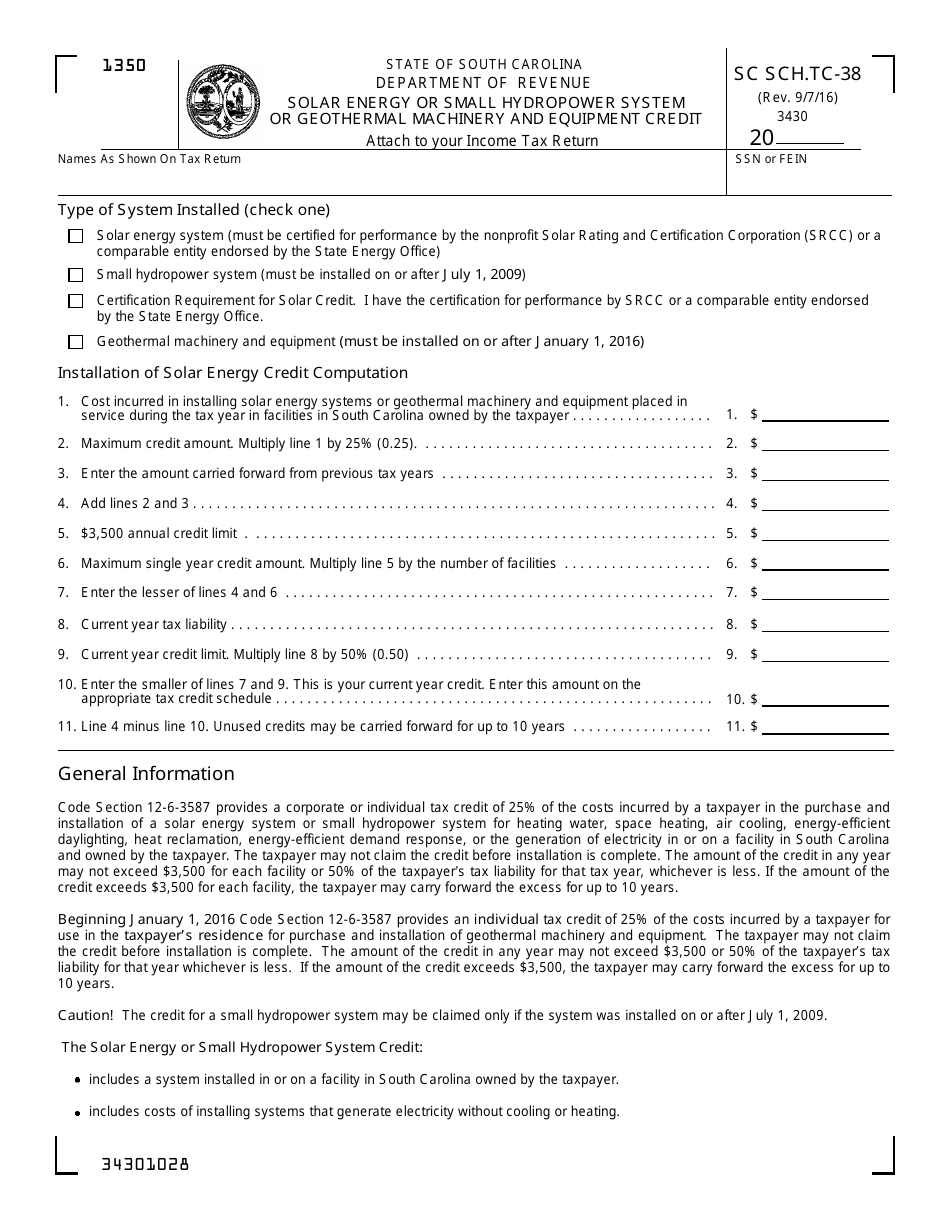

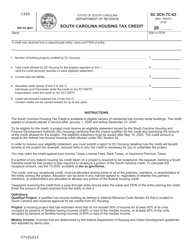

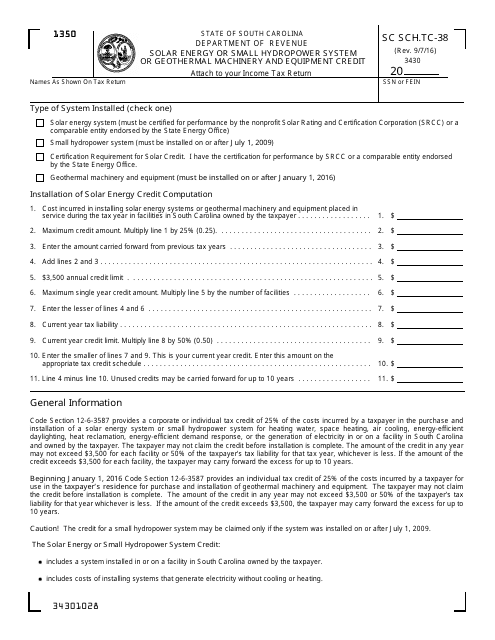

Form SC SCH.TC-38 Schedule TC-38 Solar Energy or Small Hydropower System or Geothermal Machinery and Equipment Credit - South Carolina

What Is Form SC SCH.TC-38 Schedule TC-38?

This is a legal form that was released by the South Carolina Department of Revenue - a government authority operating within South Carolina. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is SC SCH.TC-38?

A: SC SCH.TC-38 is a schedule form for claiming the Solar Energy or Small Hydropower System or Geothermal Machinery and Equipment Credit in South Carolina.

Q: What is the purpose of SC SCH.TC-38?

A: The purpose of SC SCH.TC-38 is to claim a credit for solar energy, small hydropower systems, or geothermal machinery and equipment in South Carolina.

Q: Who can use SC SCH.TC-38?

A: Anyone who has installed solar energy systems, small hydropower systems, or geothermal machinery and equipment in South Carolina can use SC SCH.TC-38.

Q: What types of systems are eligible for the credit?

A: Solar energy systems, small hydropower systems, and geothermal machinery and equipment are eligible for the credit.

Q: How much credit can be claimed?

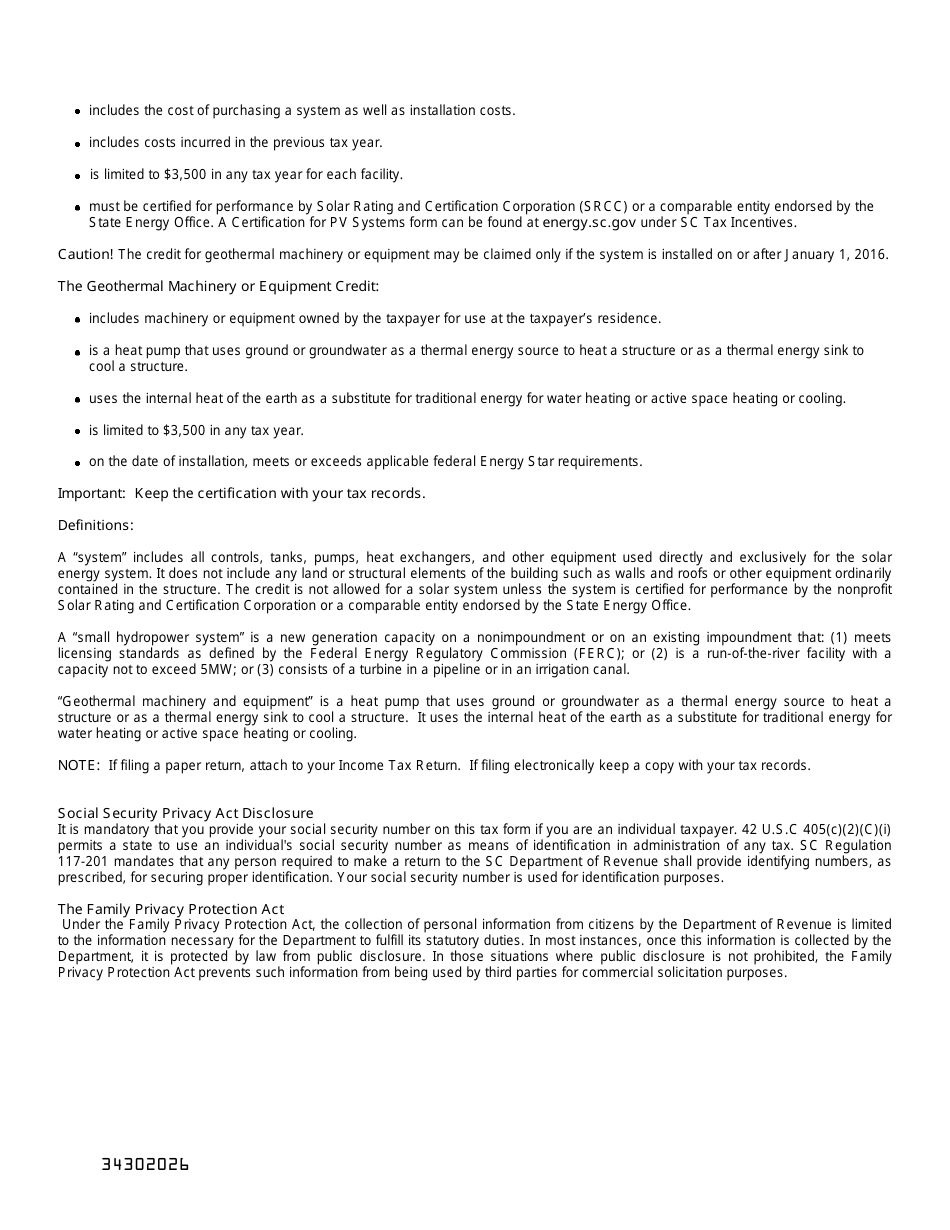

A: The credit amount varies depending on the type and capacity of the system, as well as other factors. The specific details can be found in the instructions for SC SCH.TC-38.

Form Details:

- Released on September 7, 2016;

- The latest edition provided by the South Carolina Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form SC SCH.TC-38 Schedule TC-38 by clicking the link below or browse more documents and templates provided by the South Carolina Department of Revenue.

Download Form SC SCH.TC-38 Schedule TC-38 Solar Energy or Small Hydropower System or Geothermal Machinery and Equipment Credit - South Carolina

1

2