![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form TC-41

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form TC-41

for the current year.

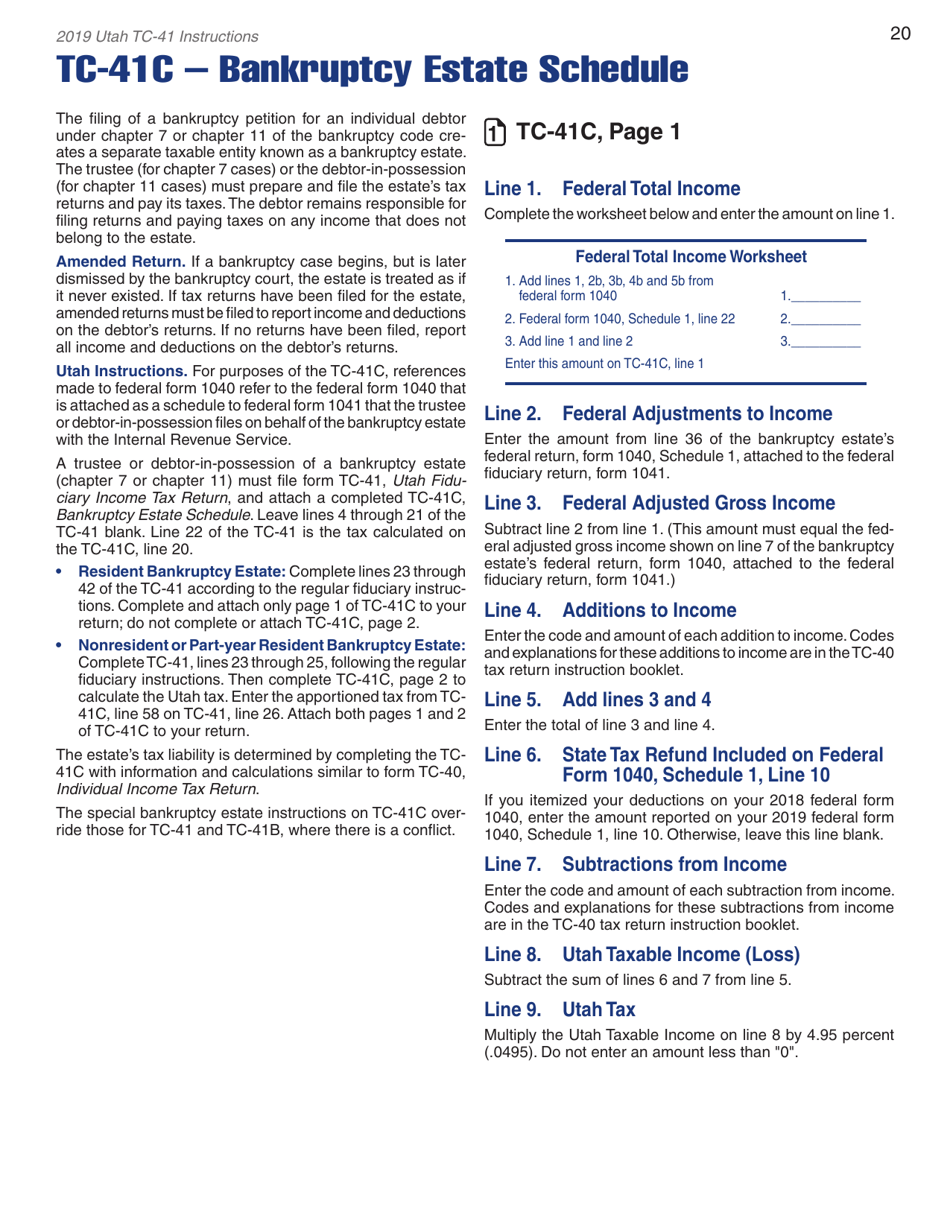

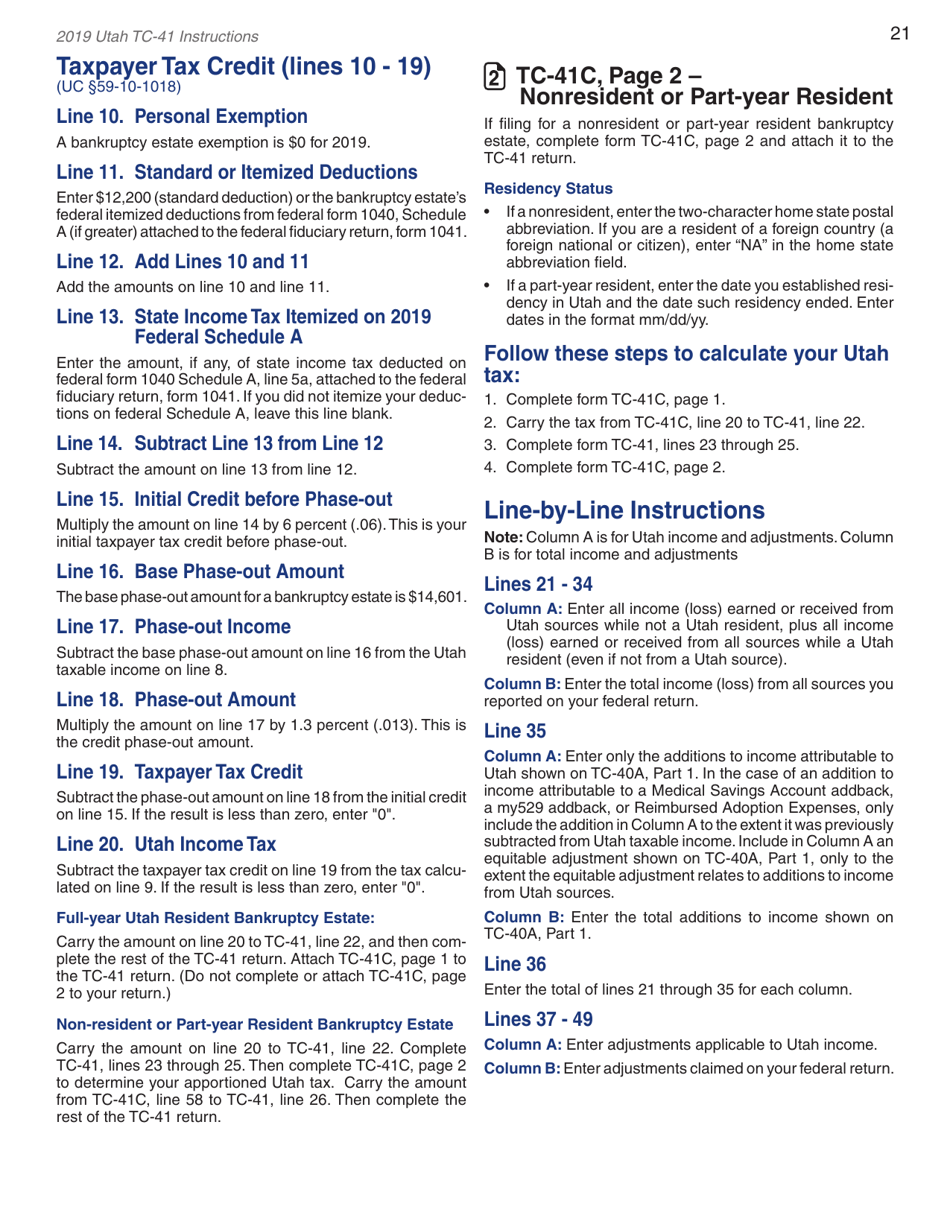

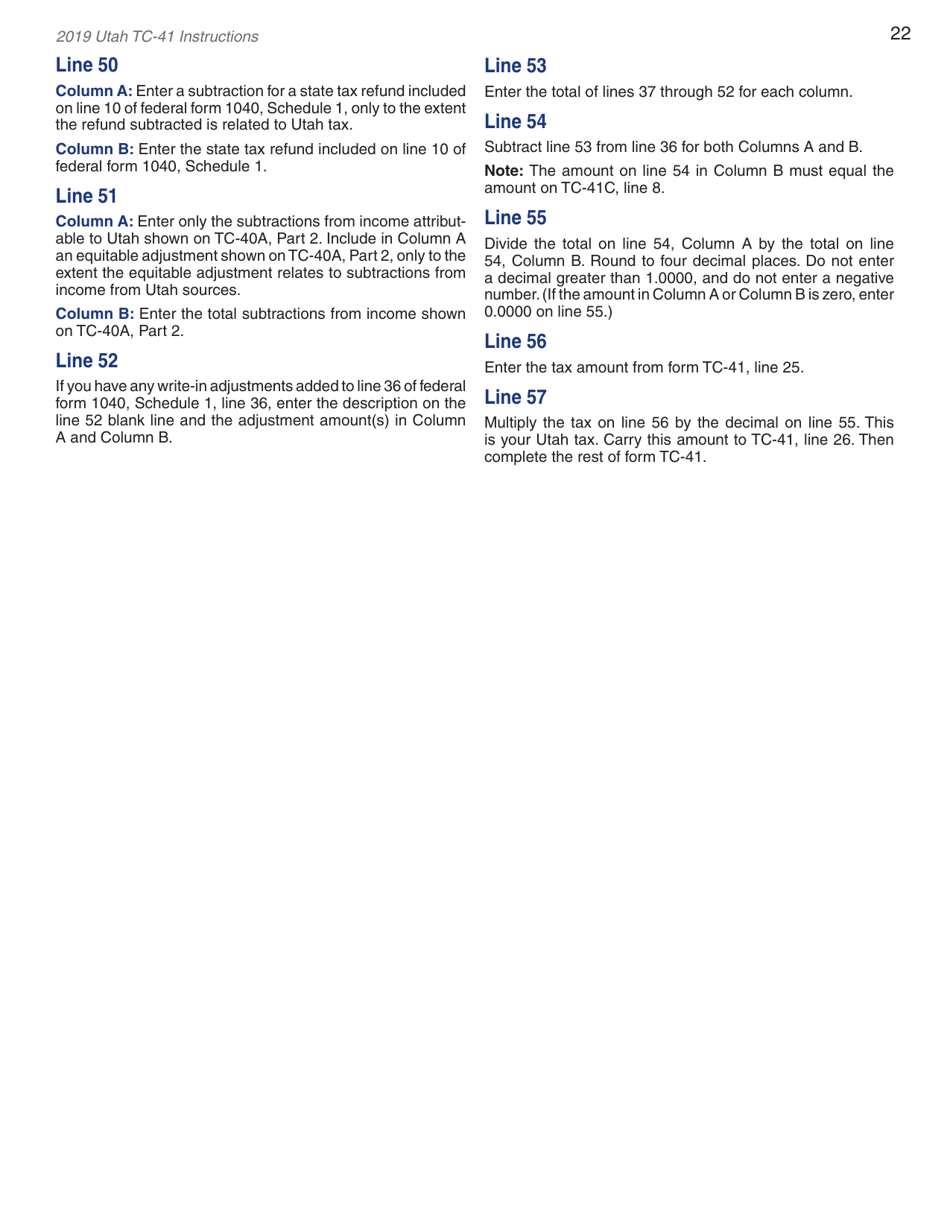

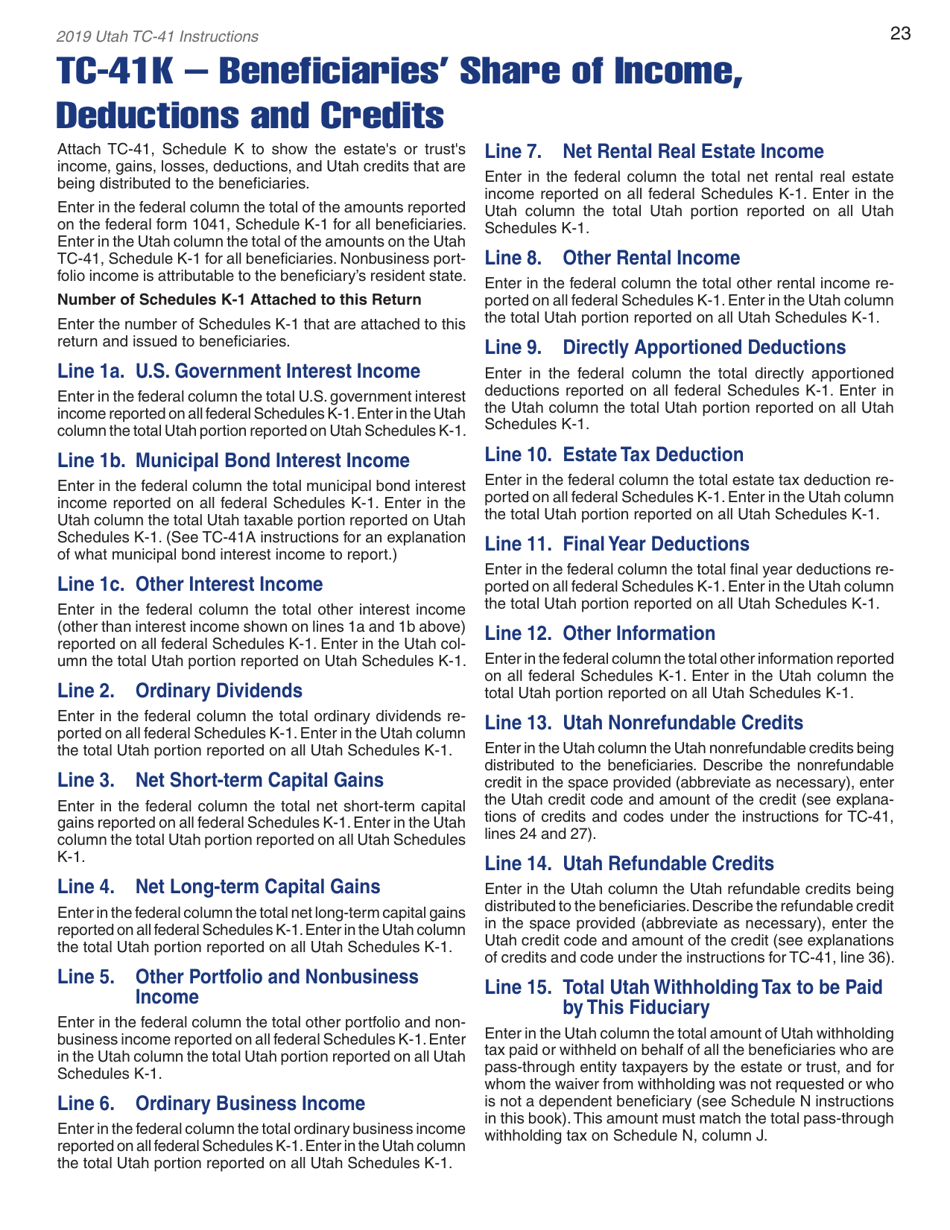

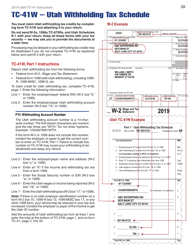

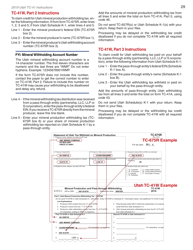

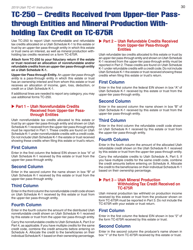

Instructions for Form TC-41 Utah Fiduciary Income Tax Return - Utah

This document contains official instructions for Form TC-41 , Utah Fiduciary Income Tax Return - a form released and collected by the Utah State Tax Commission.

FAQ

Q: What is Form TC-41?

A: Form TC-41 is the Utah Fiduciary Income Tax Return.

Q: Who needs to file Form TC-41?

A: Fiduciaries, such as executors, administrators, trustees, and guardians, who have taxable income from a trust or estate in Utah need to file Form TC-41.

Q: When is the deadline to file Form TC-41?

A: The deadline to file Form TC-41 is the same as the federal income tax deadline, which is typically April 15th.

Q: Is there an extension available for filing Form TC-41?

A: Yes, you can request an extension to file Form TC-41. The extension gives you an additional 6 months to file the return.

Q: What information do I need to complete Form TC-41?

A: You will need information such as the trust or estate's income, deductions, credits, and any withholding taxes.

Q: Are there any additional forms or schedules that need to be attached to Form TC-41?

A: Depending on your specific situation, you may need to attach additional forms or schedules, such as Schedule A for itemized deductions.

Q: What if I have questions or need assistance filling out Form TC-41?

A: If you have questions or need assistance, you can contact the Utah State Tax Commission or consult with a tax professional.

Instruction Details:

- This 34-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Utah State Tax Commission.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34