![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form REV85 0050

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form REV85 0050

for the current year.

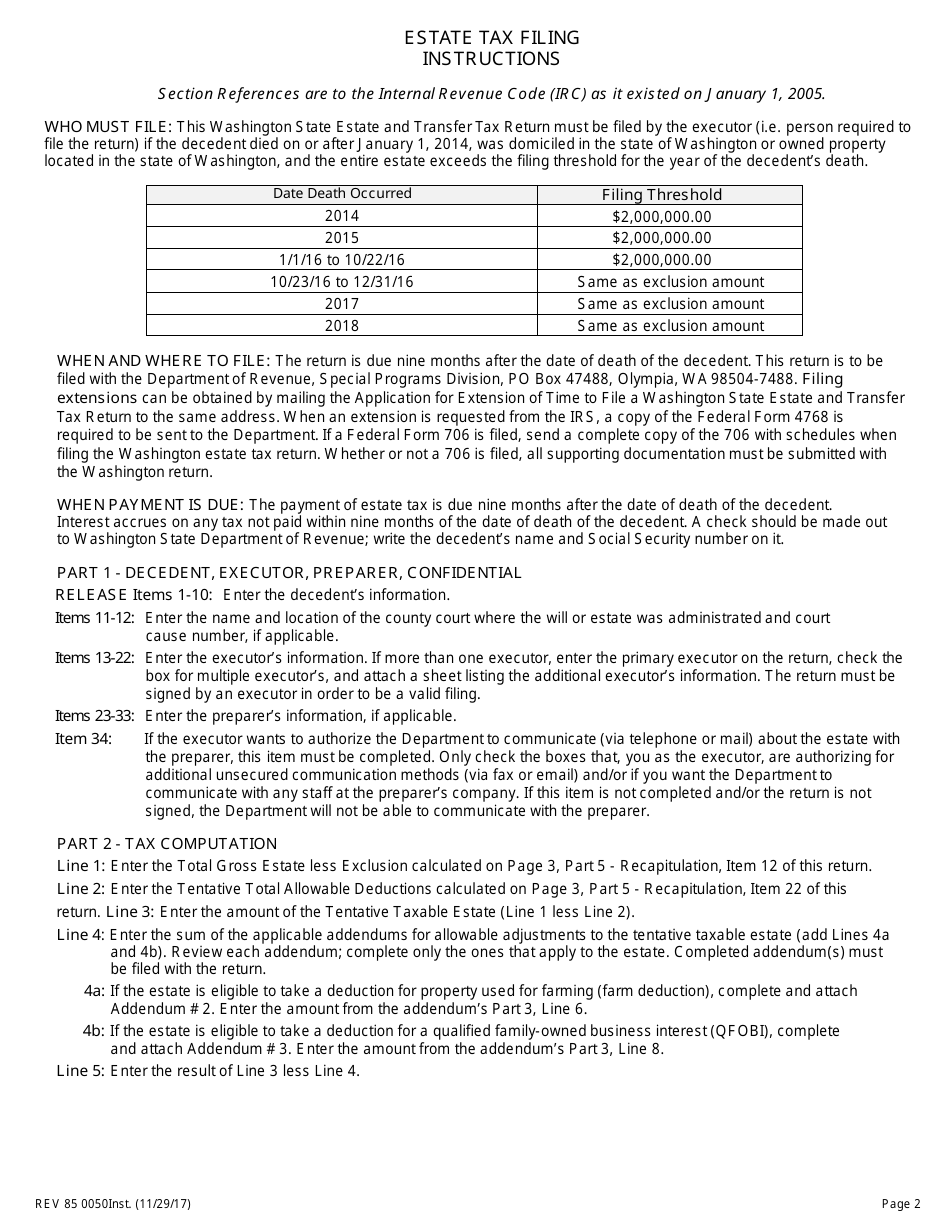

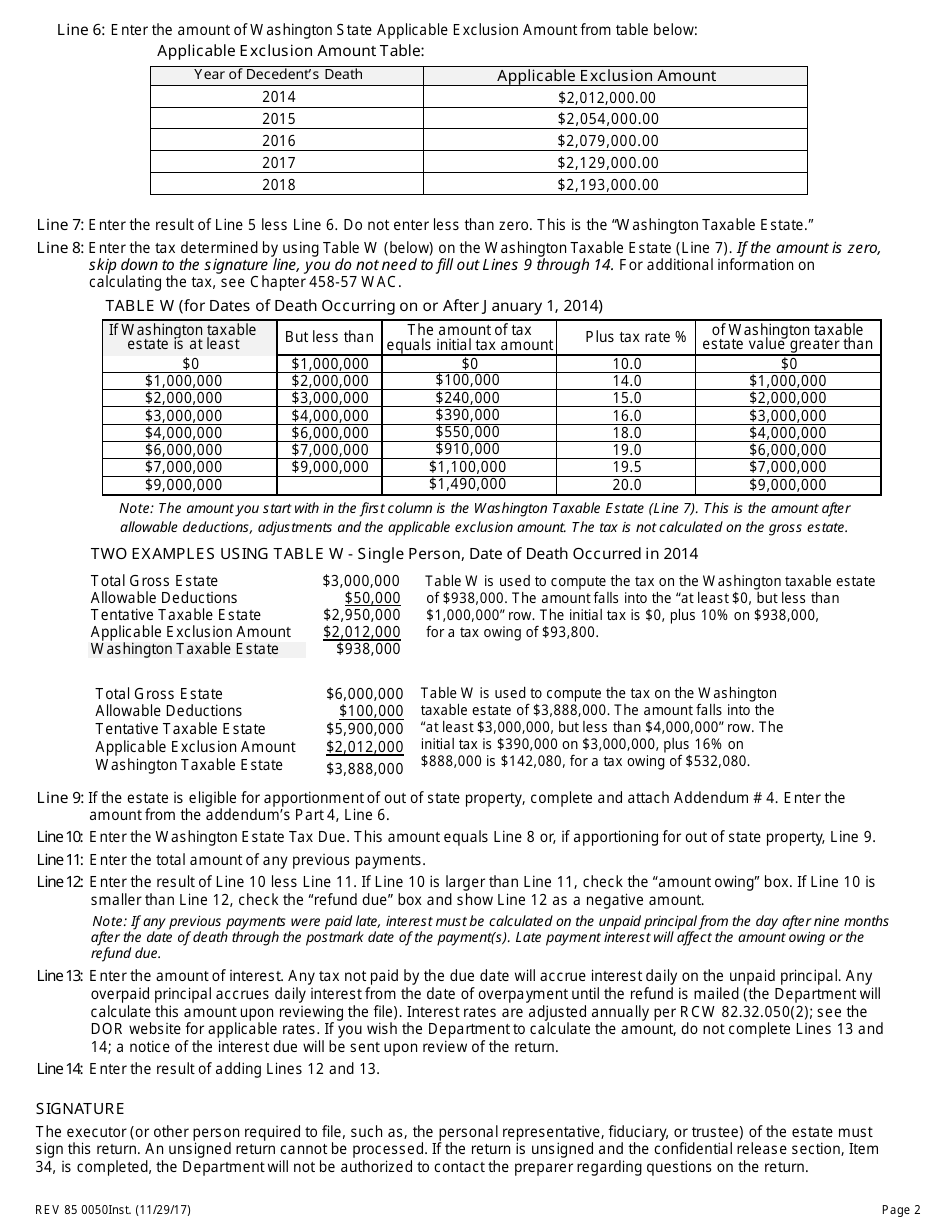

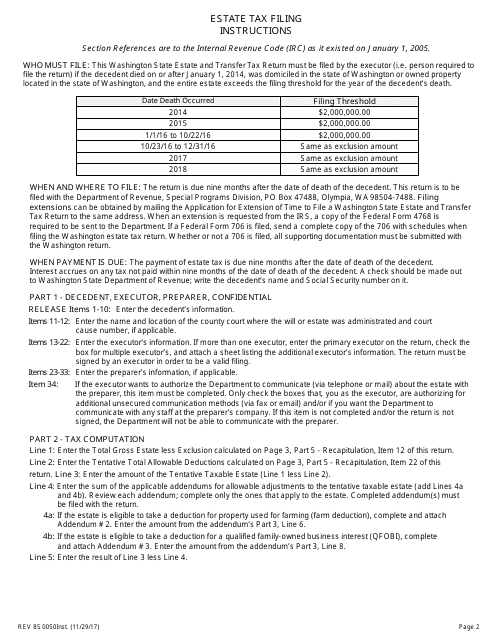

Instructions for Form REV85 0050 Washington State Estate and Transfer Tax Return - Washington

This document contains official instructions for Form REV85 0050 , Washington State Estate and Transfer Tax Return - a form released and collected by the Washington State Department of Revenue. An up-to-date fillable Form REV85 0050 is available for download through this link.

FAQ

Q: What is Form REV85 0050?

A: Form REV85 0050 is the Washington State Estate and Transfer Tax Return.

Q: Who needs to file Form REV85 0050?

A: The executor or personal representative of a deceased person's estate needs to file Form REV85 0050.

Q: What is the purpose of Form REV85 0050?

A: The purpose of Form REV85 0050 is to calculate and report the estate and transfer tax owed to the state of Washington.

Q: When should Form REV85 0050 be filed?

A: Form REV85 0050 should be filed within 9 months from the date of the deceased person's death or within 9 months from the date the representative was appointed, whichever is later.

Q: Are there any filing fees for Form REV85 0050?

A: No, there are no filing fees for Form REV85 0050.

Q: What documents and information do I need to complete Form REV85 0050?

A: You will need information about the deceased person's assets, liabilities, and beneficiaries, as well as documentation such as the death certificate and any relevant estate planning documents.

Q: What happens if I don't file Form REV85 0050?

A: Failure to file Form REV85 0050 may result in penalties and interest being assessed on any unpaid taxes owed.

Instruction Details:

- This 28-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Washington State Department of Revenue.

Download Instructions for Form REV85 0050 Washington State Estate and Transfer Tax Return - Washington

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28