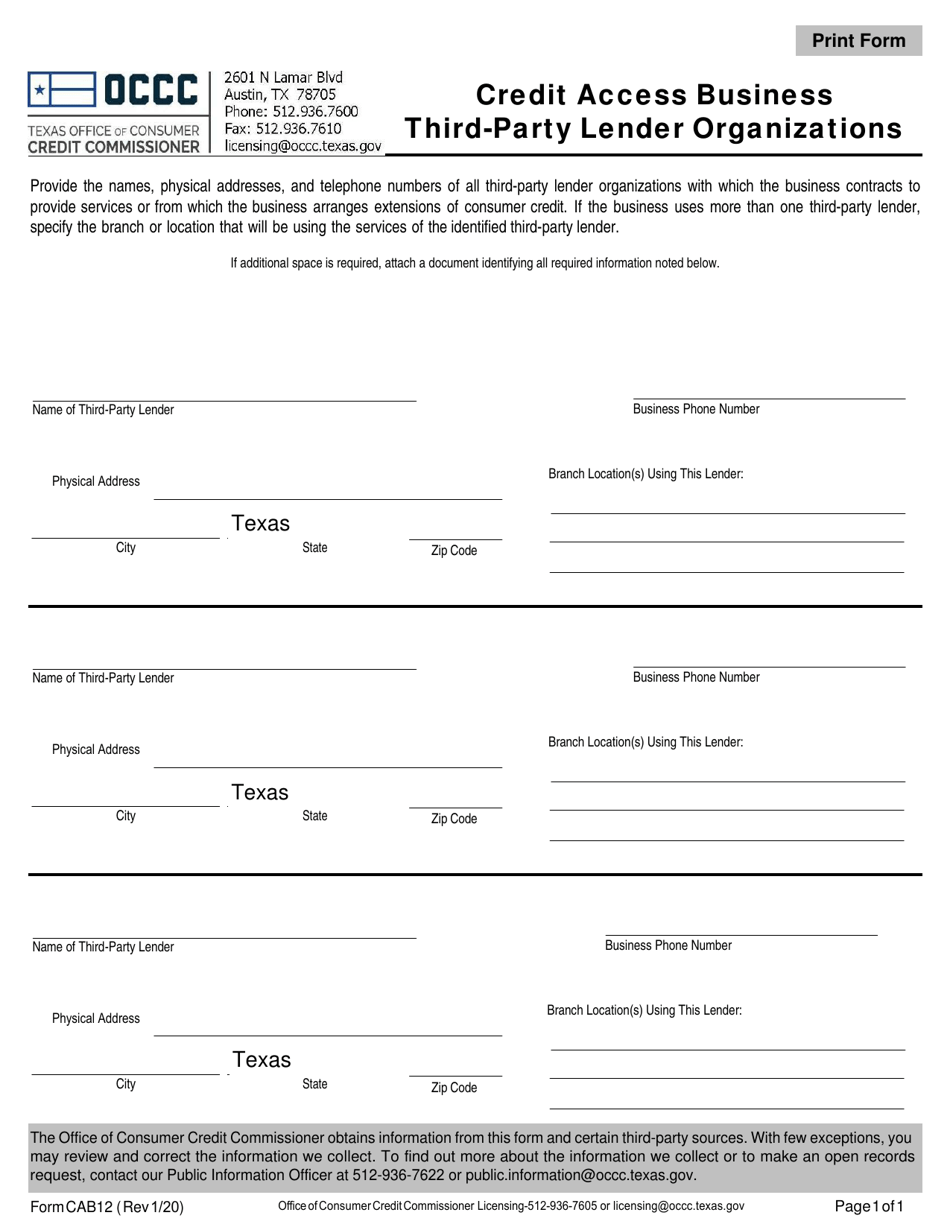

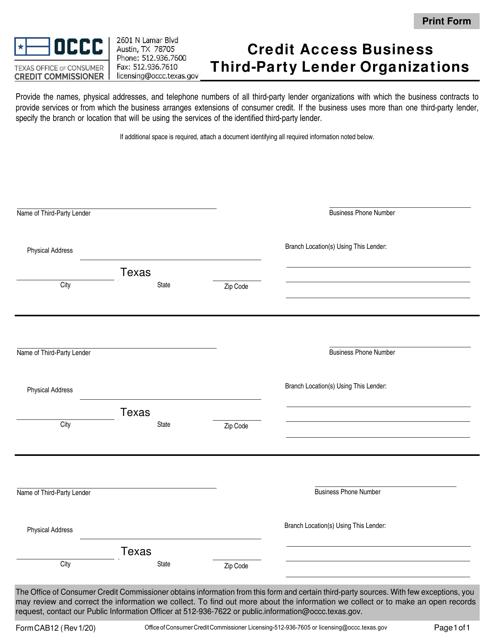

Form CAB12 Credit Access Business Third-Party Lender Organizations - Texas

What Is Form CAB12?

This is a legal form that was released by the Texas Office of Consumer Credit Commissioner - a government authority operating within Texas. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is a CAB?

A: CAB stands for Credit Access Business.

Q: What is a Third-Party Lender Organization?

A: A Third-Party Lender Organization is a type of business that provides loans through a Credit Access Business (CAB).

Q: What does a CAB do?

A: A CAB facilitates loans by connecting borrowers with third-party lenders.

Q: Are CABs regulated in Texas?

A: Yes, CABs are regulated in Texas.

Q: What are the requirements for a CAB license in Texas?

A: To obtain a CAB license in Texas, a business must meet specific criteria including financial requirements and operational guidelines.

Q: Can CABs charge high interest rates?

A: Yes, CABs can charge high interest rates on loans.

Q: What should I be aware of when using a CAB?

A: When using a CAB, be aware of the high interest rates and fees associated with the loans.

Q: Is there a limit on the loan amounts CABs can offer?

A: Yes, there is a limit on the loan amounts that CABs can offer in Texas.

Q: Are there any consumer protections for borrowers using CABs?

A: Yes, Texas has consumer protections in place for borrowers using CABs, including loan disclosure requirements and the right to cancel a loan within a certain time period.

Form Details:

- Released on January 1, 2020;

- The latest edition provided by the Texas Office of Consumer Credit Commissioner;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CAB12 by clicking the link below or browse more documents and templates provided by the Texas Office of Consumer Credit Commissioner.