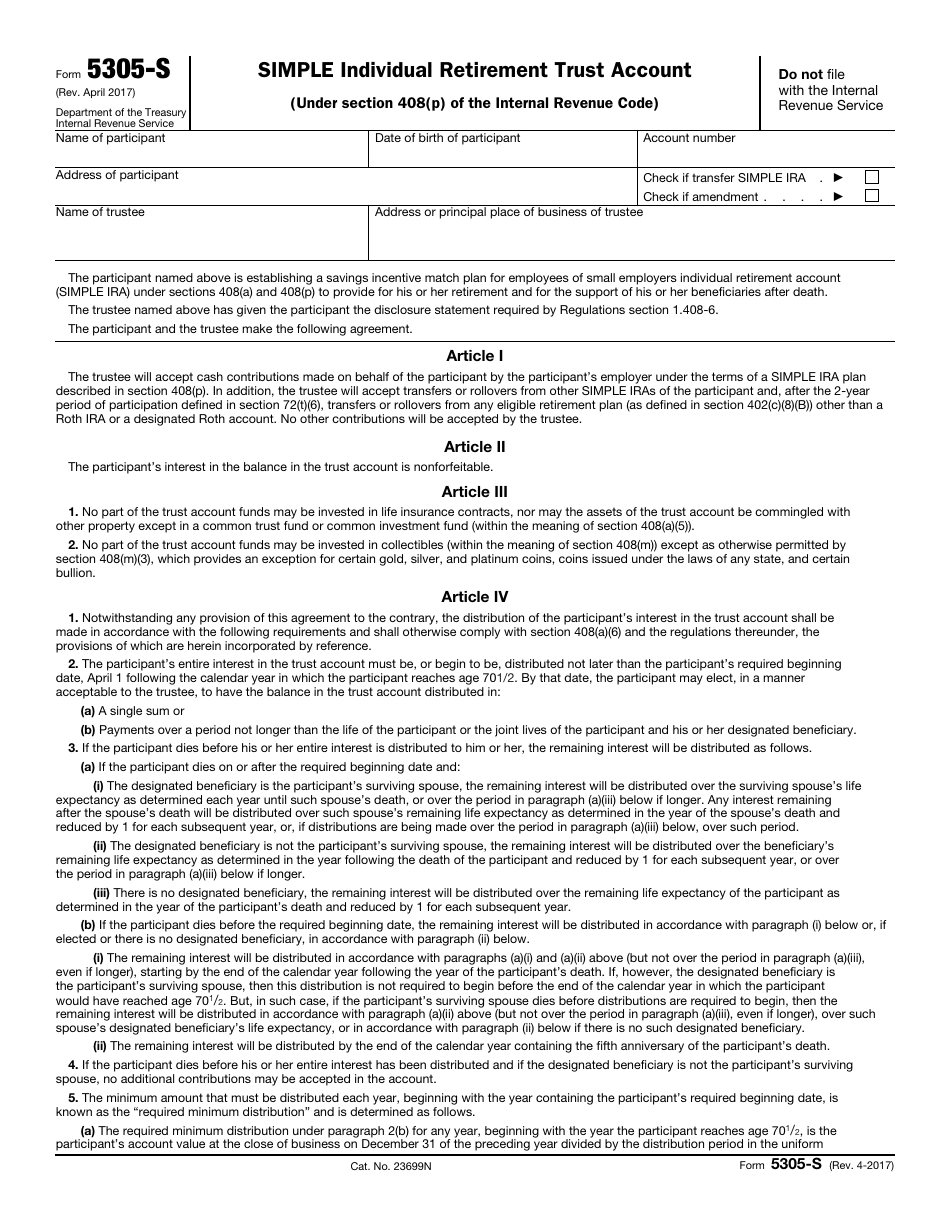

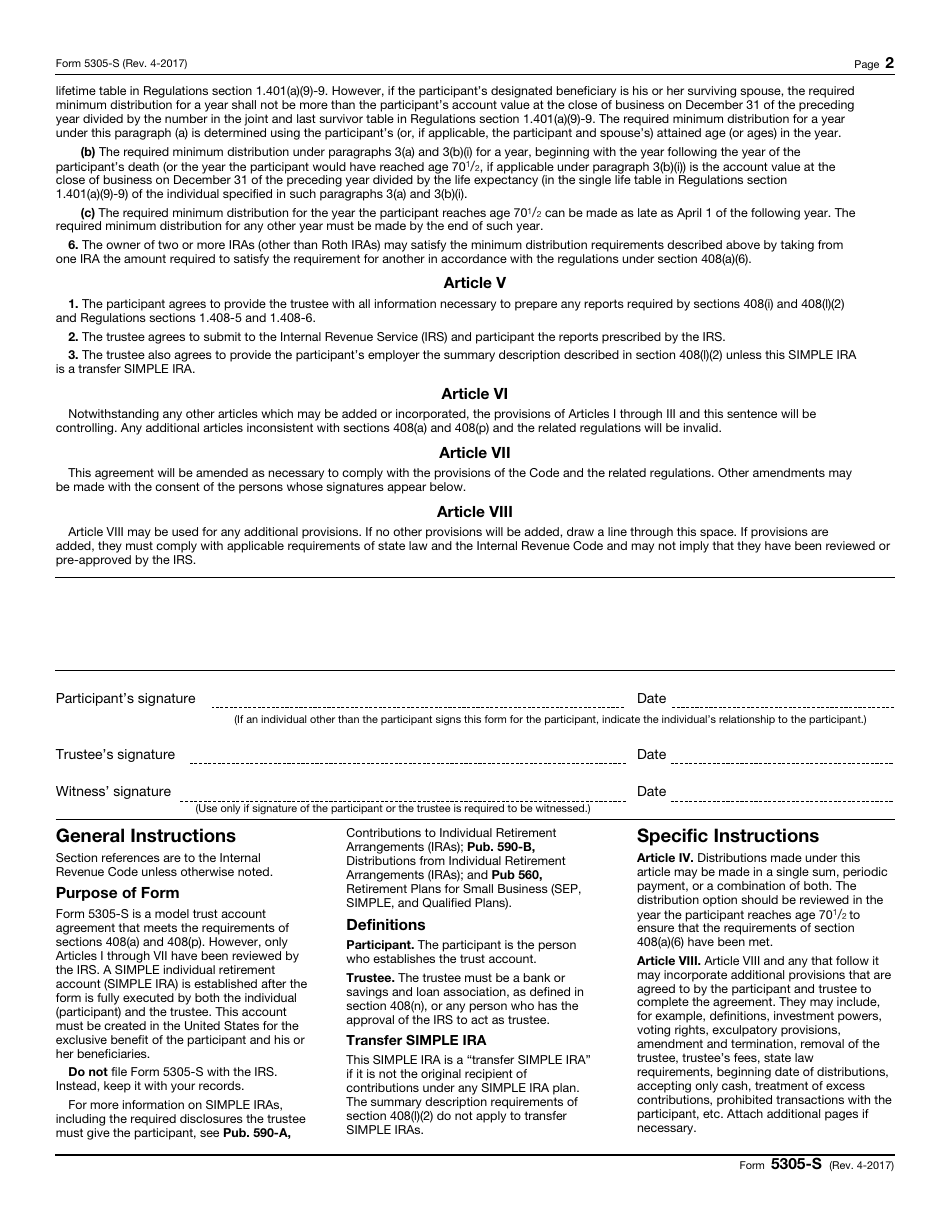

IRS Form 5305-S Simple Individual Retirement Trust Account

Fill PDF Online

Fill out online for free

without registration or credit card

What Is IRS Form 5305-S?

This is a tax form that was released by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury on April 1, 2017. As of today, no separate filing guidelines for the form are provided by the IRS.

Form Details:

- A 2-page form available for download in PDF;

- Actual and valid for filing 2023 taxes;

- Additional instructions and information can be found on page 2 of the document;

- Editable, printable, and free;

- Fill out the form in our online filing application.

Download a fillable version of IRS Form 5305-S through the link below or browse more documents in our library of IRS Forms.

Download IRS Form 5305-S Simple Individual Retirement Trust Account

1

2