yes, Form T2 Schedule 27 is specifically for tax years 2019 and later.

Q: Are there any filing deadlines for Form T2 Schedule 27?

A: Yes, the filing deadline for Form T2 Schedule 27 is the same as the corporation's tax return filing deadline.

Q: Do I need to attach any supporting documents with Form T2 Schedule 27?

A: Yes, you may be required to attach supporting documents to substantiate your claim for the deduction.

Q: Can I claim the Canadian Manufacturing and Processing Profits Deduction if I am a sole proprietor or a partnership?

A: No, the deduction is only available to Canadian corporations.

Download Form T2 Schedule 27 Calculation of Canadian Manufacturing and Processing Profits Deduction (2019 and Later Tax Years) - Canada

1

2

3

4

5

6

7