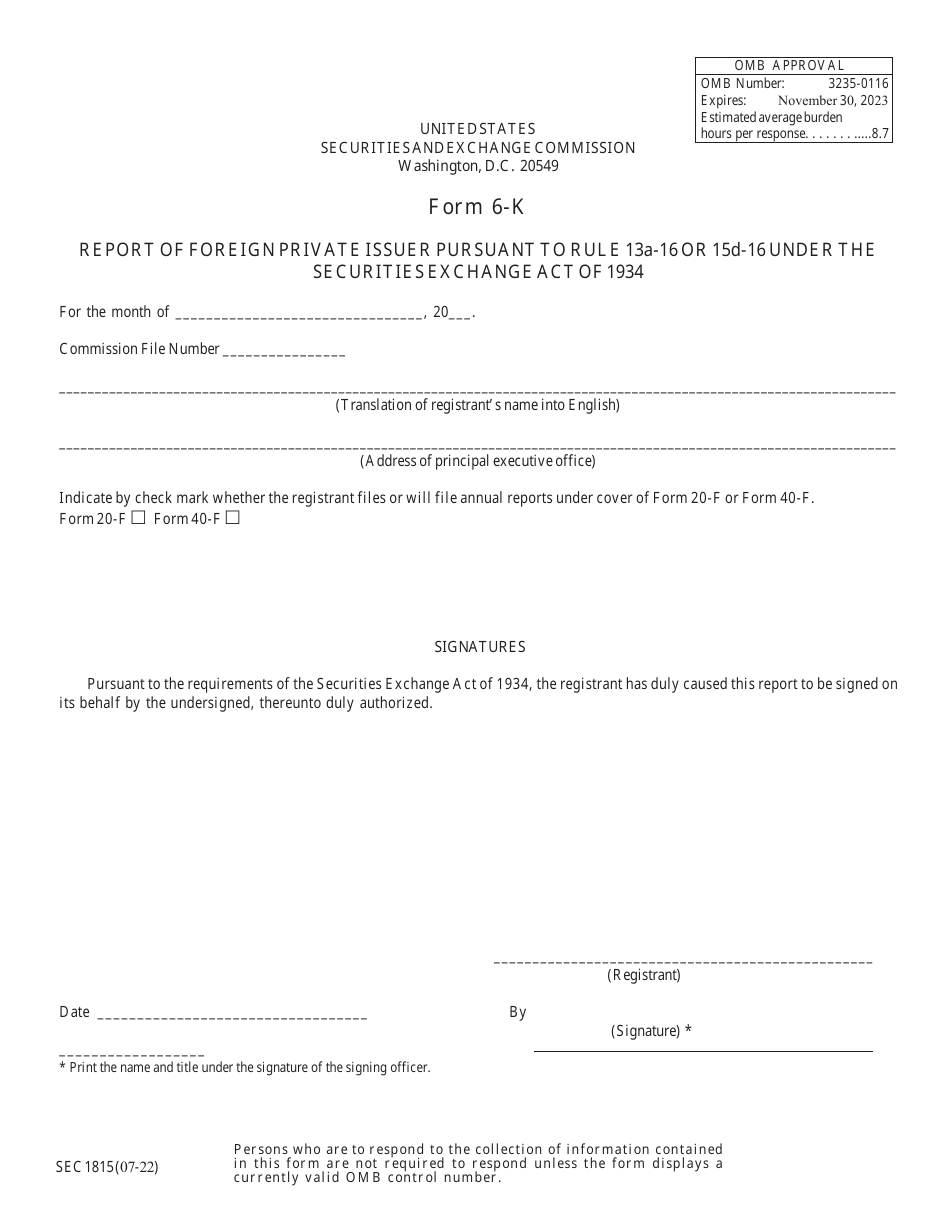

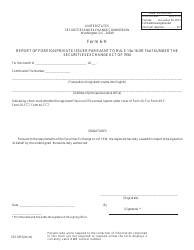

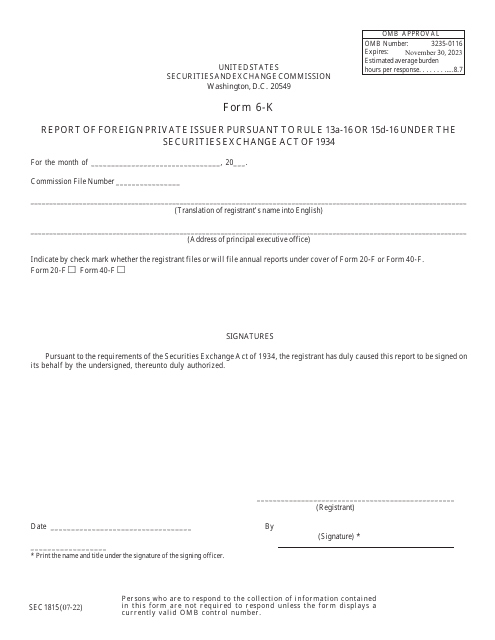

SEC Form 1815 (6-K) Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 Under the Securities Exchange Act of 1934

What Is SEC Form 1815 (6-K)?

This is a legal form that was released by the U.S. Securities and Exchange Commission on July 1, 2022 and used country-wide. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is SEC Form 1815 (6-K)?

A: SEC Form 1815 (6-K) is a report filed by a foreign private issuer with the Securities and Exchange Commission (SEC) pursuant to Rule 13a-16 or 15d-16 of the Securities Exchange Act of 1934.

Q: Who is required to file SEC Form 1815 (6-K)?

A: Foreign private issuers are required to file SEC Form 1815 (6-K) if they meet the reporting requirements under Rule 13a-16 or 15d-16 of the Securities Exchange Act of 1934.

Q: What information is included in SEC Form 1815 (6-K)?

A: SEC Form 1815 (6-K) includes information about the financial condition and operations of the foreign private issuer, as well as any material information that needs to be disclosed to the SEC.

Q: Why is SEC Form 1815 (6-K) important?

A: SEC Form 1815 (6-K) is important because it provides transparency and disclosure of information from foreign private issuers to the SEC and investors in the United States.

Q: What is the purpose of Rule 13a-16 or 15d-16?

A: Rule 13a-16 or 15d-16 requires foreign private issuers to meet certain reporting obligations, including the filing of SEC Form 1815 (6-K), to ensure transparency in the U.S. securities markets.

Q: Is SEC Form 1815 (6-K) only applicable to foreign private issuers?

A: Yes, SEC Form 1815 (6-K) is specifically designed for foreign private issuers who are subject to the reporting requirements under Rule 13a-16 or 15d-16.

Form Details:

- Released on July 1, 2022;

- The latest available edition released by the U.S. Securities and Exchange Commission;

- Easy to use and ready to print;

- Yours to fill out and keep for your records;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of SEC Form 1815 (6-K) by clicking the link below or browse more documents and templates provided by the U.S. Securities and Exchange Commission.

Download SEC Form 1815 (6-K) Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 Under the Securities Exchange Act of 1934

1

2

3

4