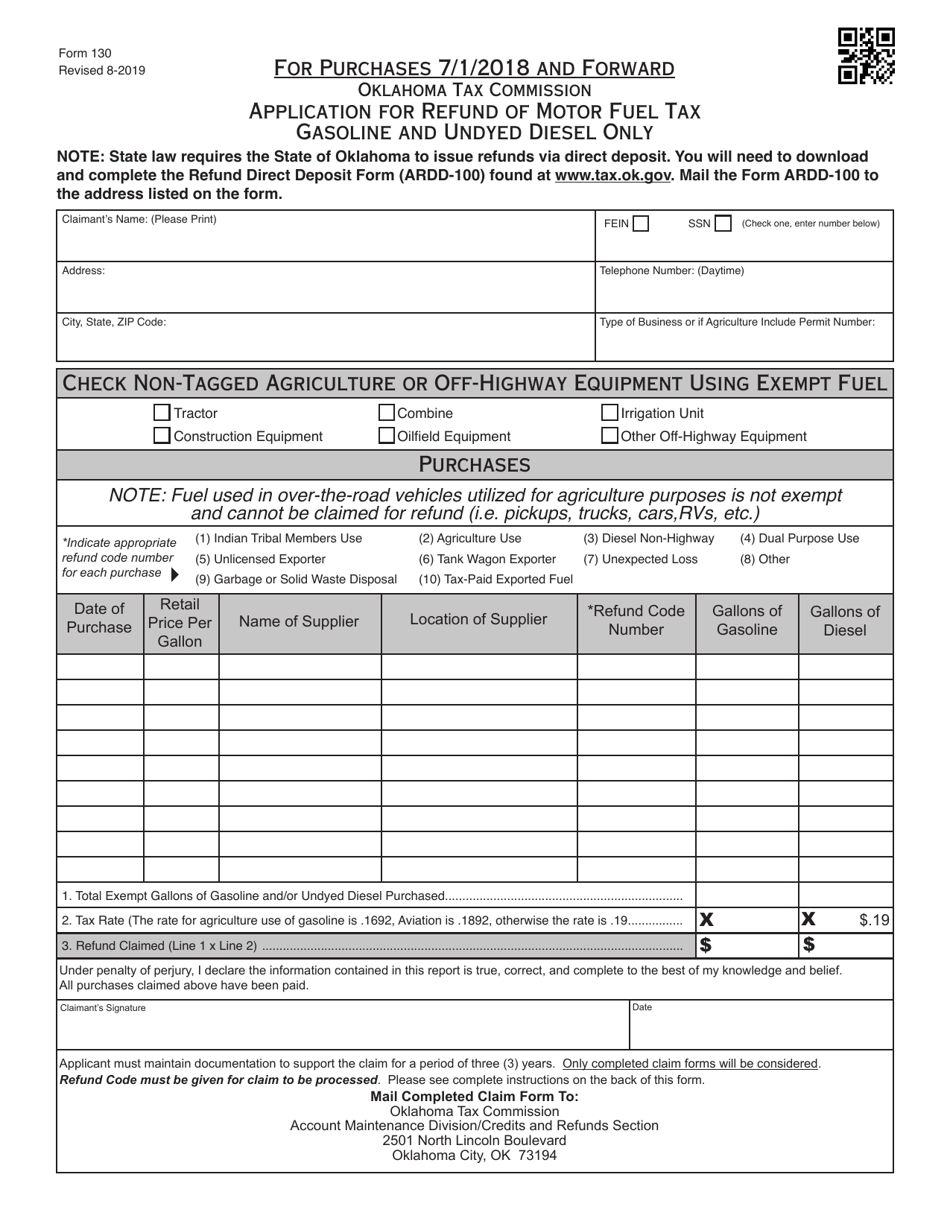

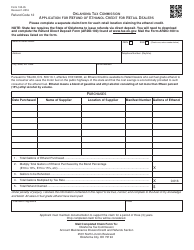

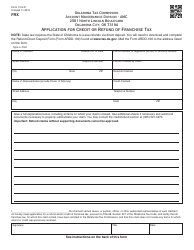

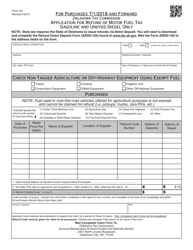

Form 130 Application for Refund of Motor Fuel Tax - Gasoline and Undyed Diesel Only (For Purchases July 1, 2018 and Forward) - Oklahoma

What Is Form 130?

This is a legal form that was released by the Oklahoma Tax Commission - a government authority operating within Oklahoma. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is form 130?

A: Form 130 is the Application for Refund of Motor Fuel Tax for gasoline and undyed diesel.

Q: What is the purpose of form 130?

A: The purpose of form 130 is to apply for a refund of motor fuel tax on gasoline and undyed diesel purchased in Oklahoma.

Q: Who is eligible to use form 130?

A: Anyone who has purchased gasoline or undyed diesel in Oklahoma after July 1, 2018, is eligible to use form 130 to apply for a refund.

Q: What purchases does form 130 apply to?

A: Form 130 applies to purchases of gasoline and undyed diesel made in Oklahoma after July 1, 2018.

Q: When should I submit form 130?

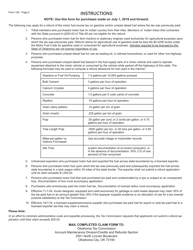

A: Form 130 should be submitted within one year from the date of purchase.

Q: What documentation is required to accompany form 130?

A: Documentation such as fuel receipts and proof of payment is required to accompany form 130.

Q: How long does it take to receive a refund using form 130?

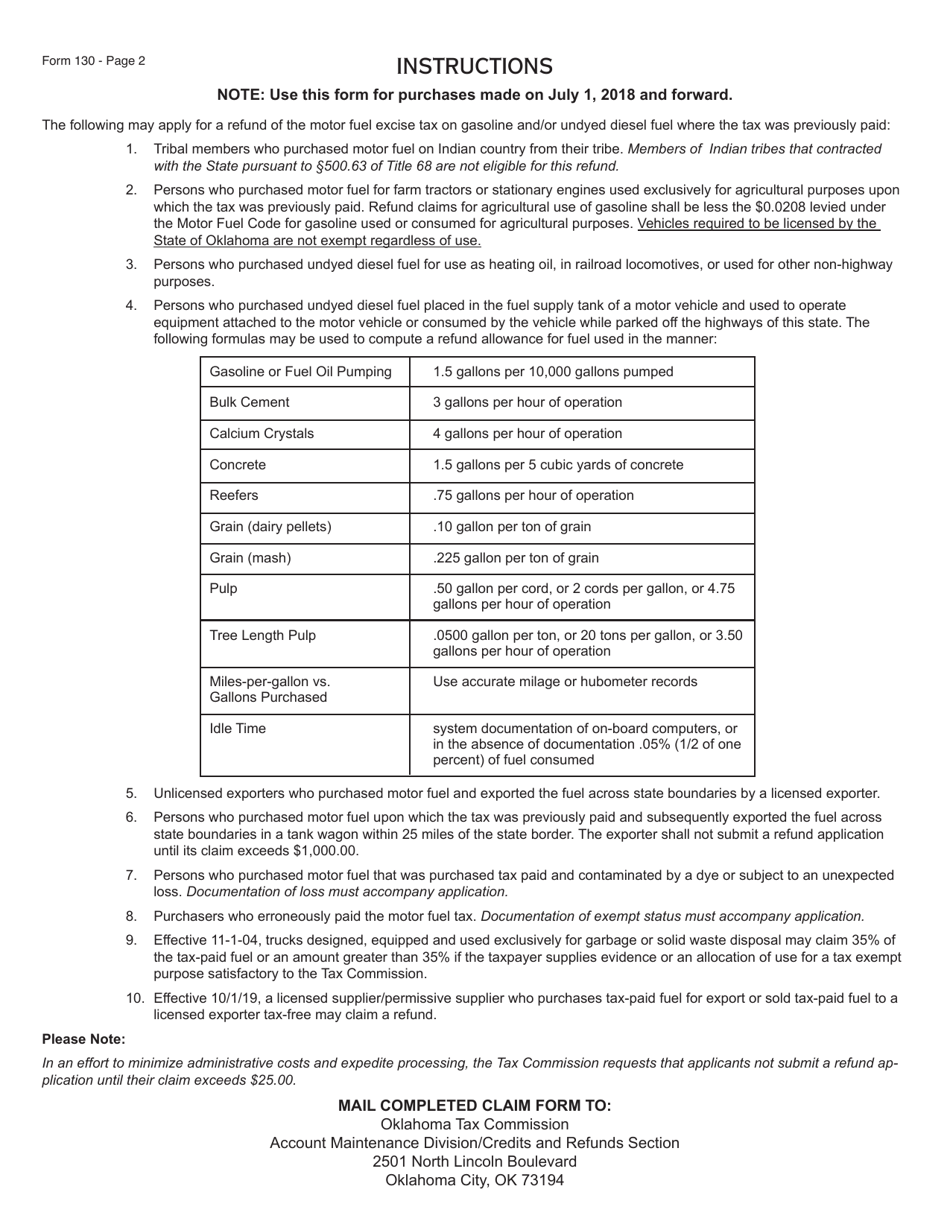

A: The processing time for a refund application using form 130 is typically 45 days.

Q: Can I file form 130 electronically?

A: Yes, the Oklahoma Tax Commission allows for electronic filing of form 130.

Q: What should I do if I have more questions about form 130?

A: If you have more questions about form 130, you can contact the Oklahoma Tax Commission for assistance.

Form Details:

- Released on August 1, 2019;

- The latest edition provided by the Oklahoma Tax Commission;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 130 by clicking the link below or browse more documents and templates provided by the Oklahoma Tax Commission.

Download Form 130 Application for Refund of Motor Fuel Tax - Gasoline and Undyed Diesel Only (For Purchases July 1, 2018 and Forward) - Oklahoma

1

2

3