![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CT-501

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CT-501

for the current year.

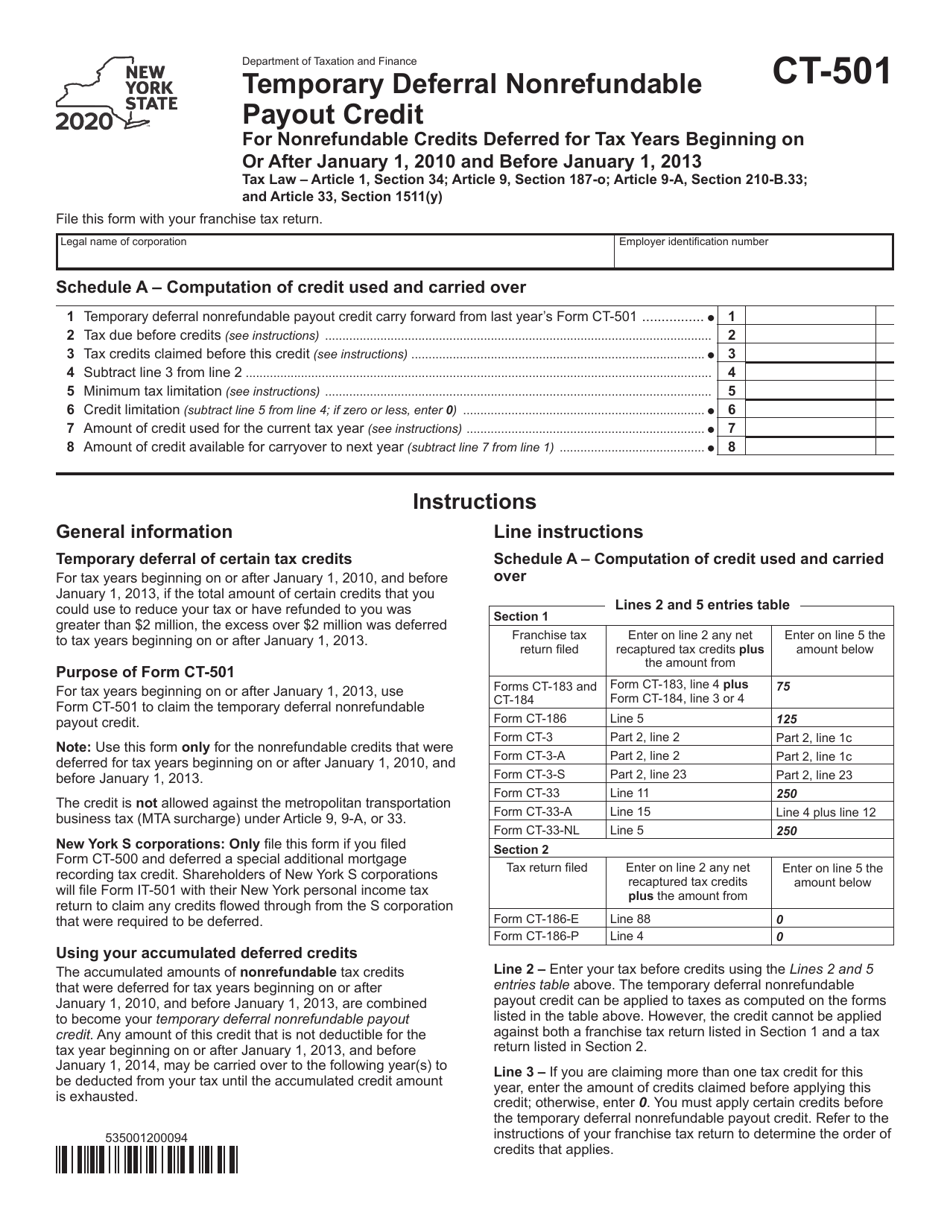

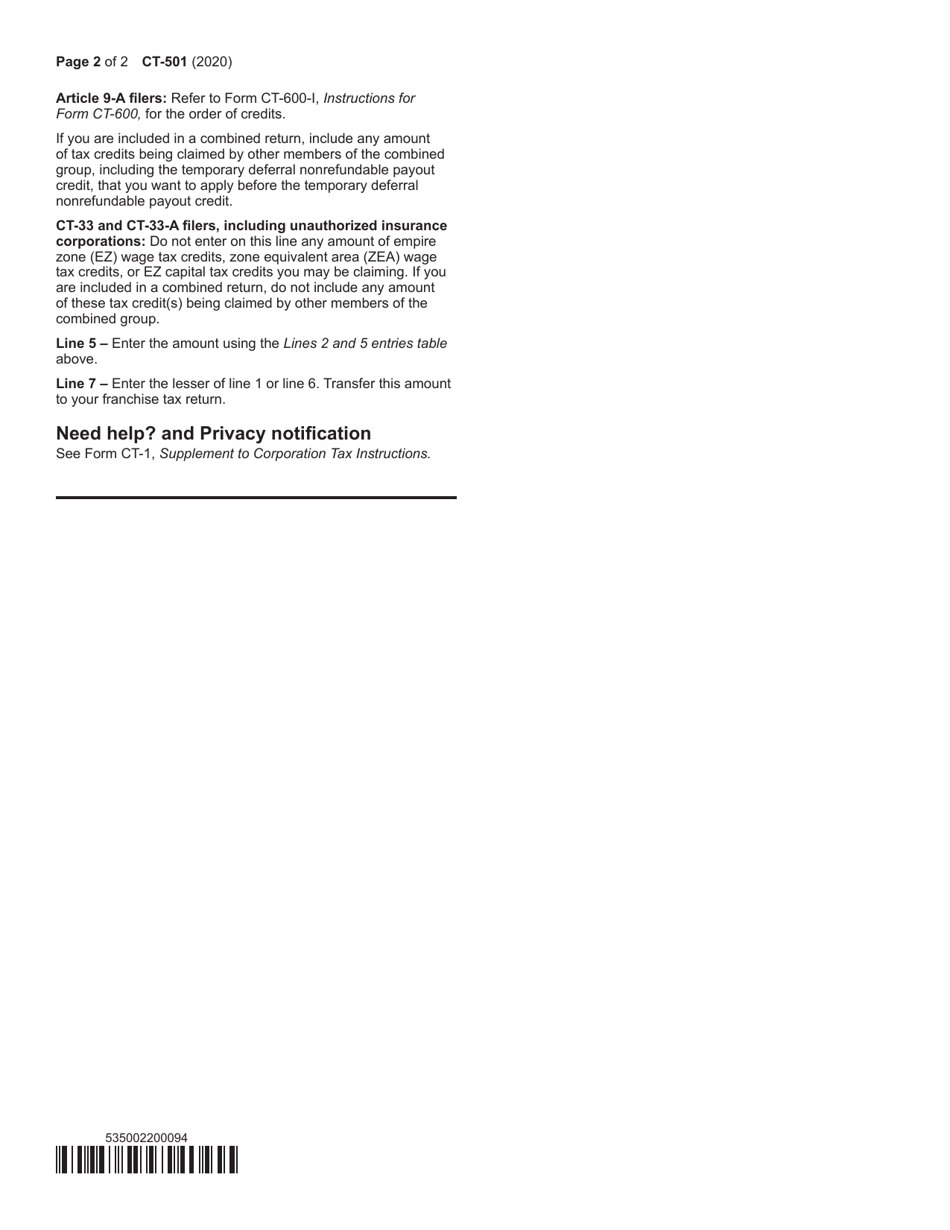

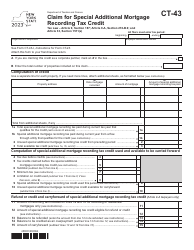

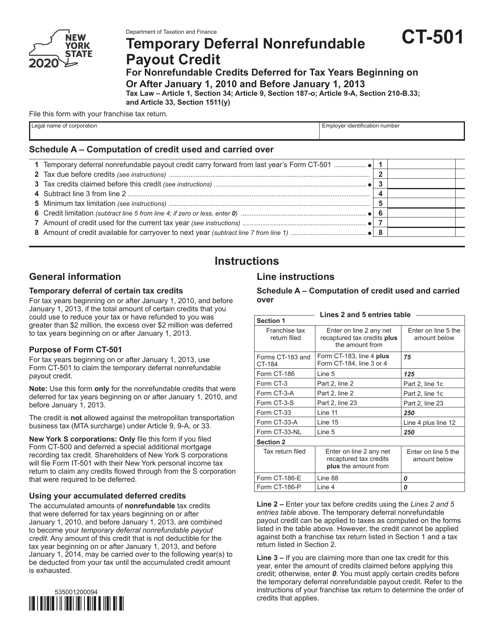

Form CT-501 Temporary Deferral Nonrefundable Payout Credit for Nonrefundable Credits Deferred for Tax Years Beginning on or After January 1, 2010 and Before January 1, 2013 - New York

What Is Form CT-501?

This is a legal form that was released by the New York State Department of Taxation and Finance - a government authority operating within New York. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CT-501?

A: Form CT-501 is a form used for the Temporary Deferral Nonrefundable Payout Credit for Nonrefundable Credits Deferred for Tax Years beginning on or after January 1, 2010 and before January 1, 2013 in New York.

Q: What is the purpose of Form CT-501?

A: The purpose of Form CT-501 is to claim a temporary deferral nonrefundable payout credit for nonrefundable credits deferred for specific tax years.

Q: When should Form CT-501 be filed?

A: Form CT-501 should be filed for tax years beginning on or after January 1, 2010 and before January 1, 2013.

Q: Who is eligible to use Form CT-501?

A: Taxpayers who deferred nonrefundable credits for tax years within the specified period are eligible to use Form CT-501.

Q: Is Form CT-501 refundable?

A: No, Form CT-501 is not refundable.

Q: How do I fill out Form CT-501?

A: Form CT-501 requires you to provide information about the deferred nonrefundable credits and calculate the nonrefundable payout credit.

Q: Are there any special instructions for completing Form CT-501?

A: Yes, there are specific instructions provided on the form itself. It is important to read and follow these instructions carefully.

Q: Does Form CT-501 apply to both New York and non-New York residents?

A: Yes, Form CT-501 applies to both New York residents and non-residents who have deferred nonrefundable credits within the specified tax years.

Q: What happens after I file Form CT-501?

A: After filing Form CT-501, the New York State Department of Taxation and Finance will review your claim and process your nonrefundable payout credit accordingly.

Form Details:

- The latest edition provided by the New York State Department of Taxation and Finance;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form CT-501 by clicking the link below or browse more documents and templates provided by the New York State Department of Taxation and Finance.

Download Form CT-501 Temporary Deferral Nonrefundable Payout Credit for Nonrefundable Credits Deferred for Tax Years Beginning on or After January 1, 2010 and Before January 1, 2013 - New York

1

2