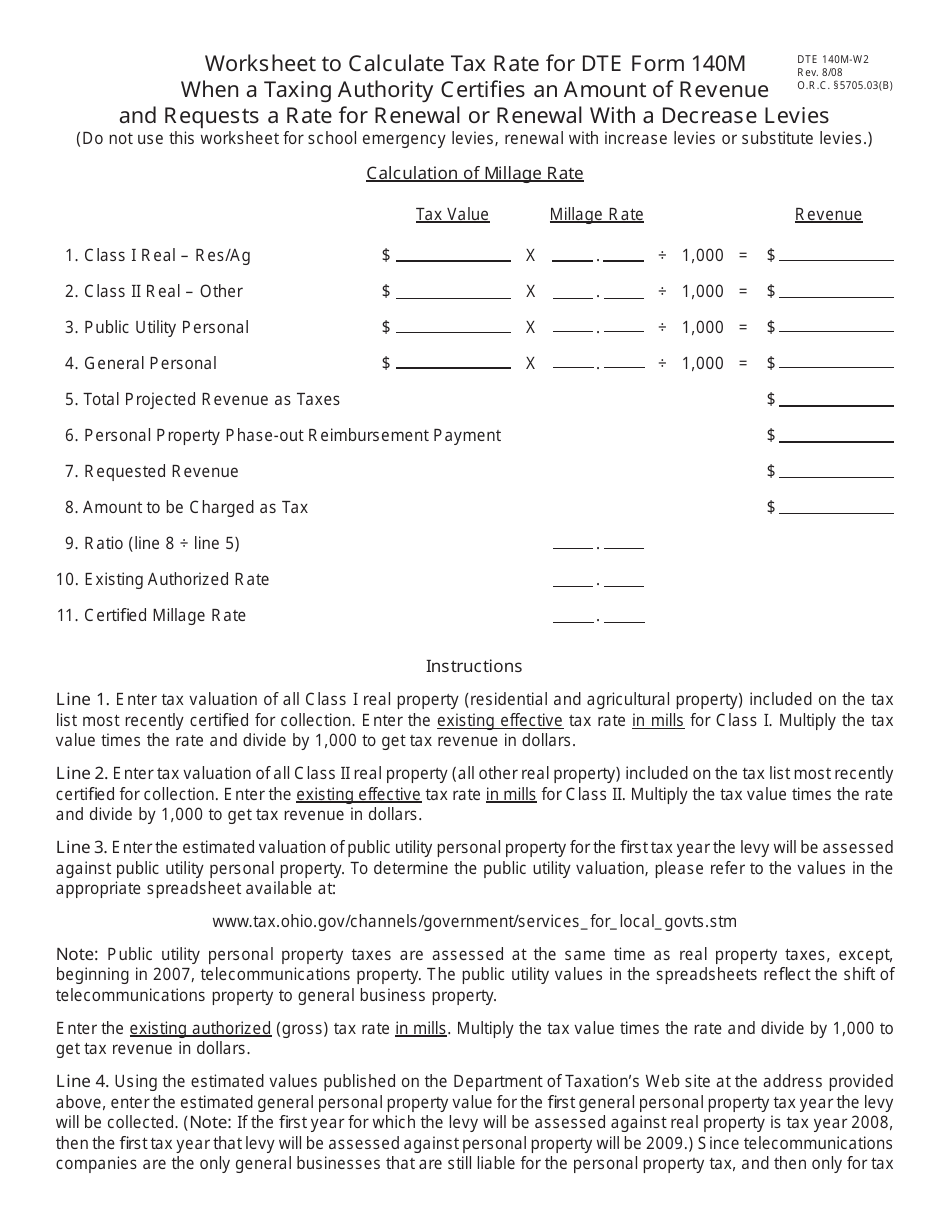

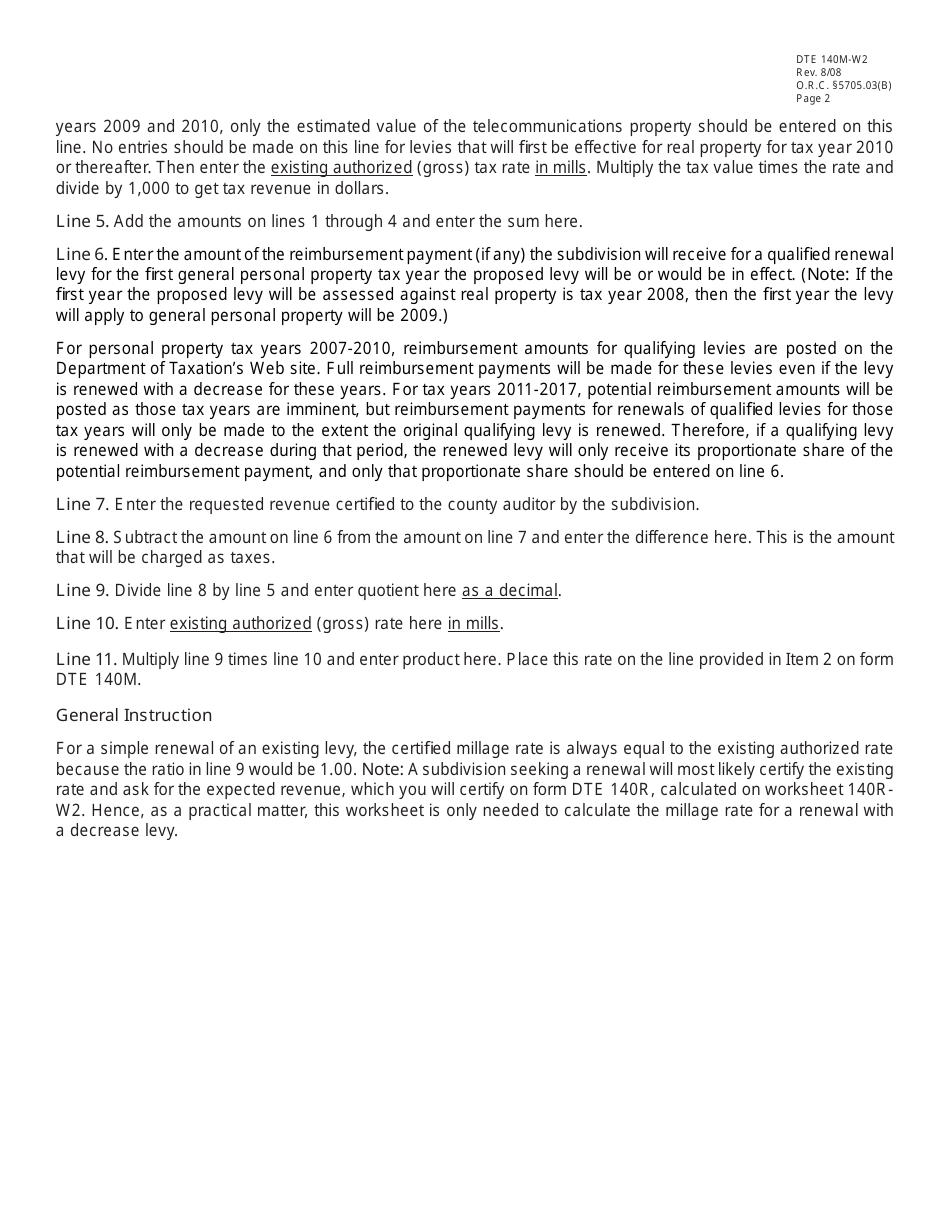

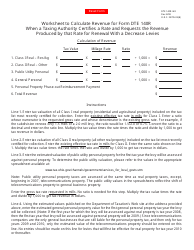

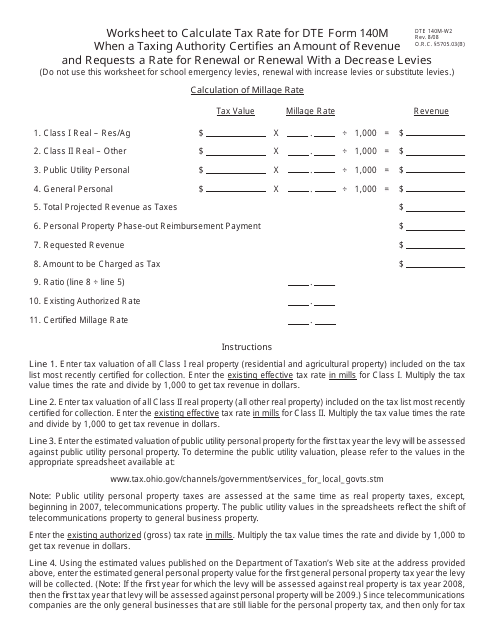

Form DTE140M-W2 Worksheet for Renewal or Renewal With a Decrease Levies - Ohio

What Is Form DTE140M-W2?

This is a legal form that was released by the Ohio Department of Taxation - a government authority operating within Ohio. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form DTE140M-W2?

A: Form DTE140M-W2 is a worksheet for property owners in Ohio who are applying for renewal or renewal with a decrease levies.

Q: Who needs to use Form DTE140M-W2?

A: Property owners in Ohio applying for renewal or renewal with a decrease levies need to use Form DTE140M-W2.

Q: What is the purpose of Form DTE140M-W2?

A: The purpose of Form DTE140M-W2 is to help property owners calculate their property tax liabilities based on various levies.

Q: When should Form DTE140M-W2 be used?

A: Form DTE140M-W2 should be used when applying for renewal or renewal with a decrease levies in Ohio.

Q: How do I fill out Form DTE140M-W2?

A: You need to provide the requested information on the form, including property details, levies information, and calculation of property tax liabilities.

Q: Are there any fees associated with filing Form DTE140M-W2?

A: There are no fees associated with filing Form DTE140M-W2.

Q: Is there a deadline for submitting Form DTE140M-W2?

A: The deadline for submitting Form DTE140M-W2 varies by county, so you should check with your local county auditor's office for the specific deadline.

Q: What should I do if I made a mistake on Form DTE140M-W2?

A: If you made a mistake on Form DTE140M-W2, you should contact your local county auditor's office for guidance on how to correct the error.

Form Details:

- Released on August 1, 2008;

- The latest edition provided by the Ohio Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form DTE140M-W2 by clicking the link below or browse more documents and templates provided by the Ohio Department of Taxation.

Download Form DTE140M-W2 Worksheet for Renewal or Renewal With a Decrease Levies - Ohio

1

2