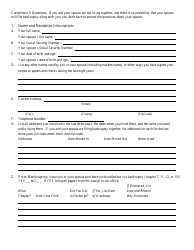

Bankruptcy Questionnaire Template

A Bankruptcy Questionnaire Template is a document used to gather information about a person or a company's financial situation when they file for bankruptcy. It helps collect details about income, expenses, assets, and debts that are necessary for the bankruptcy process.

The bankruptcy questionnaire template is typically completed by the individual or business seeking bankruptcy protection.

FAQ

Q: What is a bankruptcy questionnaire?

A: A bankruptcy questionnaire is a document that helps gather information necessary for filing bankruptcy.

Q: Why is a bankruptcy questionnaire important?

A: A bankruptcy questionnaire is important because it helps gather all the necessary information required for filing bankruptcy.

Q: What information is typically included in a bankruptcy questionnaire?

A: A bankruptcy questionnaire typically includes personal and financial information, such as income, expenses, debts, assets, and personal details.

Q: Do I need to fill out a bankruptcy questionnaire if I hire a bankruptcy attorney?

A: Yes, your bankruptcy attorney will likely ask you to fill out a bankruptcy questionnaire to ensure they have all the necessary information for your case.

Q: Can I fill out the bankruptcy questionnaire on my own?

A: Yes, you can fill out the bankruptcy questionnaire on your own, but it is recommended to seek professional guidance from a bankruptcy attorney.

Q: What should I do if I don't understand a question on the bankruptcy questionnaire?

A: If you don't understand a question on the bankruptcy questionnaire, it is best to consult with your bankruptcy attorney for clarification.

Q: Is it important to be honest when filling out the bankruptcy questionnaire?

A: Yes, it is crucial to be honest when filling out the bankruptcy questionnaire as providing false or incomplete information can have legal consequences.

Q: How long does it typically take to complete a bankruptcy questionnaire?

A: The time it takes to complete a bankruptcy questionnaire can vary depending on the complexity of your financial situation, but it generally takes a few hours to gather and organize the required information.

Q: Can I make changes to my bankruptcy questionnaire after submitting it?

A: It is possible to make changes to your bankruptcy questionnaire after submitting it, but you should consult with your bankruptcy attorney to understand the process and any potential implications.

Download Bankruptcy Questionnaire Template

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

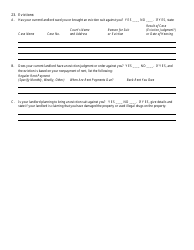

23

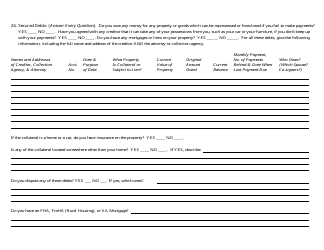

24

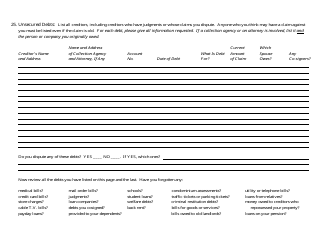

25

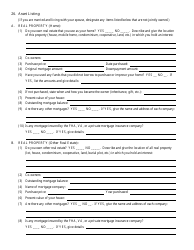

26