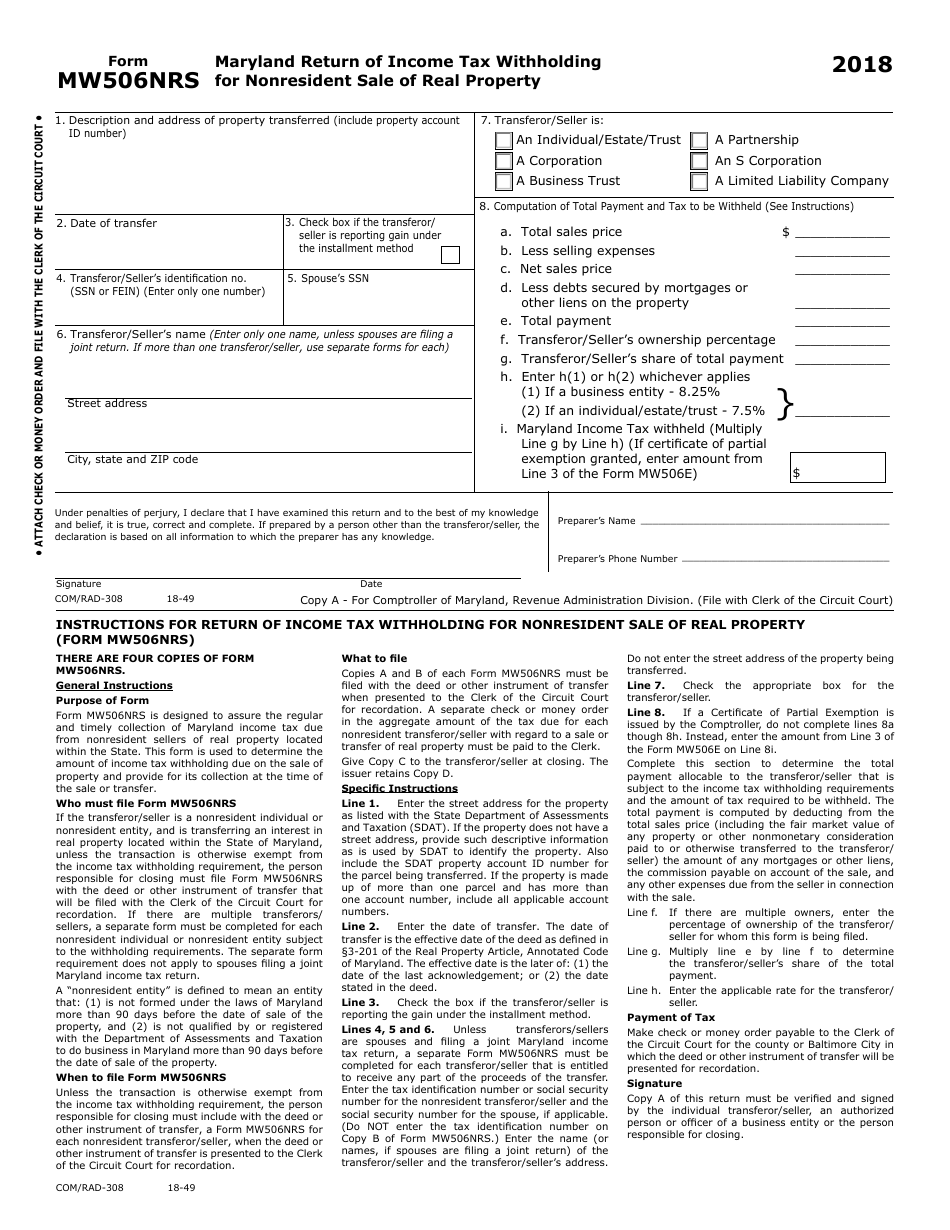

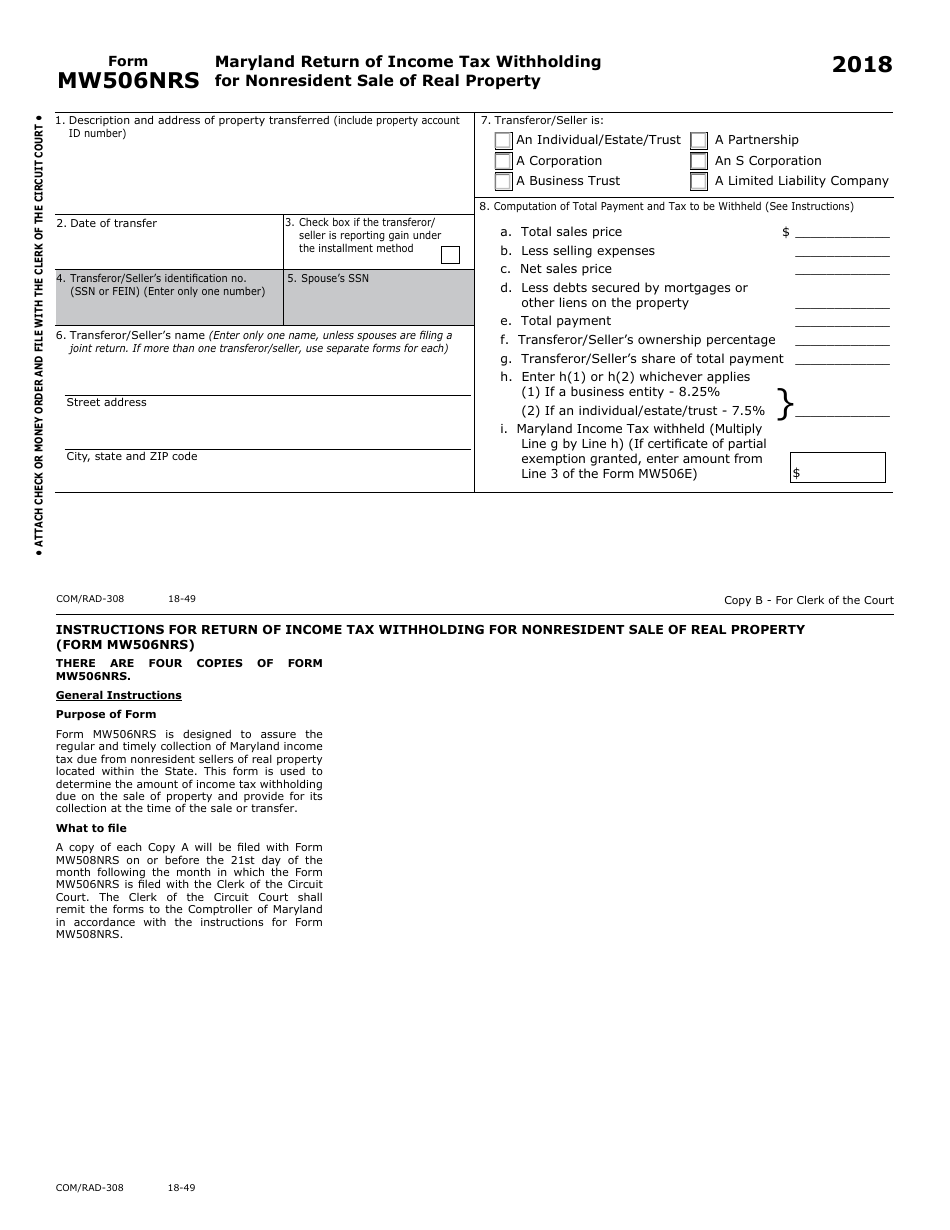

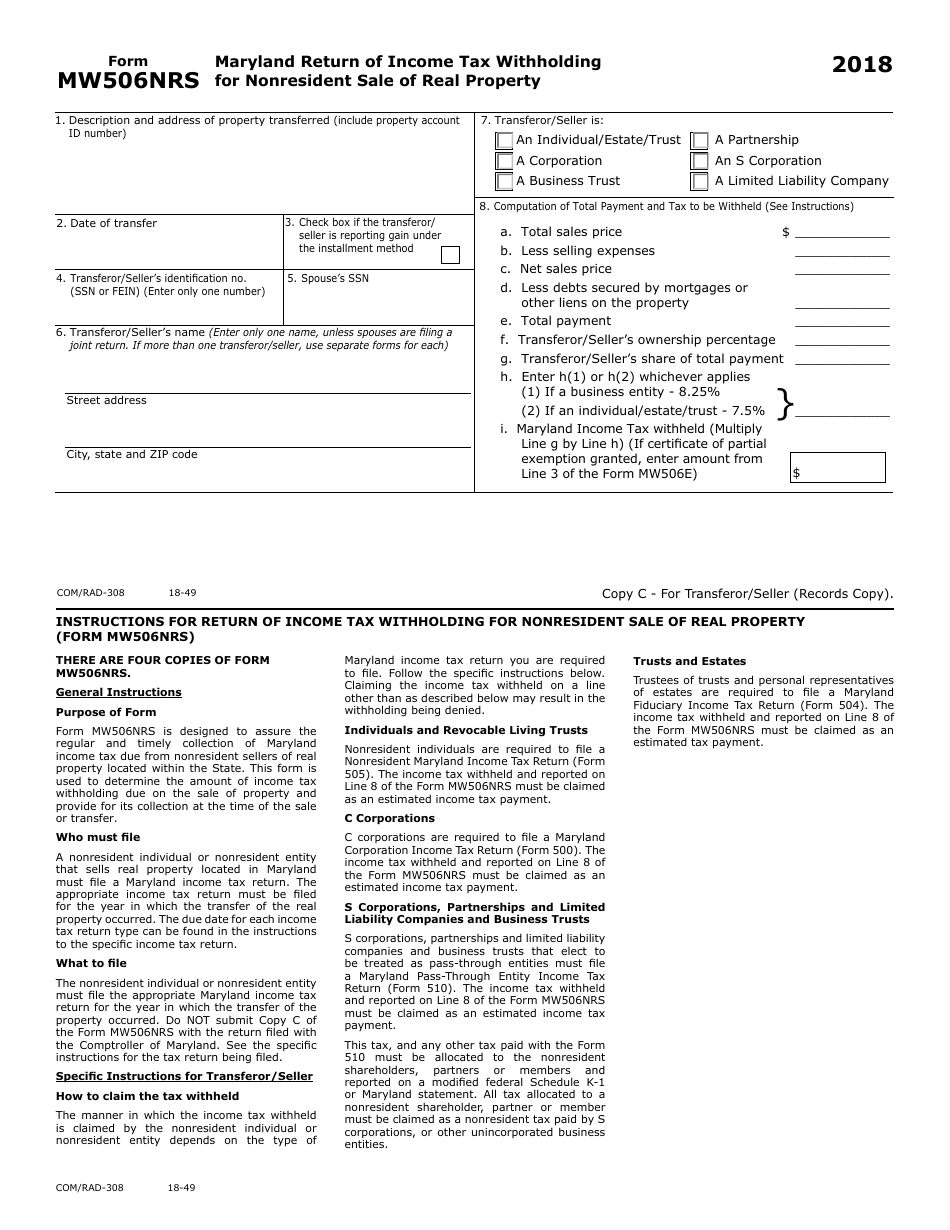

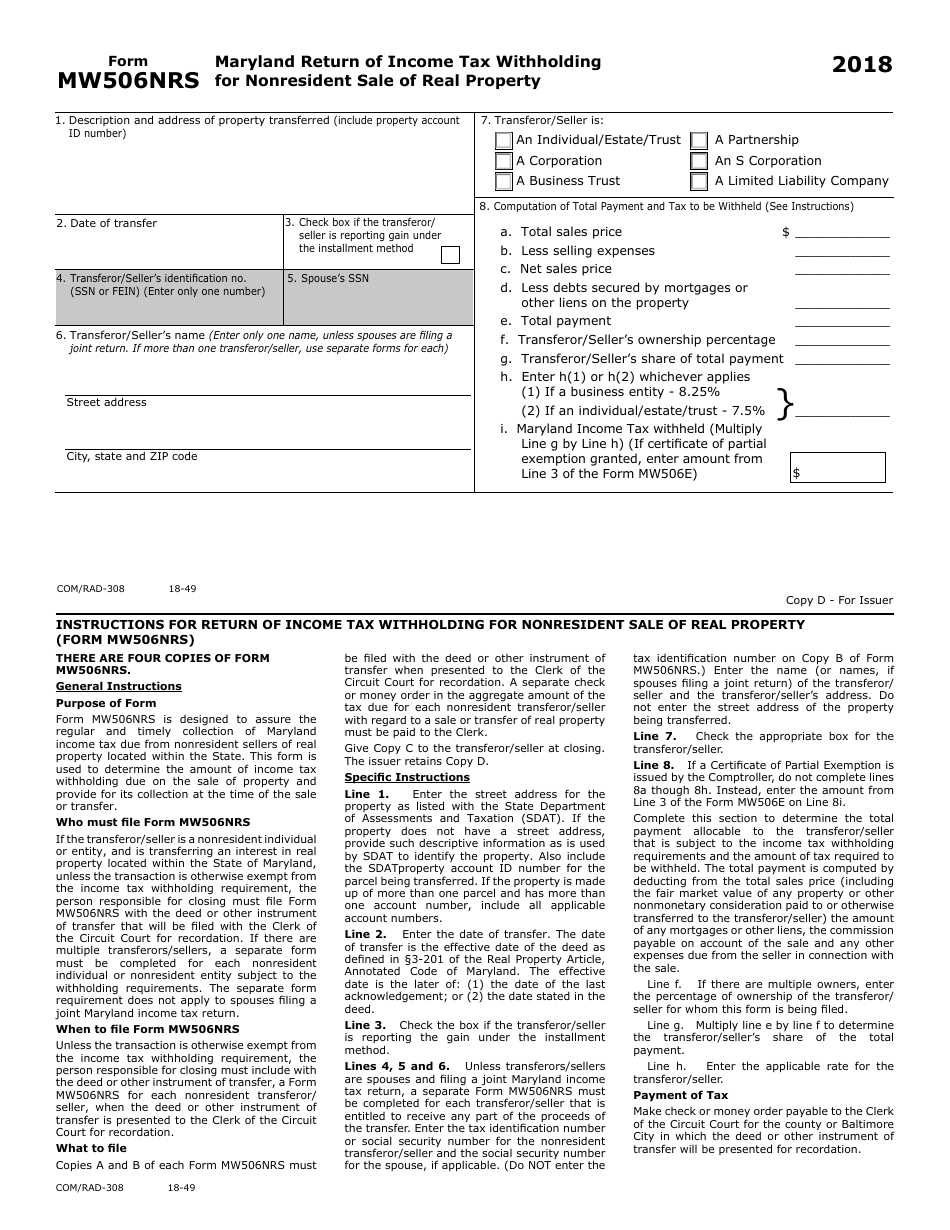

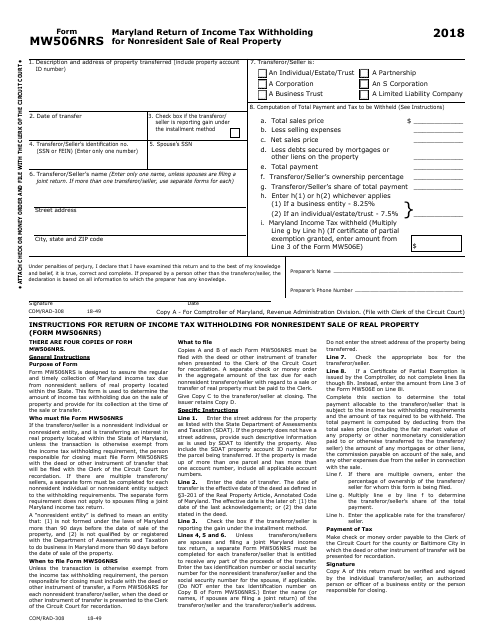

Form MW506NRS Maryland Return of Income Tax Withholding for Nonresident Sale of Real Property - Maryland

What Is Form MW506NRS?

This is a legal form that was released by the Comptroller of Maryland - a government authority operating within Maryland. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the MW506NRS form?

A: The MW506NRS form is the Maryland Return of Income Tax Withholding for Nonresident Sale of Real Property.

Q: Who needs to file the MW506NRS form?

A: Nonresident individuals or entities who sold real property in Maryland need to file the MW506NRS form.

Q: What is the purpose of the MW506NRS form?

A: The purpose of the MW506NRS form is to report and remit income tax withholding from the sale of real property in Maryland by nonresident individuals or entities.

Q: When is the deadline to file the MW506NRS form?

A: The MW506NRS form must be filed within 30 days after the date of transfer of the real property.

Q: Is there a penalty for late filing of the MW506NRS form?

A: Yes, there is a penalty for late filing of the MW506NRS form. The penalty is 5% of the tax due per month, up to a maximum of 25%.

Q: What documentation should be attached to the MW506NRS form?

A: You should attach a copy of the settlement statement or closing disclosure to the MW506NRS form.

Q: Do I need to pay estimated taxes in addition to filing the MW506NRS form?

A: If you are a nonresident individual or entity who sold real property in Maryland, you may be required to pay estimated taxes in addition to filing the MW506NRS form. It is recommended to consult a tax professional for accurate guidance.

Q: Are there any exemptions or deductions available for nonresident individuals or entities filing the MW506NRS form?

A: There are no specific exemptions or deductions available for nonresident individuals or entities filing the MW506NRS form. However, you may be eligible for certain federal tax deductions. Consult a tax professional for more information.

Form Details:

- The latest edition provided by the Comptroller of Maryland;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form MW506NRS by clicking the link below or browse more documents and templates provided by the Comptroller of Maryland.

Download Form MW506NRS Maryland Return of Income Tax Withholding for Nonresident Sale of Real Property - Maryland

1

2

3

4