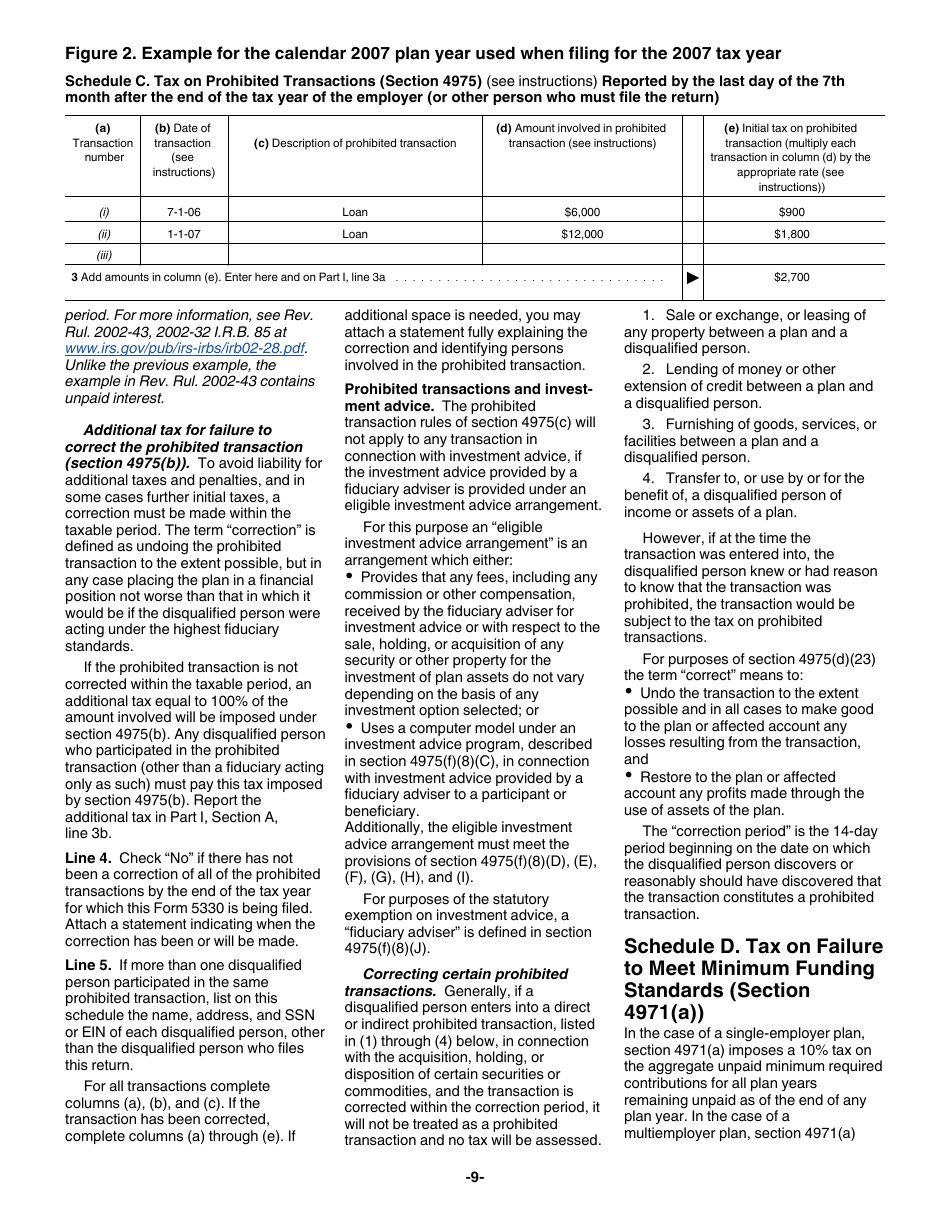

![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 5330

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 5330

for the current year.

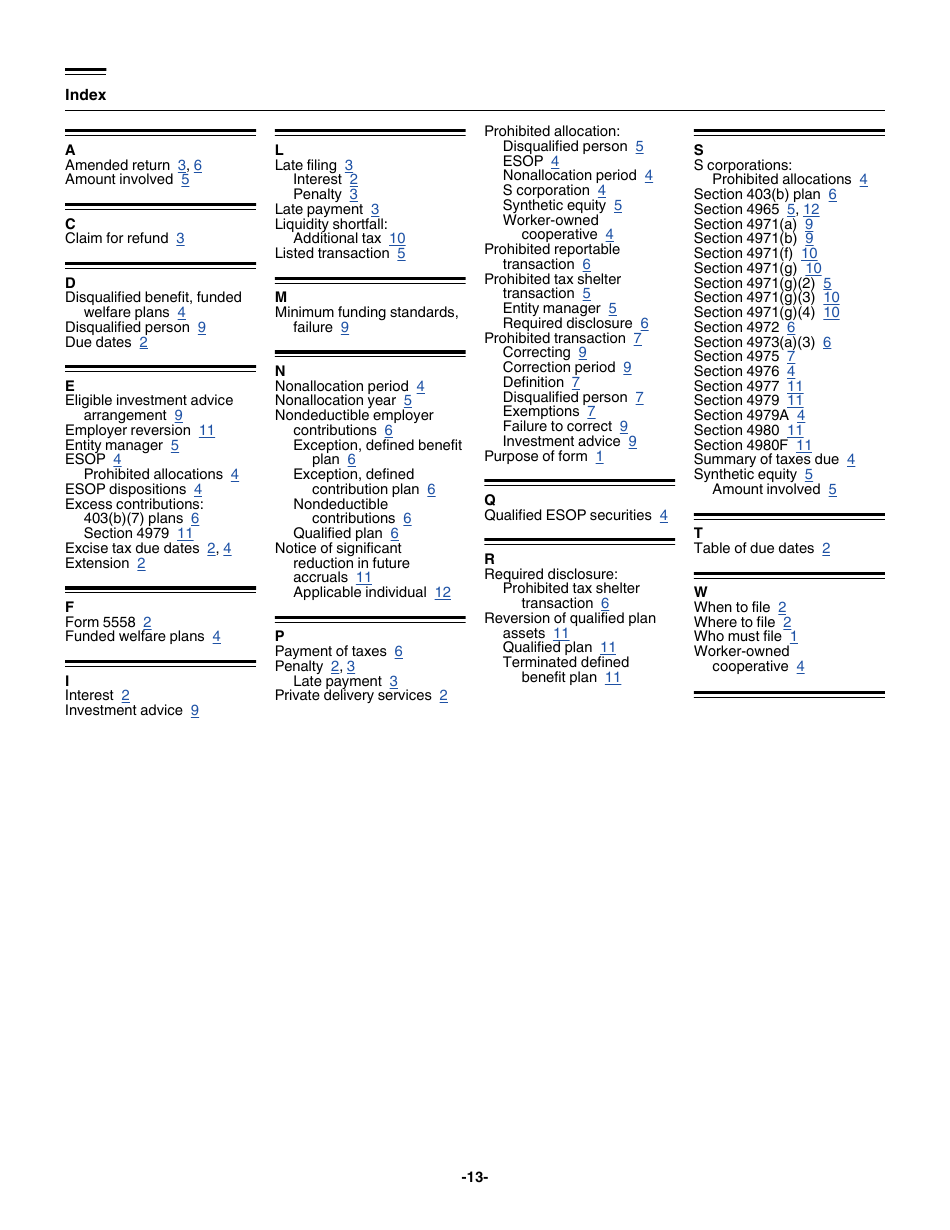

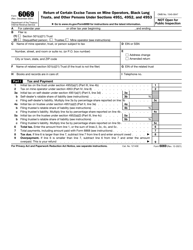

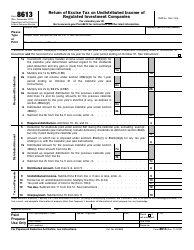

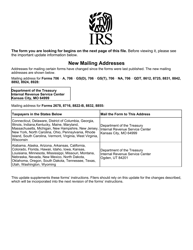

Instructions for IRS Form 5330 Return of Excise Taxes Related to Employee Benefit Plans

This document contains official instructions for IRS Form 5330 , Return of Excise Taxes Related to Employee Benefit Plans - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 5330 is available for download through this link.

FAQ

Q: What is IRS Form 5330?

A: IRS Form 5330 is used to report and pay excise taxes related to employee benefit plans.

Q: What are excise taxes related to employee benefit plans?

A: Excise taxes related to employee benefit plans are taxes imposed on certain prohibited transactions or failures to meet certain requirements under the Internal Revenue Code.

Q: Who needs to file IRS Form 5330?

A: Employers who have engaged in transactions or actions that result in excise taxes related to their employee benefit plans must file IRS Form 5330.

Q: What information is required on IRS Form 5330?

A: IRS Form 5330 requires information about the employer, the employee benefit plan, the specific excise tax being reported, and the amount of tax due.

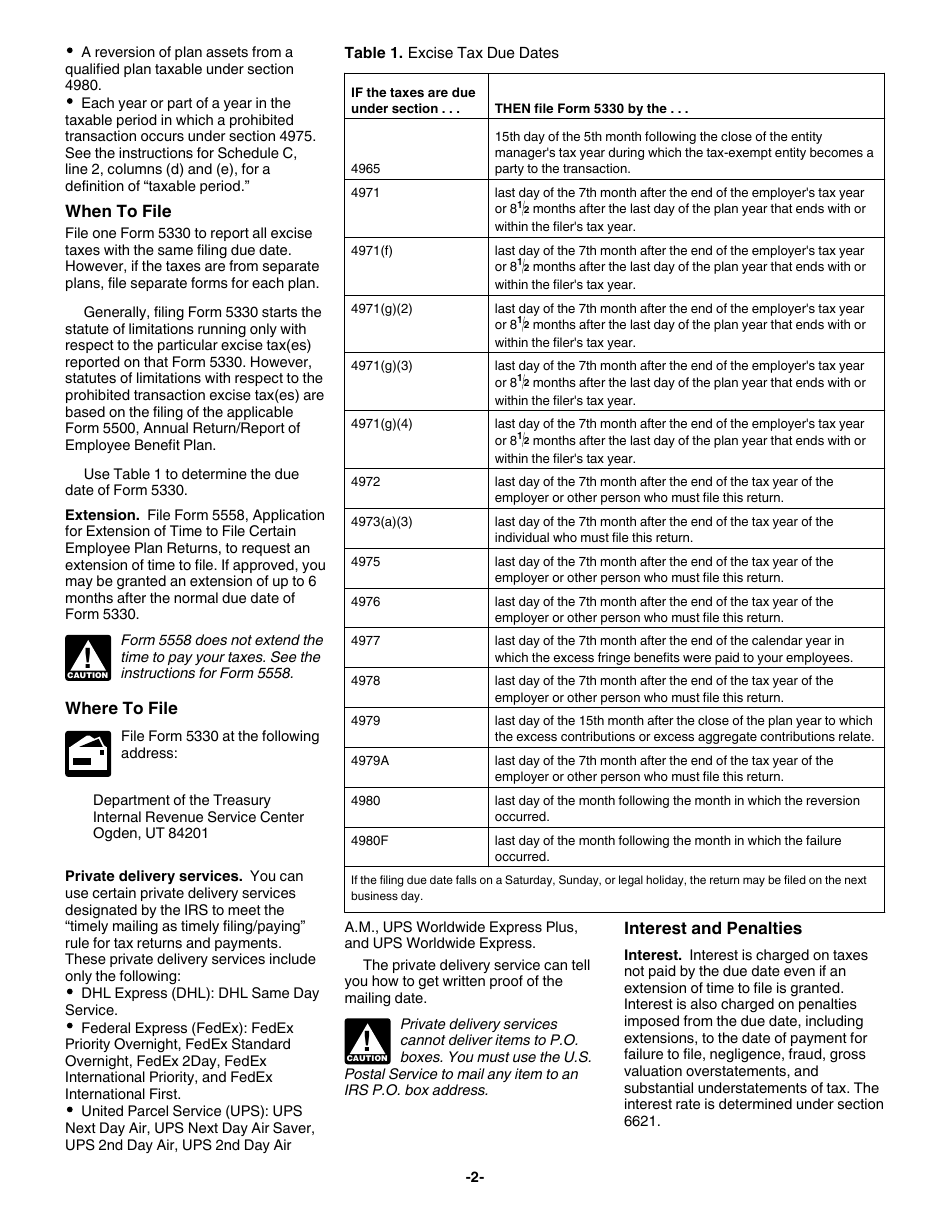

Q: When is IRS Form 5330 due?

A: IRS Form 5330 is generally due by the last day of the seventh month following the end of the employer's tax year.

Q: How can IRS Form 5330 be filed?

A: IRS Form 5330 can be filed electronically using the IRS e-file system or by mail.

Q: Are there any penalties for failing to file IRS Form 5330?

A: Yes, there may be penalties for failure to file IRS Form 5330, including potential monetary penalties and interest on unpaid taxes.

Instruction Details:

- This 13-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 5330 Return of Excise Taxes Related to Employee Benefit Plans

1

2

3

4

5

6

7

8

9

10

11

12

13