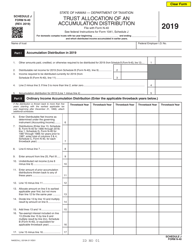

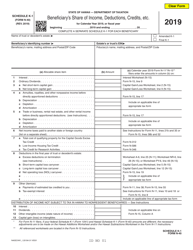

Instructions for Form N-40 Schedule A, B, C, D, E, F, G, J, K-1 - Hawaii

This document contains official instructions for Schedule A, Schedule B, Schedule C, Schedule D, Schedule E, Schedule F, Schedule G, Schedule J, and Schedule K-1 for Form N-40. . These documents are released and collected by the Hawaii Department of Taxation. An up-to-date fillable Form N-40 Schedule D is available for download through this link. The latest available Form N-40 Schedule J can be downloaded through this link. Form N-40 Schedule K-1 can be found here.

Instruction Details:

- This 17-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Hawaii Department of Taxation.

Other Revision

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17