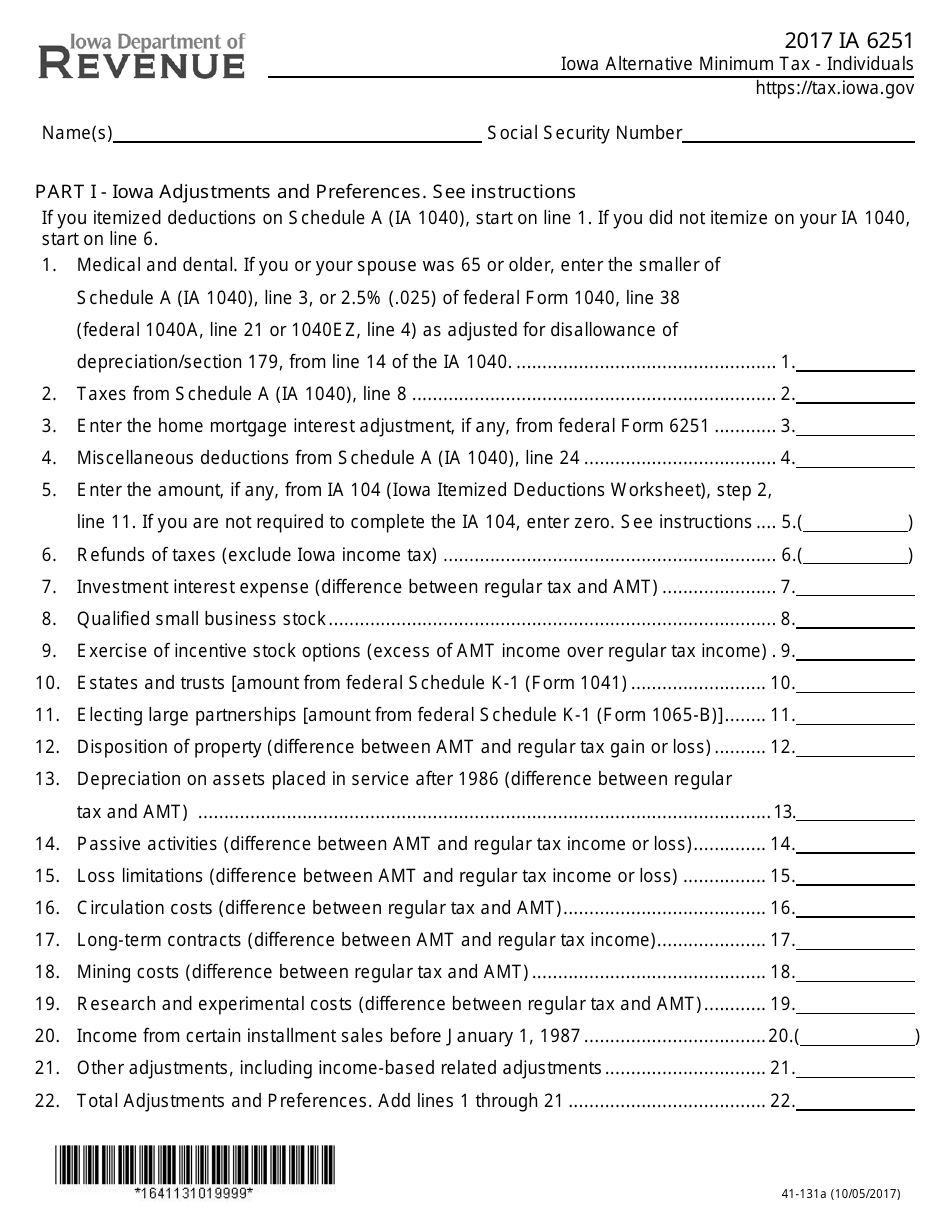

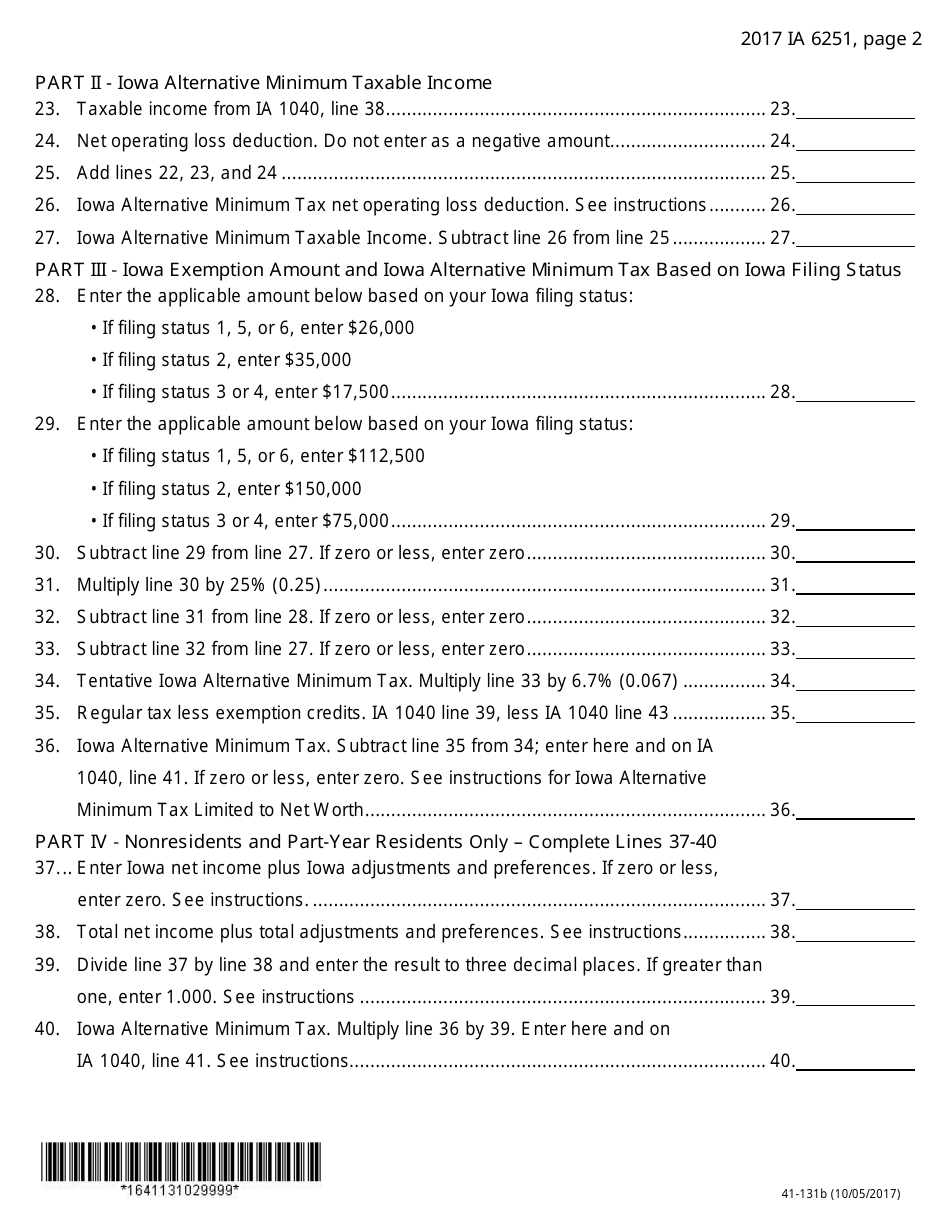

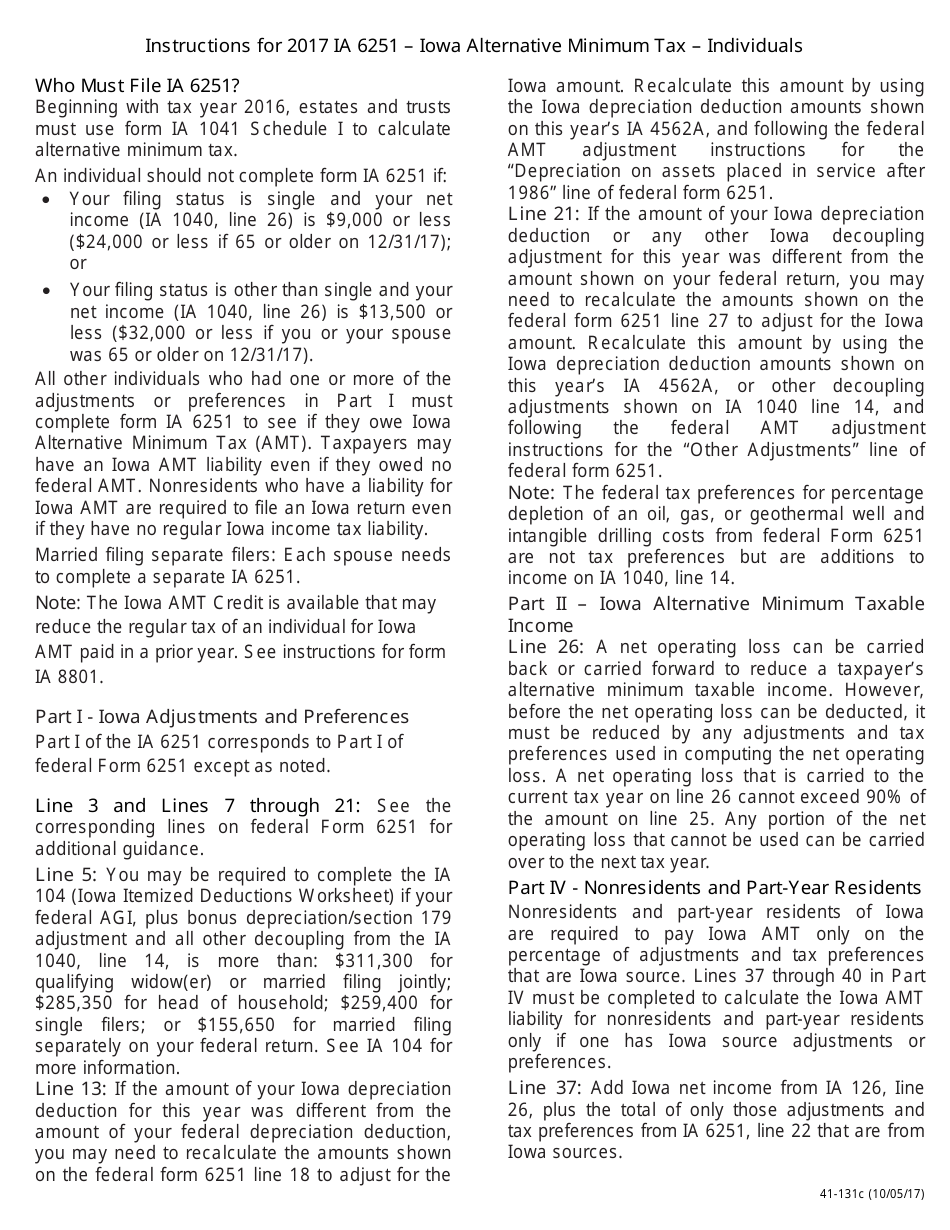

Form IA6251 Iowa Alternative Minimum Tax - Individuals - Iowa

What Is Form IA6251?

This is a legal form that was released by the Iowa Department of Revenue - a government authority operating within Iowa. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form IA6251?

A: Form IA6251 is the Iowa Alternative Minimum Tax form for individuals.

Q: Who needs to file Form IA6251?

A: Residents of Iowa who are subject to the alternative minimum tax (AMT) need to file Form IA6251.

Q: What is the alternative minimum tax (AMT)?

A: The alternative minimum tax (AMT) is a separate income tax calculation that ensures individuals with high deductions and credits still pay a minimum amount of tax.

Q: What does Form IA6251 calculate?

A: Form IA6251 calculates the alternative minimum tax (AMT) liability for Iowa residents.

Q: Are there any exemptions or deductions available for the Iowa alternative minimum tax?

A: No, there are no specific exemptions or deductions available for the Iowa alternative minimum tax.

Q: When is the deadline to file Form IA6251?

A: The deadline to file Form IA6251 is the same as the deadline for filing your Iowa income tax return, which is typically April 30.

Q: Can I file Form IA6251 electronically?

A: Yes, Iowa allows for electronic filing of Form IA6251.

Q: Do I need to include Form IA6251 with my federal tax return?

A: No, Form IA6251 is specific to Iowa and should not be included with your federal tax return.

Q: Do I need to include a copy of my federal tax return with Form IA6251?

A: Yes, you need to include a copy of your federal tax return with Form IA6251.

Form Details:

- Released on May 10, 2017;

- The latest edition provided by the Iowa Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form IA6251 by clicking the link below or browse more documents and templates provided by the Iowa Department of Revenue.

Download Form IA6251 Iowa Alternative Minimum Tax - Individuals - Iowa

1

2

3