![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1120

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1120

for the current year.

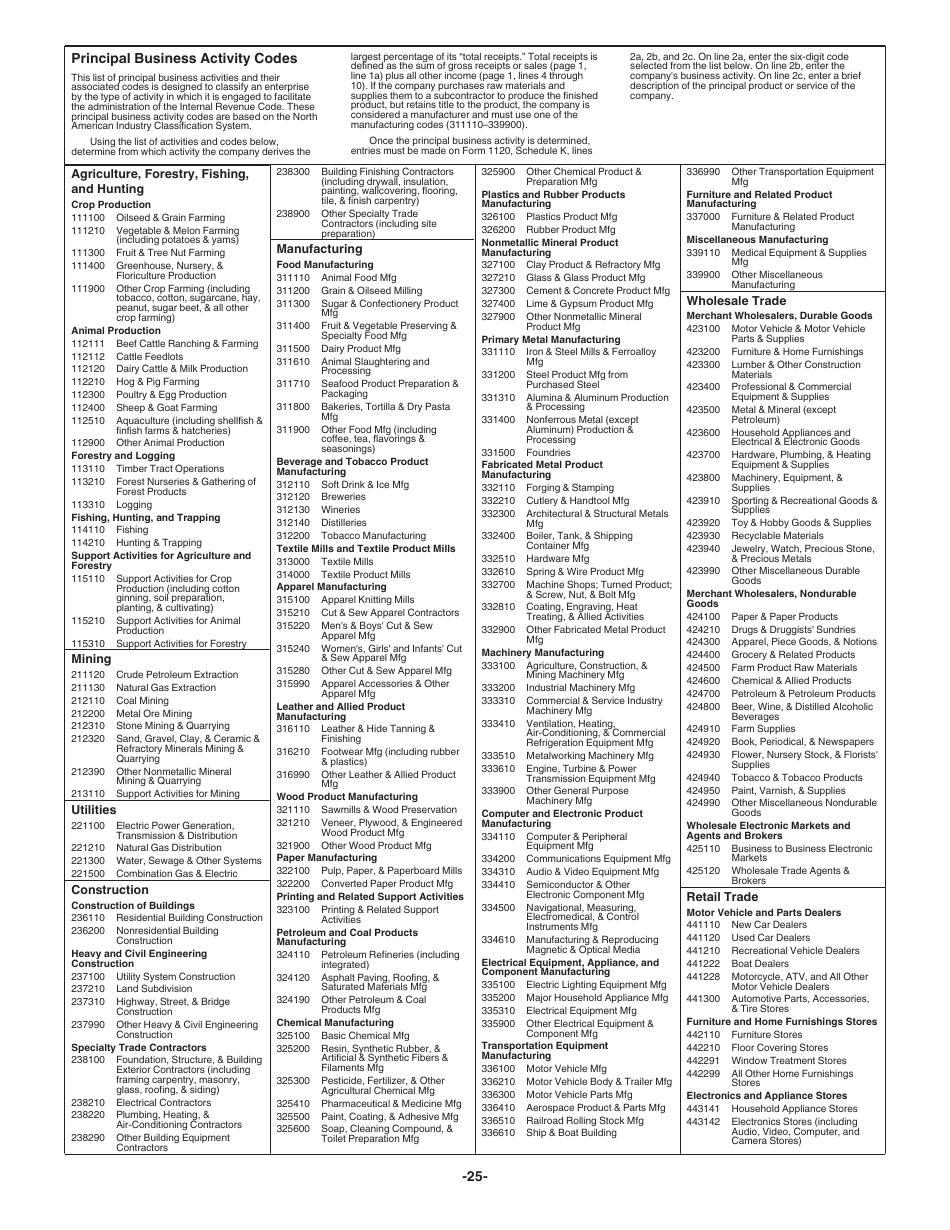

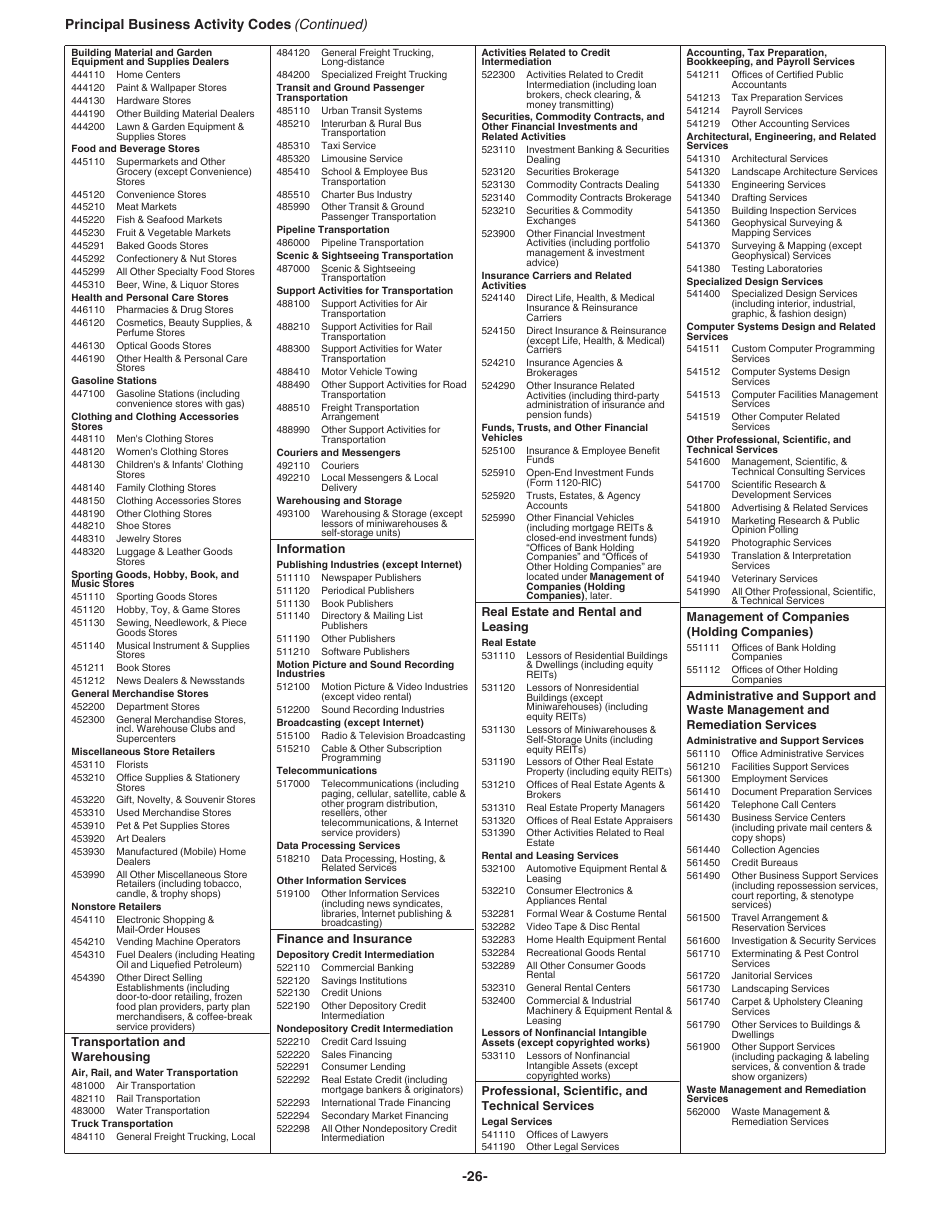

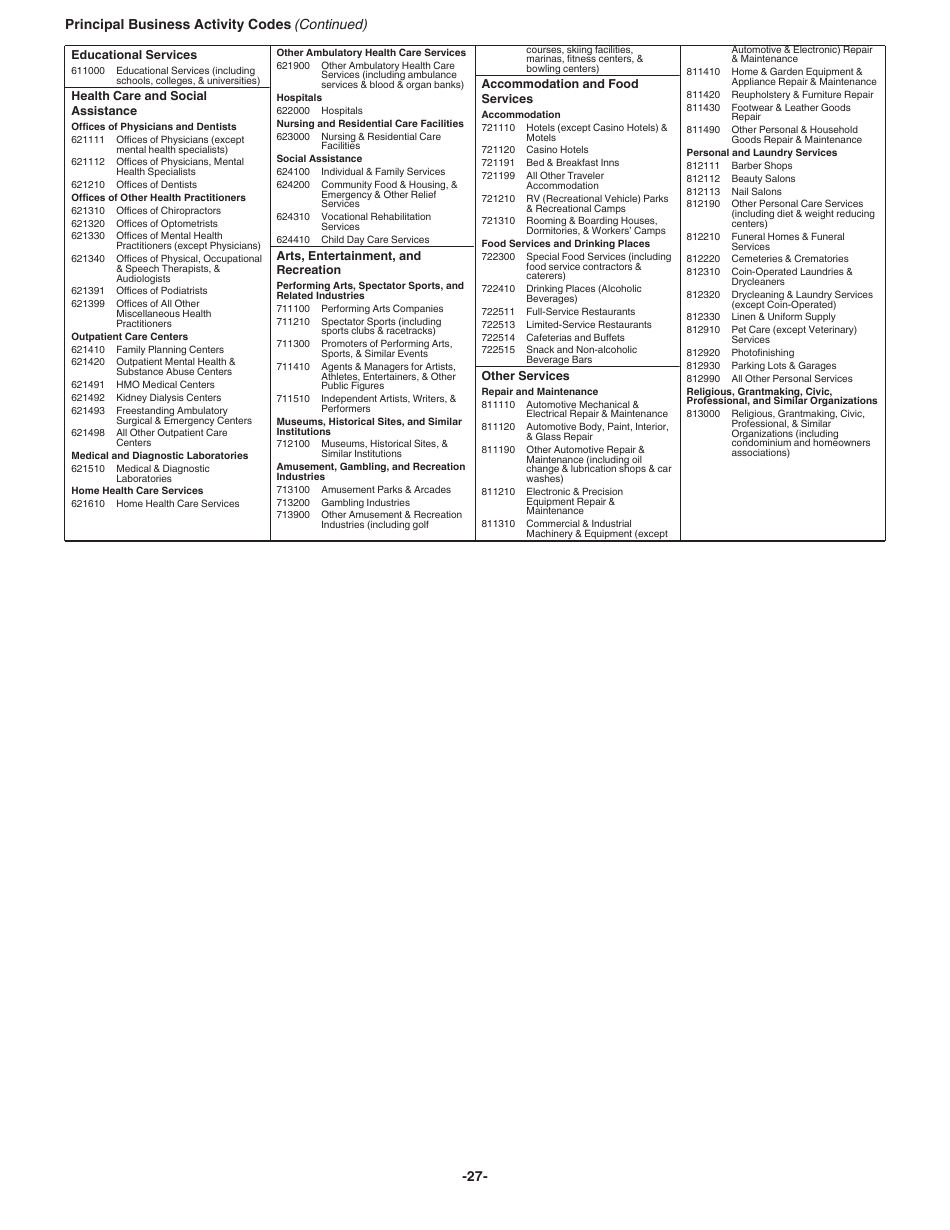

Instructions for IRS Form 1120 U.S. Corporation Income Tax Return

This document contains official instructions for IRS Form 1120 , U.S. Corporation Income Tax Return - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1120 Schedule D is available for download through this link.

FAQ

Q: What is IRS Form 1120?

A: IRS Form 1120 is the U.S. Corporation Income Tax Return.

Q: Who needs to file Form 1120?

A: All domestic corporations (including S corporations) are required to file Form 1120.

Q: When is the deadline to file Form 1120?

A: The deadline to file Form 1120 is generally the 15th day of the 4th month after the end of the corporation's tax year.

Q: What information is required to complete Form 1120?

A: Form 1120 requires information about the corporation's income, deductions, credits, and other relevant financial details.

Q: Are there any penalties for not filing Form 1120?

A: Yes, failure to file Form 1120 or filing it late can result in penalties and interest charges.

Q: Can I e-file Form 1120?

A: Yes, you can e-file Form 1120 if you meet the requirements for electronic filing.

Q: Are there any special rules or deductions for small corporations?

A: Yes, there are certain tax provisions and deductions specifically designed for small corporations.

Q: Do I need to attach any supporting documents with Form 1120?

A: You may need to attach certain schedules and statements depending on the corporation's specific situation.

Instruction Details:

- This 28-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28