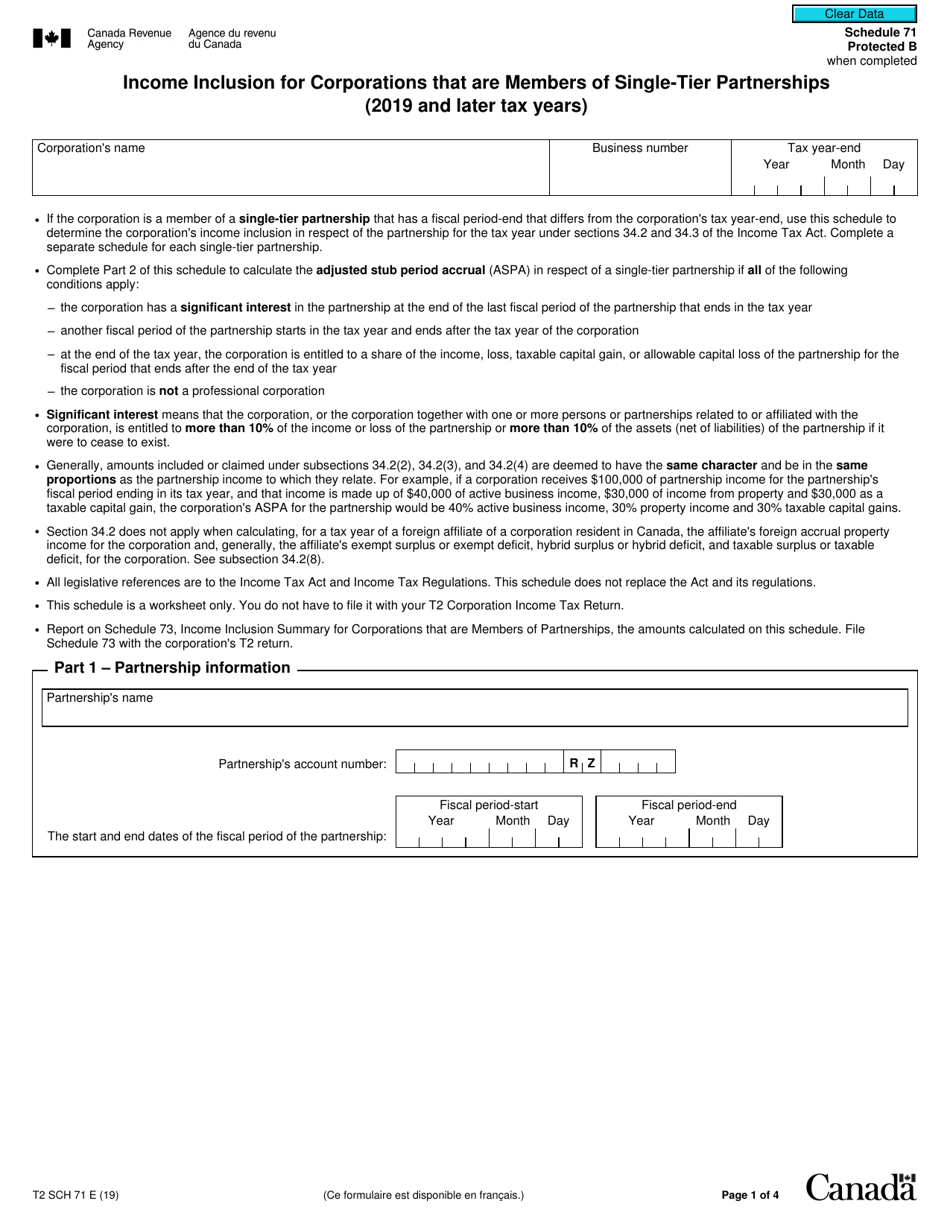

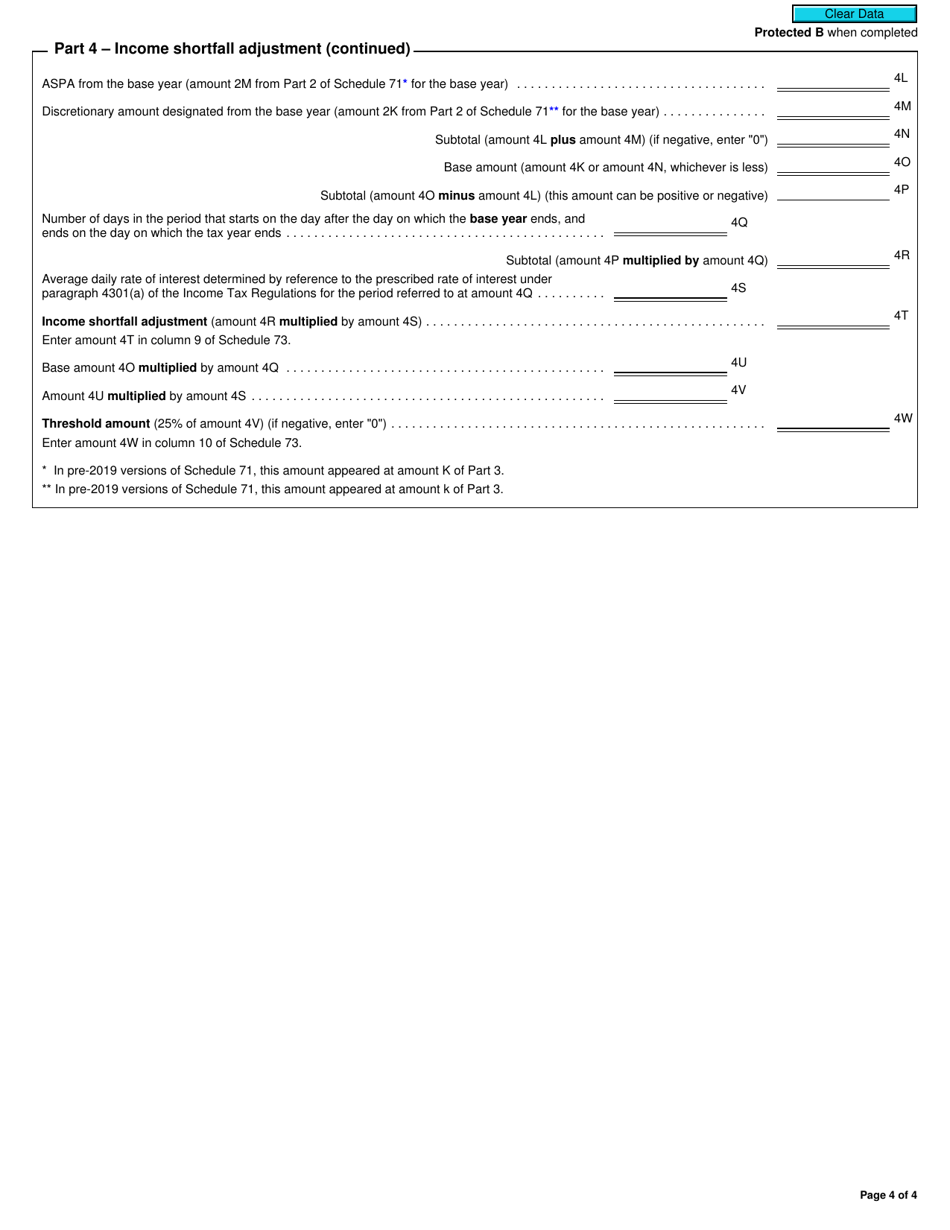

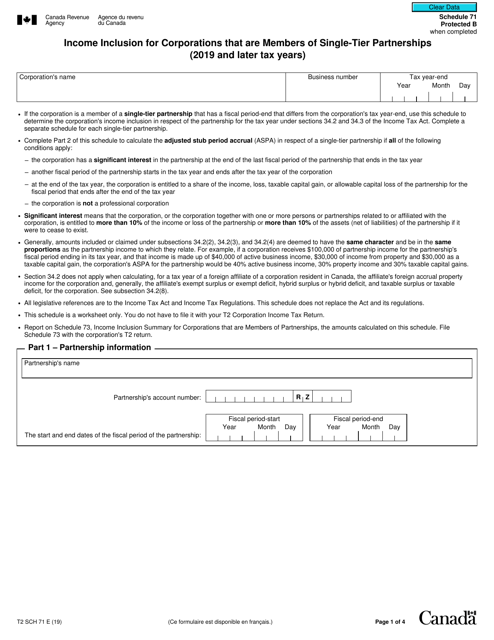

Form T2 Schedule 71 Income Inclusion for Corporations That Are Members of Single-Tier Partnerships (2019 and Later Tax Years) - Canada

Form T2 Schedule 71 in Canada is used by corporations that are members of single-tier partnerships to report their income inclusion for tax purposes. It is applicable for tax years 2019 and later.

The form T2 Schedule 71 is filed by corporations that are members of single-tier partnerships for the tax years 2019 and later in Canada.

FAQ

Q: What is Form T2 Schedule 71?

A: Form T2 Schedule 71 is a tax form used by corporations in Canada that are members of single-tier partnerships to report their income inclusion for tax purposes.

Q: Who needs to file Form T2 Schedule 71?

A: Corporations in Canada that are members of single-tier partnerships need to file Form T2 Schedule 71.

Q: What does Form T2 Schedule 71 report?

A: Form T2 Schedule 71 reports the income inclusion for corporations that are members of single-tier partnerships.

Q: What tax years is Form T2 Schedule 71 applicable for?

A: Form T2 Schedule 71 is applicable for tax years starting in 2019 and later.

Download Form T2 Schedule 71 Income Inclusion for Corporations That Are Members of Single-Tier Partnerships (2019 and Later Tax Years) - Canada

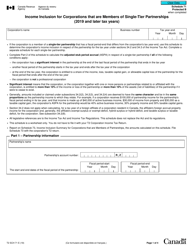

1

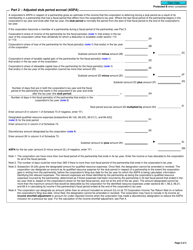

2

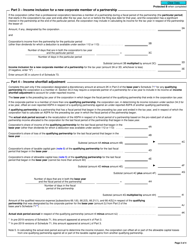

3

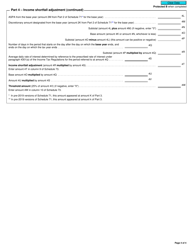

4