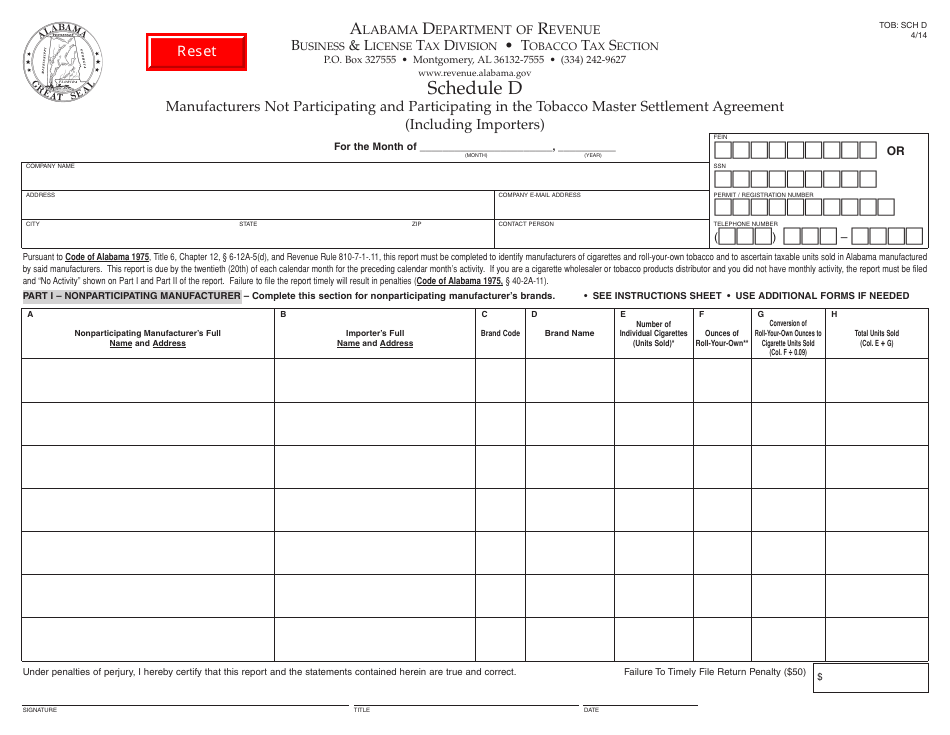

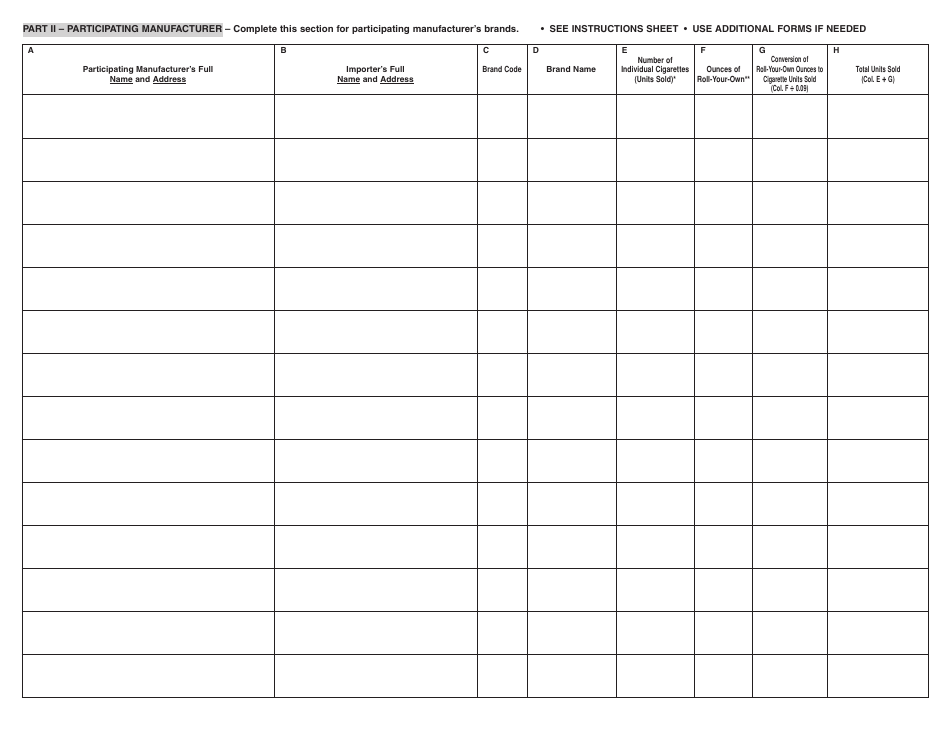

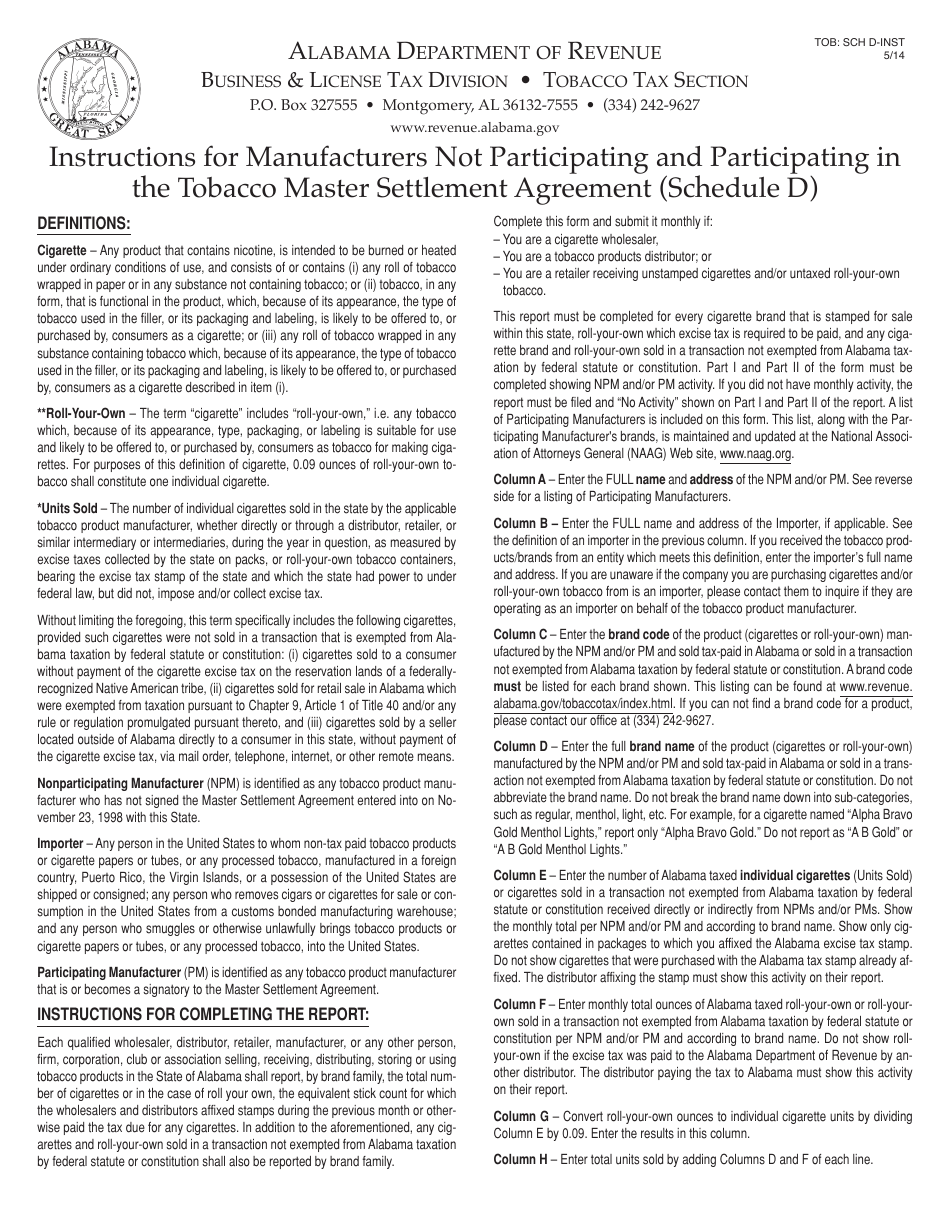

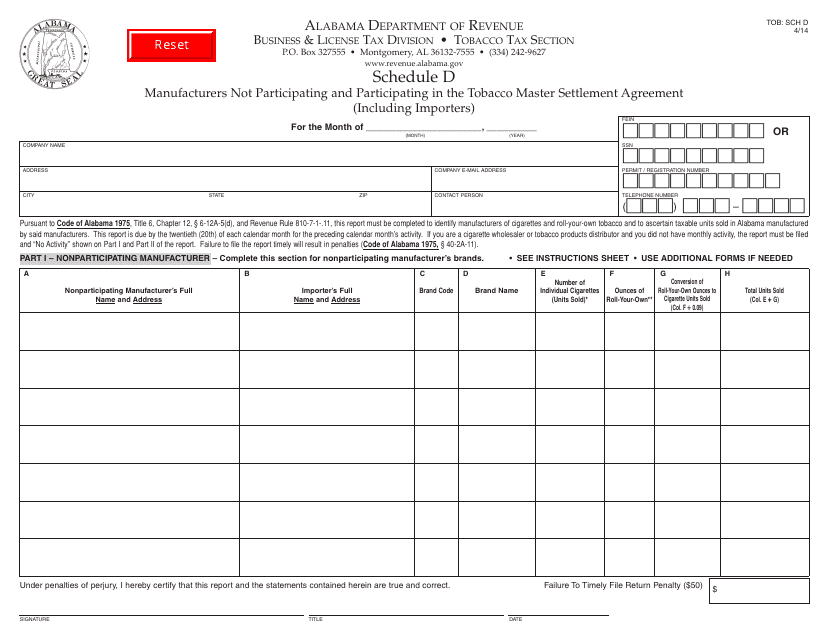

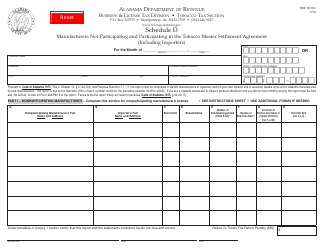

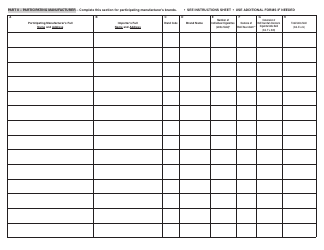

Schedule D Manufacturers Not Participating in the Tobacco Master Settlement Agreement (Including Importers) - Alabama

What Is Schedule D?

This is a legal form that was released by the Alabama Department of Revenue - a government authority operating within Alabama. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the Tobacco Master Settlement Agreement?

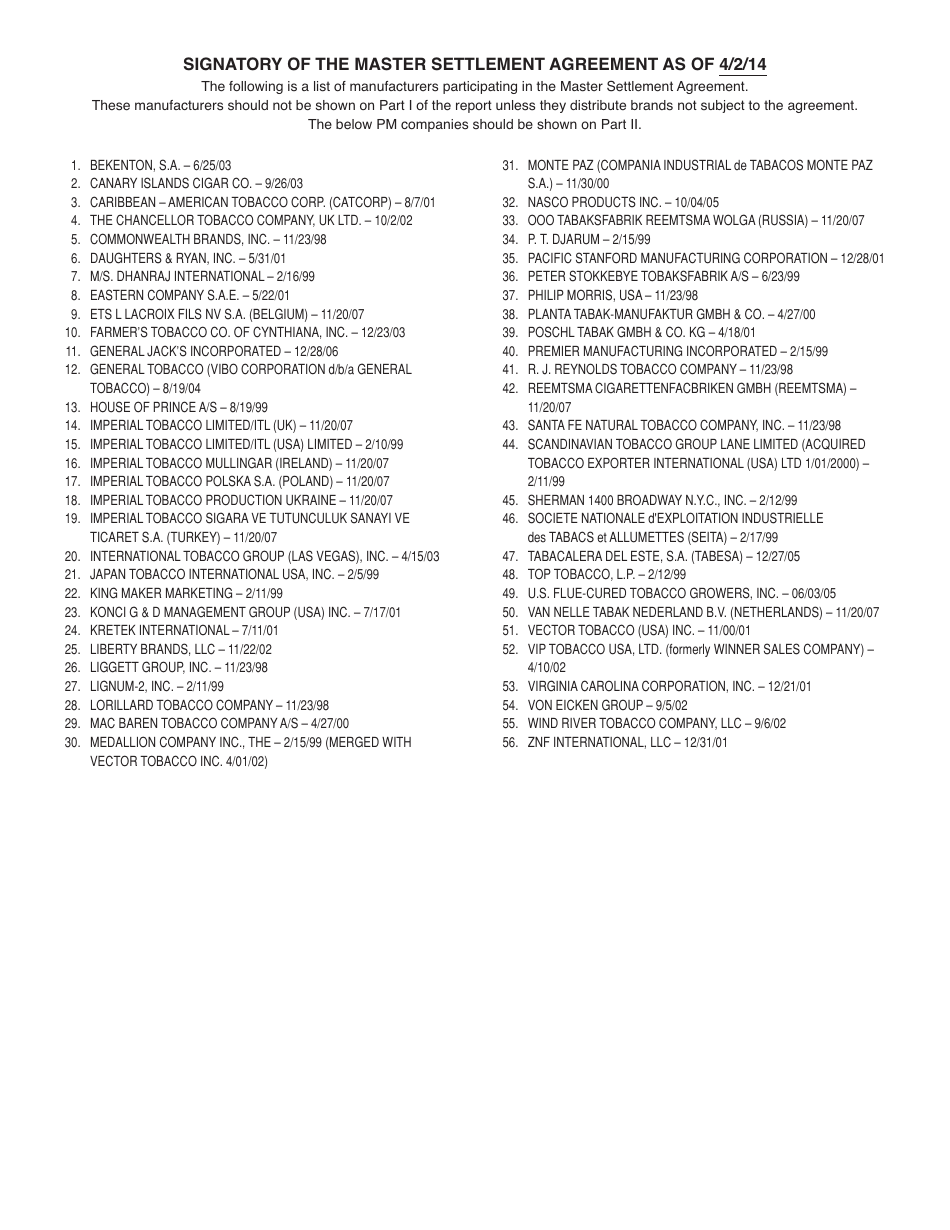

A: The Tobacco Master Settlement Agreement is an agreement reached in 1998 between the major tobacco companies and 46 U.S. states, including Alabama, to settle lawsuits related to the health costs associated with tobacco use.

Q: What is Schedule D?

A: Schedule D is a list of manufacturers, including importers, who are not participating in the Tobacco Master Settlement Agreement.

Q: Why are some manufacturers not participating in the agreement?

A: Some manufacturers may choose not to participate in the agreement for various reasons, such as having a different business model or not meeting the criteria set by the agreement.

Q: How does the agreement affect tobacco use?

A: The agreement requires participating manufacturers to make annual payments to the states to compensate for the health costs related to tobacco use. It also includes restrictions on marketing and advertising practices.

Q: What happens if a manufacturer is not part of the agreement?

A: Manufacturers not participating in the agreement are not required to make the same payments or follow the same marketing restrictions. However, they are still subject to other tobacco regulations and may face legal consequences for non-compliance.

Form Details:

- Released on April 1, 2014;

- The latest edition provided by the Alabama Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Schedule D by clicking the link below or browse more documents and templates provided by the Alabama Department of Revenue.

Download Schedule D Manufacturers Not Participating in the Tobacco Master Settlement Agreement (Including Importers) - Alabama

1

2

3

4