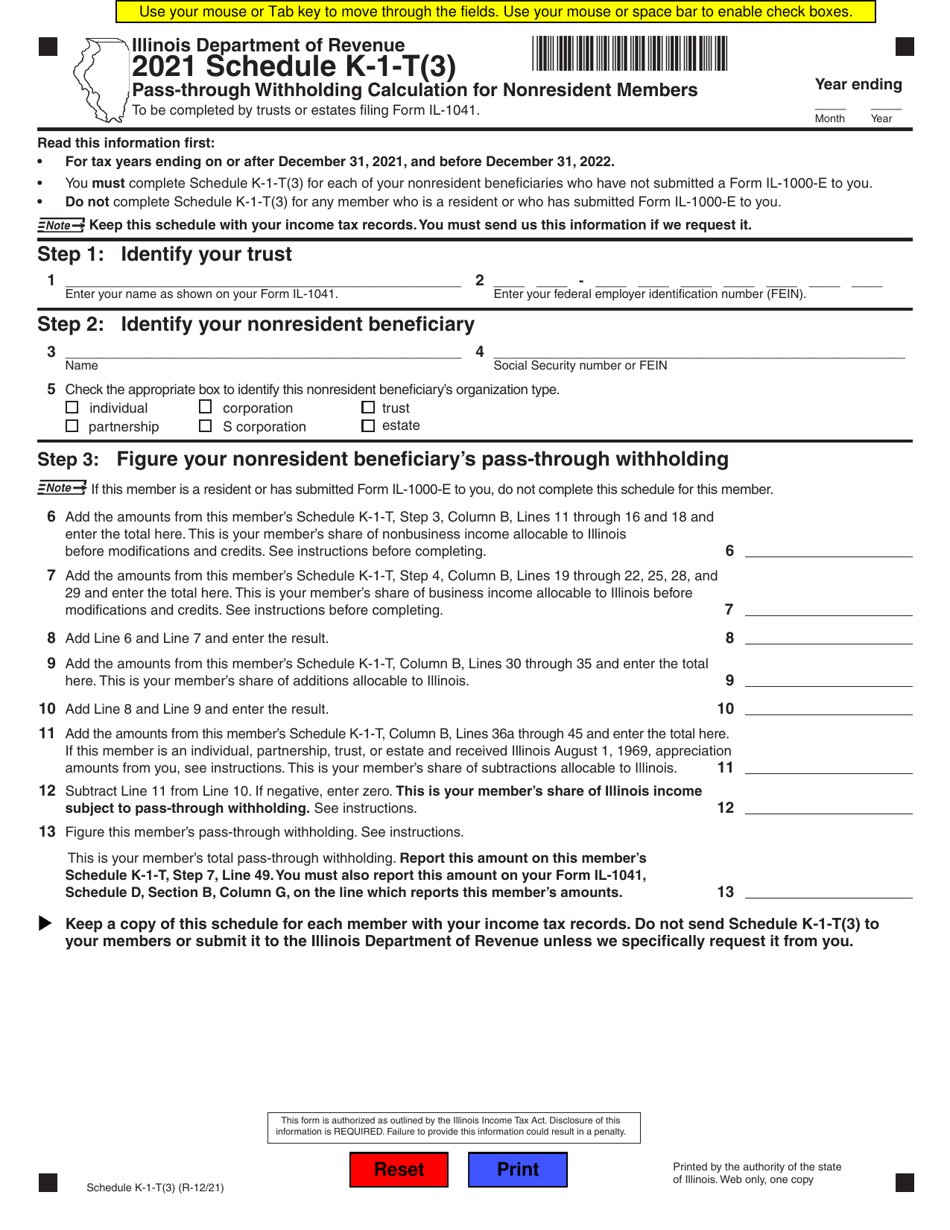

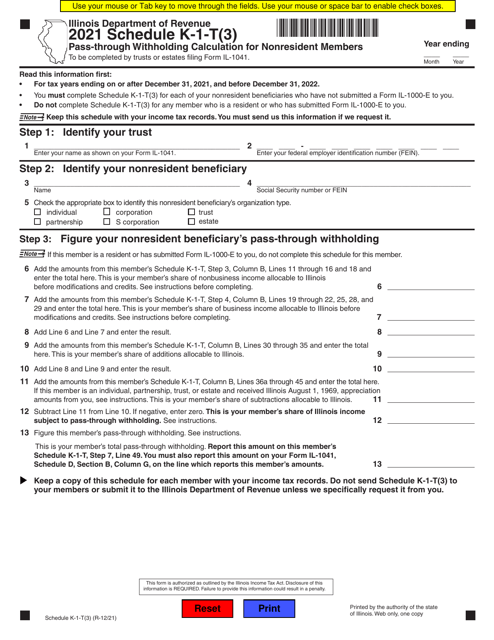

Schedule K-1-T(3) Pass-Through Withholding Calculation for Nonresident Members - Illinois

What Is Schedule K-1-T(3)?

This is a legal form that was released by the Illinois Department of Revenue - a government authority operating within Illinois. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Schedule K-1-T(3)?

A: Schedule K-1-T(3) is a tax form used to calculate pass-through withholding for nonresident members.

Q: Who uses Schedule K-1-T(3)?

A: Schedule K-1-T(3) is used by nonresident members in Illinois.

Q: What is pass-through withholding?

A: Pass-through withholding is a mechanism to collect taxes on income distributed to nonresident members of a partnership or LLC.

Q: Why is pass-through withholding calculation necessary?

A: Pass-through withholding calculation is necessary to ensure compliance with tax laws and to accurately report and pay taxes on income distributed to nonresident members.

Q: What information is required for pass-through withholding calculation on Schedule K-1-T(3)?

A: The information required for pass-through withholding calculation on Schedule K-1-T(3) includes the nonresident member's share of Illinois taxable income or loss, the applicable withholding rate, and any other relevant information as required by the form.

Q: How is pass-through withholding calculated?

A: Pass-through withholding is calculated by multiplying the nonresident member's share of Illinois taxable income or loss by the applicable withholding rate.

Q: What is the purpose of pass-through withholding for nonresident members?

A: The purpose of pass-through withholding for nonresident members is to ensure that taxes are paid on income distributed to them, even if they are not residents of Illinois.

Q: Are there any exemptions or exceptions to pass-through withholding for nonresident members?

A: Yes, there may be exemptions or exceptions to pass-through withholding for nonresident members, depending on their specific circumstances and any applicable tax laws or regulations.

Q: Is pass-through withholding calculation the final tax liability for nonresident members?

A: No, pass-through withholding calculation is not the final tax liability for nonresident members. It is an estimated amount of tax to be withheld and reported, and the nonresident member may still have additional tax obligations based on their overall tax situation.

Form Details:

- Released on December 1, 2021;

- The latest edition provided by the Illinois Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Schedule K-1-T(3) by clicking the link below or browse more documents and templates provided by the Illinois Department of Revenue.