![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1099-R, 5498

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1099-R, 5498

for the current year.

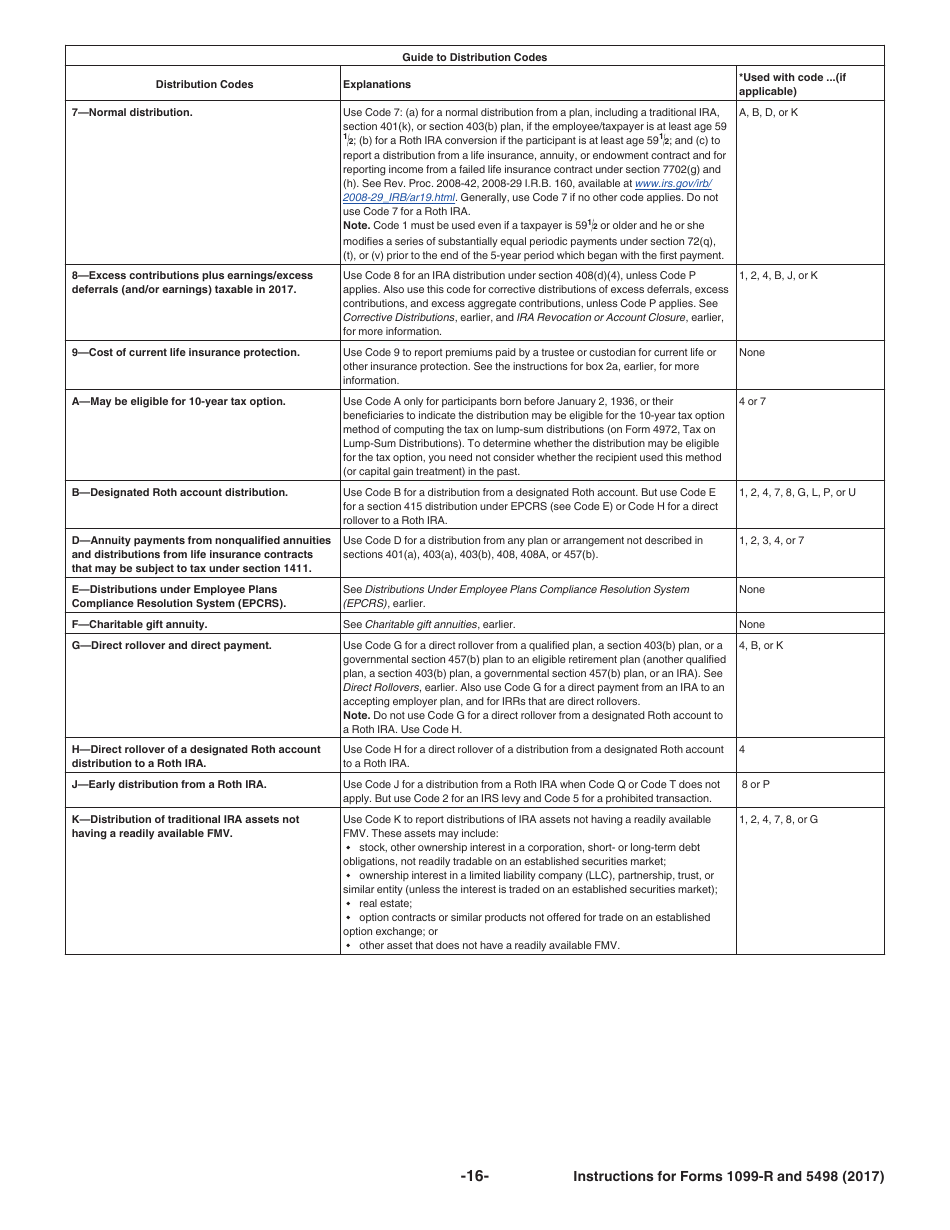

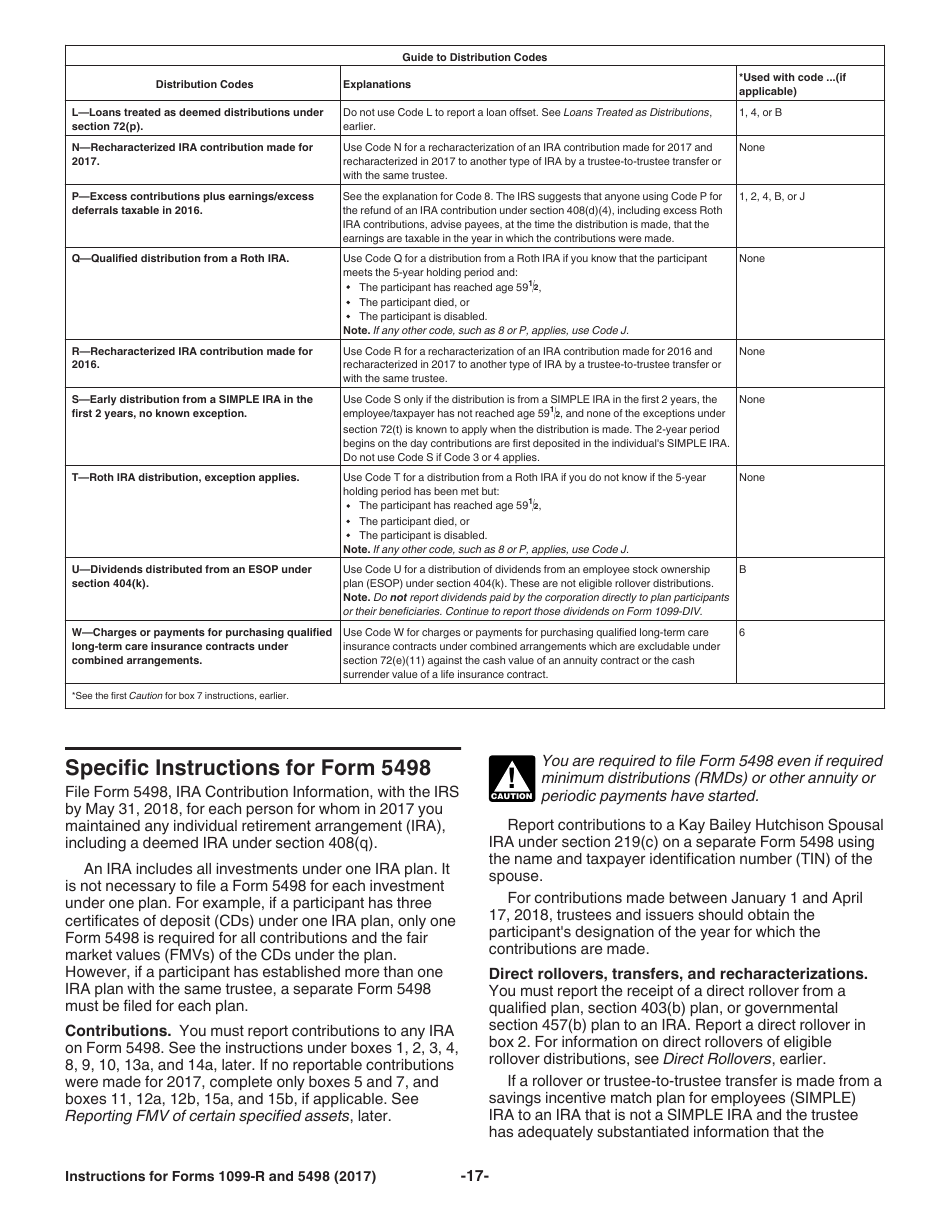

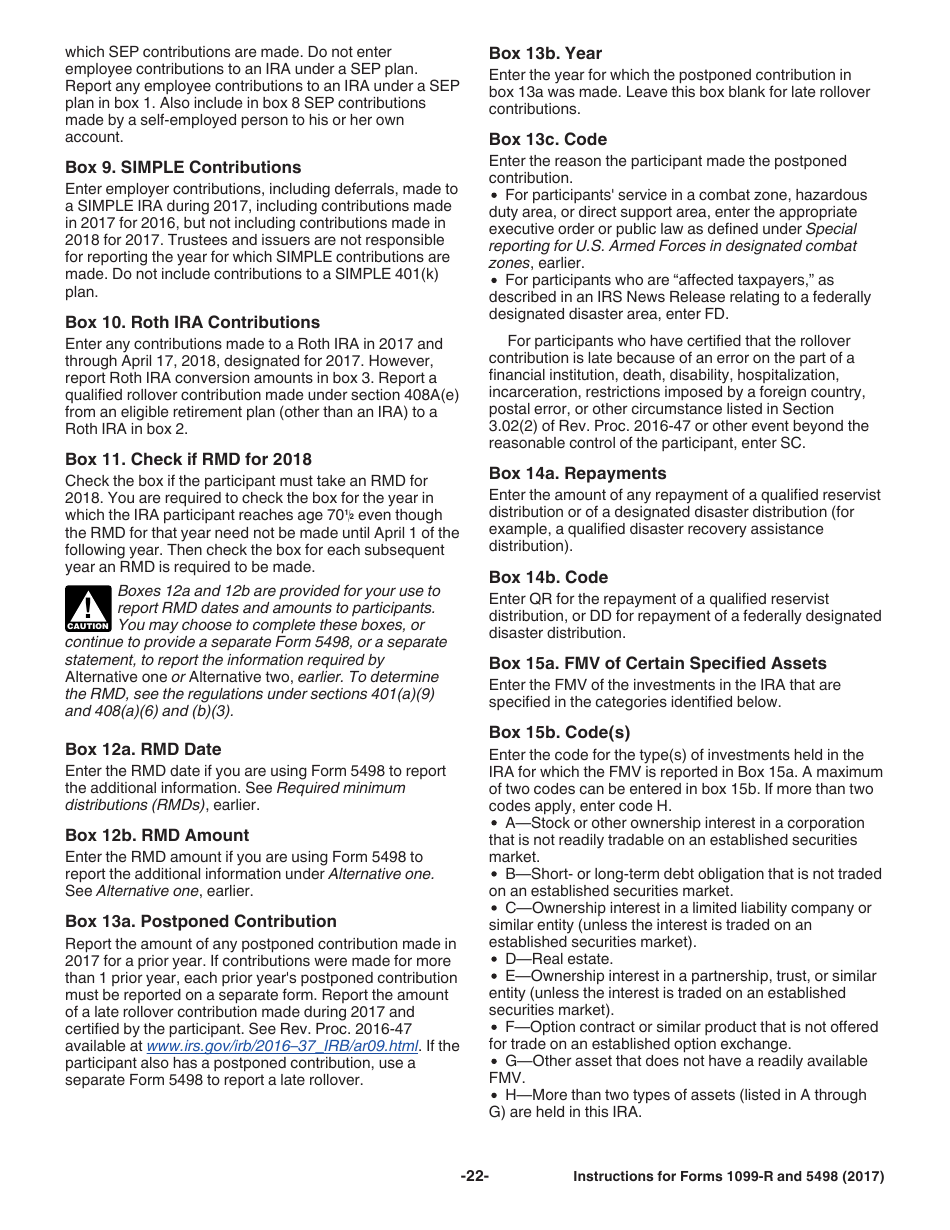

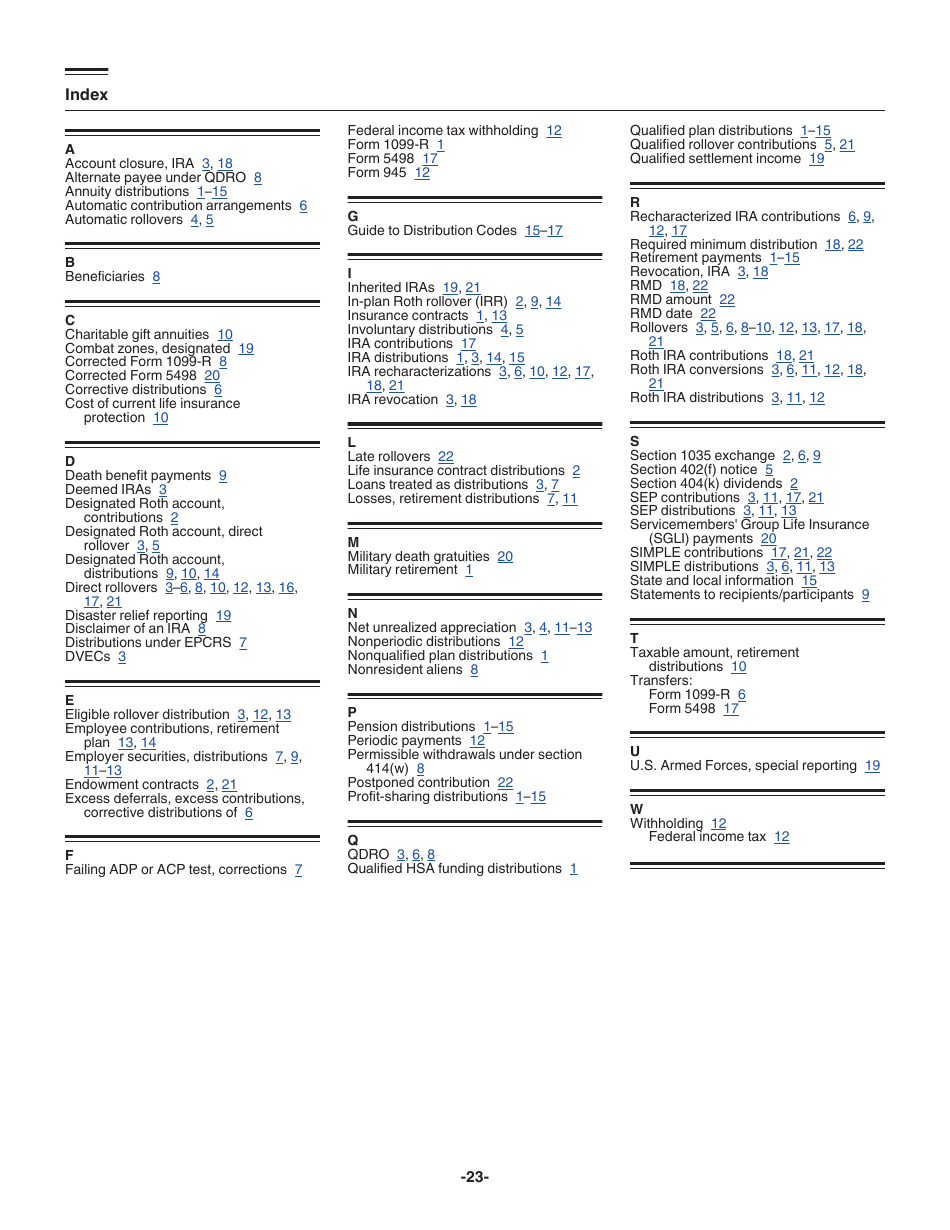

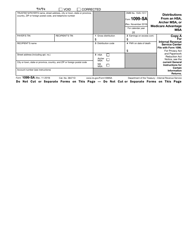

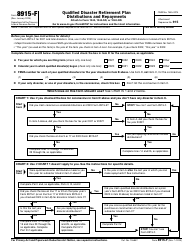

Instructions for IRS Form 1099-R, 5498 Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc. and Ira Contribution Information

This document contains official instructions for IRS Form 1099-R , and IRS Form 5498 . Both forms are released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1099-r is available for download through this link.

FAQ

Q: What is IRS Form 1099-R?

A: IRS Form 1099-R is used to report distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, insurance contracts, etc.

Q: What is IRS Form 5498?

A: IRS Form 5498 is used to report contributions made to IRAs.

Q: What information is reported on IRS Form 1099-R?

A: IRS Form 1099-R reports the amount of distributions made from retirement or investment accounts, as well as any taxes withheld.

Q: What information is reported on IRS Form 5498?

A: IRS Form 5498 reports the amount of contributions made to IRAs.

Q: When is IRS Form 1099-R issued?

A: IRS Form 1099-R is typically issued by the end of January each year for the previous tax year.

Q: When is IRS Form 5498 issued?

A: IRS Form 5498 is typically issued by May 31st each year for the previous tax year.

Q: Do I need to include IRS Form 1099-R with my tax return?

A: Yes, you generally need to include IRS Form 1099-R with your tax return if you received distributions that are subject to income tax.

Q: Do I need to include IRS Form 5498 with my tax return?

A: No, you do not typically need to include IRS Form 5498 with your tax return. It is for informational purposes only.

Instruction Details:

- This 23-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 1099-R, 5498 Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, Etc. and Ira Contribution Information

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23