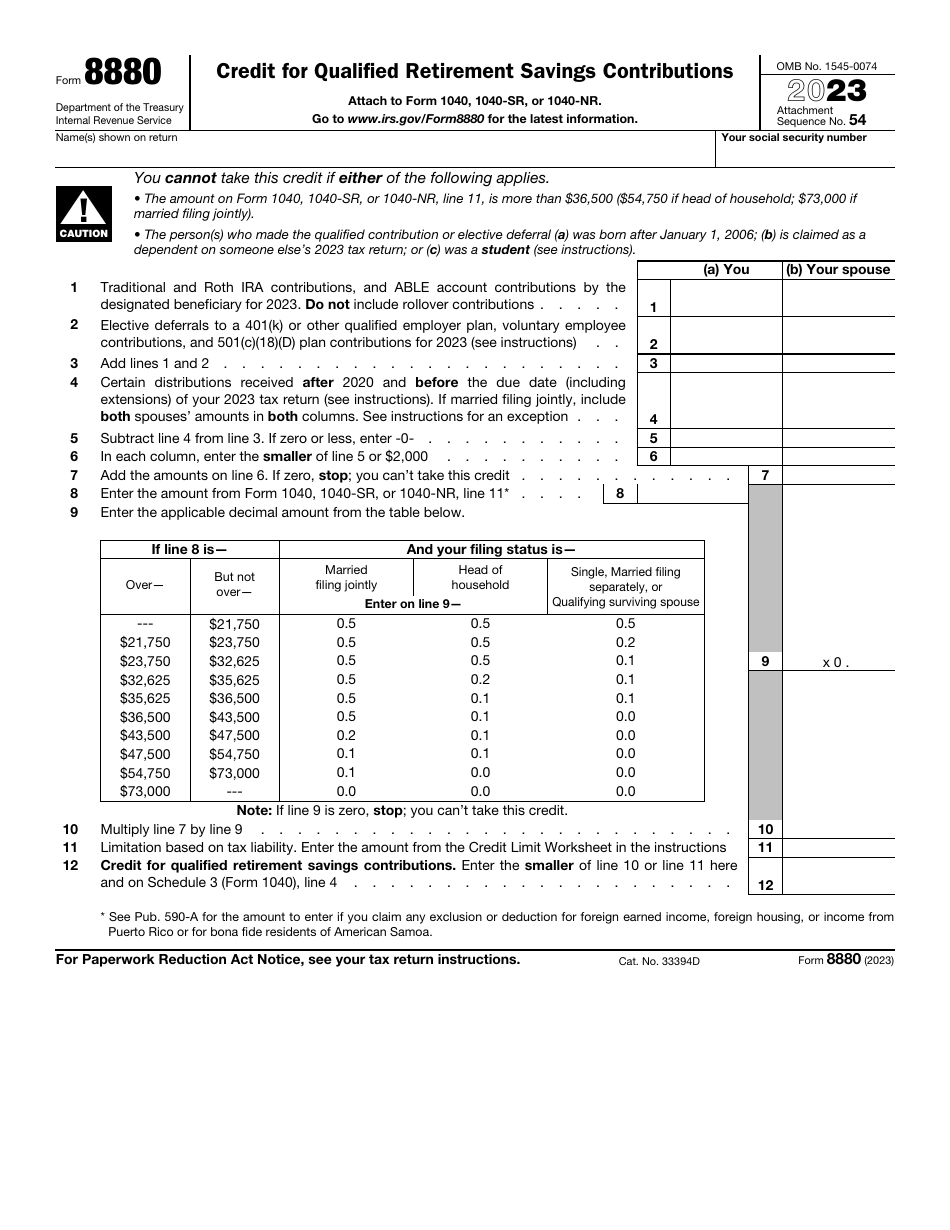

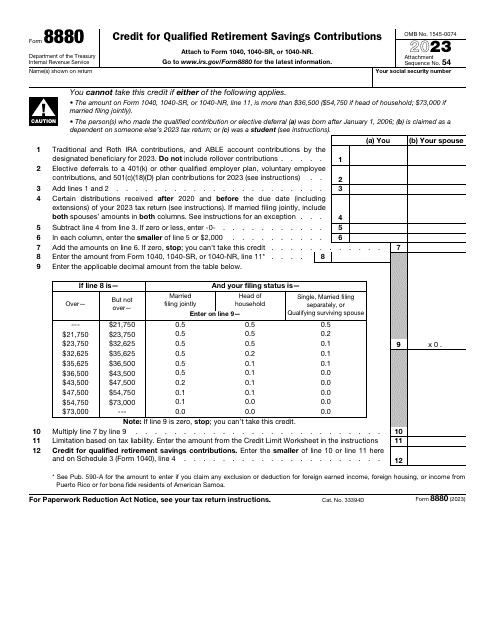

IRS Form 8880 Credit for Qualified Retirement Savings Contributions

What Is Form 8880?

IRS Form 8880, Credit for Qualified Retirement Savings Contributions, is a formal instrument that allows individuals to express their intention to receive a saver's credit after contributing money to their retirement savings plans.

Alternate Names:

- Tax Form 8880;

- Federal Form 8880;

- Saver’s Credit Form.

Any taxpayer that meets the criteria written in the statement is allowed to reach out to tax organs and ask them to reduce the amount of income tax they owe because of the tax credit they qualify for - utilize Form 8880 and lower your tax liability annually as long as you comply with requirements listed in the document.

This application was issued by the Internal Revenue Service (IRS) in 2023, making older editions outdated. You may download an IRS Form 8880 fillable version below.

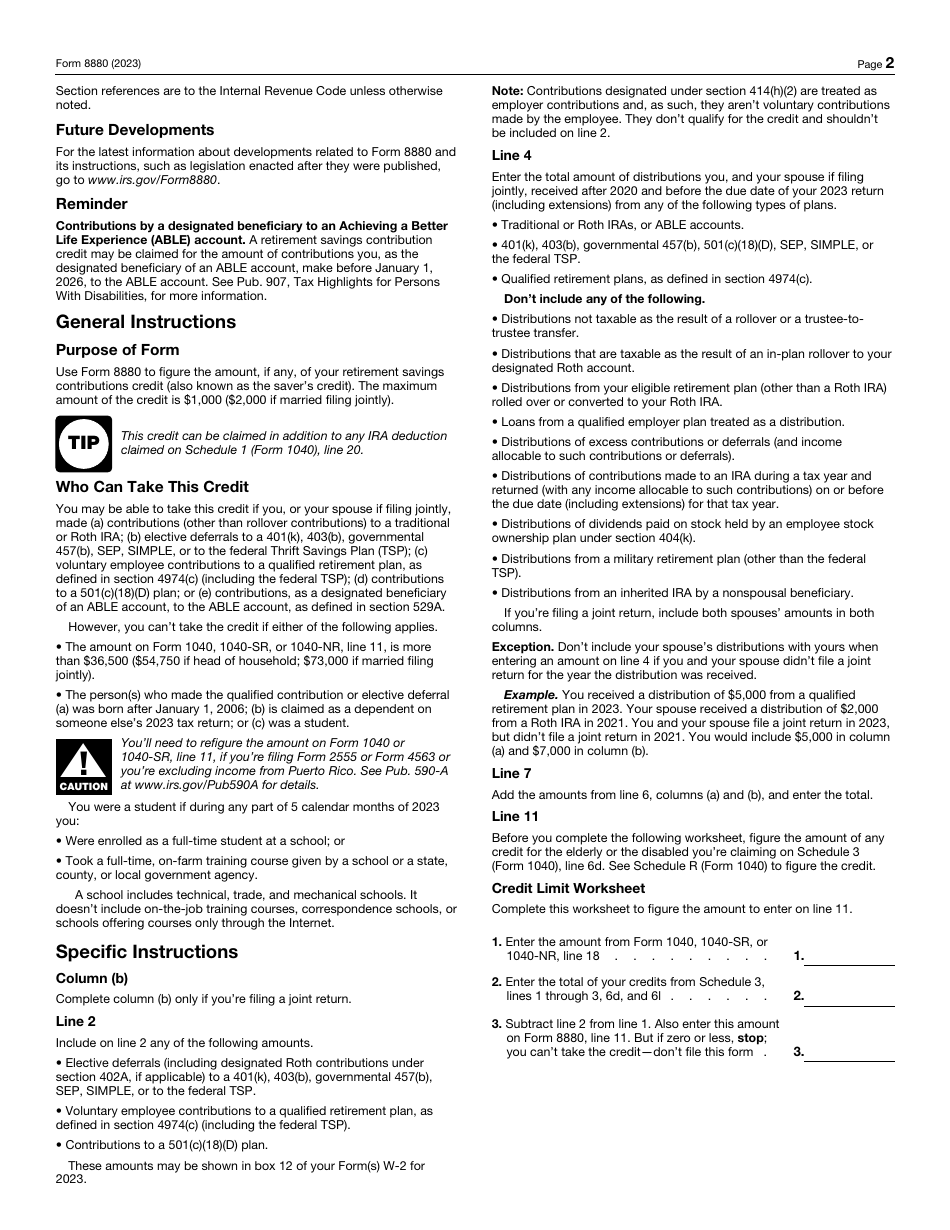

Unlike many other IRS forms, this form does not require a lot of identification information. It is connected with the fact that it is supposed to be attached to IRS Form 1040, IRS Form 1040-SR, or IRS Form 1040-NR, where the identification information is already entered. The application itself is presented on one page and it is accompanied by one page of instructions.

What Is Form 8880 Used For?

The purpose of the Tax Form 8880 is to figure out whether the taxpayer qualifies for a saver's credit in order to offset the retirement costs of the person. Use this statement to prove to the IRS you are entitled to receive a tax credit in question - $1,000 for individual taxpayers and $2,000 for married couples that prefer to file joint tax returns. Those thresholds are adjusted annually so be prepared to deal with different numbers if you are planning to file an application for a credit later in the future.

The amount of credit the government will grant to you will depend on your contributions to accounts and plans set up to ensure your retirement is financially sustainable. It is important to remember the calculations the IRS will accept upon examining your application do not include rollovers from existing accounts - all the contributions have to be new funds. Overall, taxpayers should not ignore the advantages offered by this form - while you are increasing your savings, you also lower the amount of tax you end up paying every year.

How Do You Qualify for Form 8880?

Form 8880 eligibility is based on the contributions the taxpayer or their spouse if they choose to submit their tax return jointly made to various retirement savings accounts. Those accounts include individual retirement accounts, plans sponsored by employers, and savings accounts created for people with disabilities and their family members.

There are certain factors that prevent the taxpayer from being eligible for the tax credit Federal Form 8880 was designed for - you may not file the paperwork if you were born in 2006 or later, your name features on another person's tax return as their dependent, or you were enrolled in an educational institution during the tax period covered in the document (the latter includes full-time training courses).

There is also an income threshold that allows the government to be sure only individuals with low and moderate income benefit from the tax advantages the form offers - your adjusted gross income cannot exceed $36,500; people that earned more money during the year cannot claim they are eligible for the credit. The thresholds are different for unmarried filers that financially support their household ($54,750) and spouses that file tax returns jointly ($73,000) - the numbers are constantly revised due to inflation.

How to Fill Out Form 8880?

Follow these Form 8880 instructions to certify you are eligible to receive a tax credit for retirement savings:

-

Identify yourself - write down your name and taxpayer identification number. Note that the name you include on this application has to be the same one you indicate on your income statement whether you are filing IRS Form 1040, U.S. Individual Income Tax Return, IRS Form 1040-NR, U.S. Nonresident Alien Income Tax Return, or IRS Form 1040-SR, U.S. Tax Return for Seniors. Read the guidelines put in the form for the filer's convenience to check whether you have the right to apply for the credit - in case at least one of the conditions does not reflect your circumstances, you will not be able to get this tax benefit.

-

Specify the amount of contributions to your savings accounts you have made over the course of the year. Point out how many deferrals and contributions were made from your salary to your retirement plan sponsored by your employer and combine the results to showcase the total amount of contributions.

-

Record how many distributions you and your spouse have received after 2020 and before the deadline for this form from the retirement accounts and qualified plans. There are several exceptions that you are not supposed to take into account such as loans that came from qualified employer plans and distributions from military retirement plans.

-

Use the formulas and rates featured in the application to calculate the tax credit. In order to do so, you need to consider your filing status, the details you include on your tax return, and the amount you compute with the help of the worksheet provided on the second page of the instrument.

-

Do not forget to consider the contributions made and the distributions received by your spouse - there is a separate column where you can write down the information related to them; alternatively, leave those fields blank and only focus on your own operations with retirement savings. It is recommended to fill out a draft first so that you make sure your calculations are correct and avoid printing out multiple copies of the form especially if you end up completing it with a pen.

-

Once the document is filled out, you do not have to certify it in any particular manner - your identification on top of the first page will be enough for fiscal authorities. Attach this statement to your tax return and file the paperwork prior to the usual deadline - April 15 for most taxpayers. While the IRS continues to accept and review paper returns in their processing centers, it is also permitted to submit the application online if you opt for e-filing - besides, individuals are advised to send the information electronically and save themselves time and money.

Download IRS Form 8880 Credit for Qualified Retirement Savings Contributions

1

2