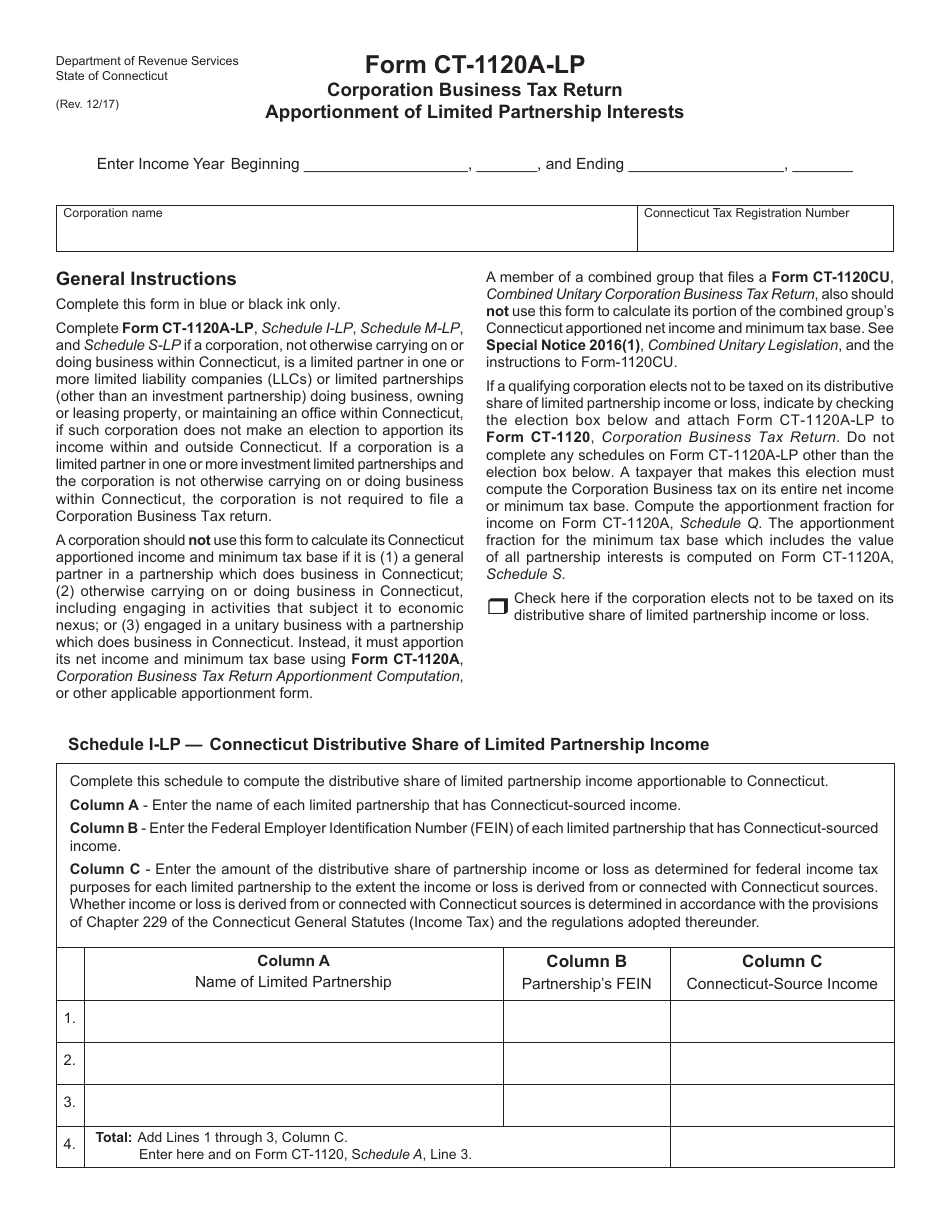

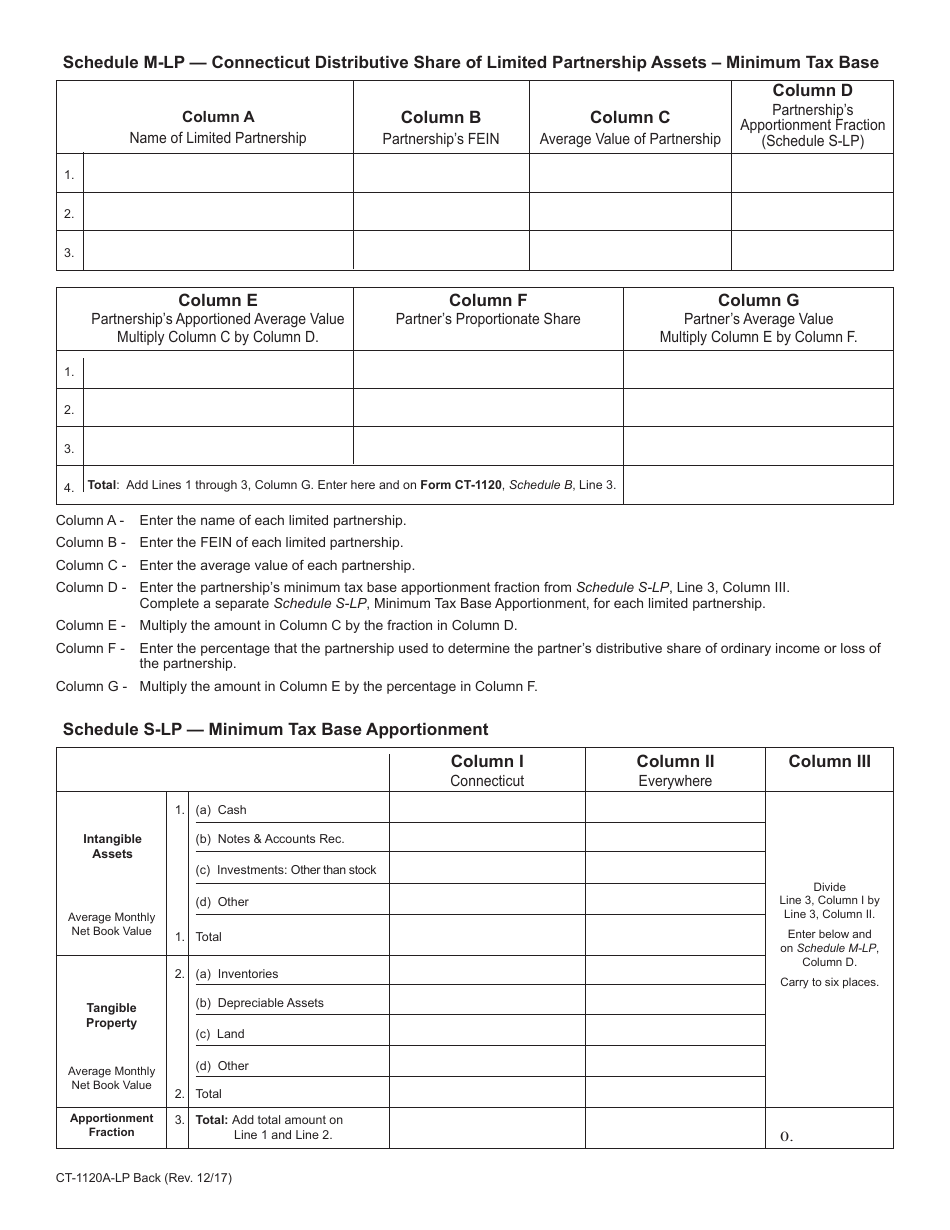

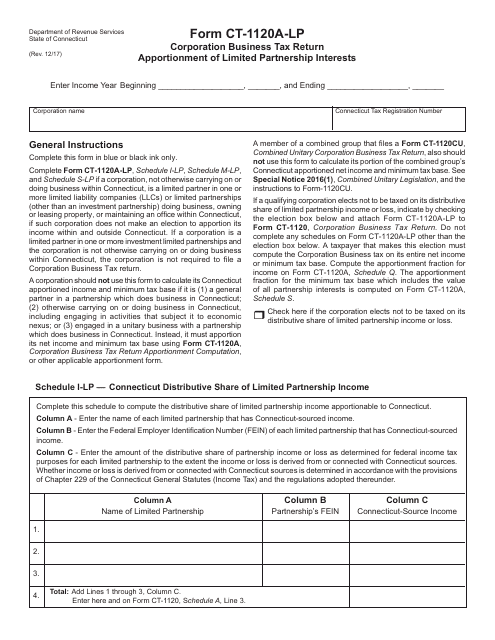

Form CT-1120A-LP Corporation Business Tax Return - Apportionment of Limited Partnership Interests - Connecticut

What Is Form CT-1120A-LP?

This is a legal form that was released by the Connecticut Department of Revenue Services - a government authority operating within Connecticut. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CT-1120A-LP?

A: Form CT-1120A-LP is the Corporation Business Tax Return used to apportion limited partnership interests in Connecticut.

Q: What is the purpose of Form CT-1120A-LP?

A: The purpose of Form CT-1120A-LP is to calculate and report the apportionment of limited partnership interests for corporations doing business in Connecticut.

Q: Who should file Form CT-1120A-LP?

A: Corporations that have limited partnership interests and are doing business in Connecticut should file Form CT-1120A-LP.

Q: What information is required on Form CT-1120A-LP?

A: Form CT-1120A-LP requires information about the corporation, its limited partnership interests, and its apportionment factors.

Q: When is Form CT-1120A-LP due?

A: Form CT-1120A-LP is due on the same date as the corporation's annual business tax return, which is usually due on the 15th day of the fourth month after the close of the fiscal year.

Form Details:

- Released on December 1, 2017;

- The latest edition provided by the Connecticut Department of Revenue Services;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form CT-1120A-LP by clicking the link below or browse more documents and templates provided by the Connecticut Department of Revenue Services.

Download Form CT-1120A-LP Corporation Business Tax Return - Apportionment of Limited Partnership Interests - Connecticut

1

2