![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8288

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8288

for the current year.

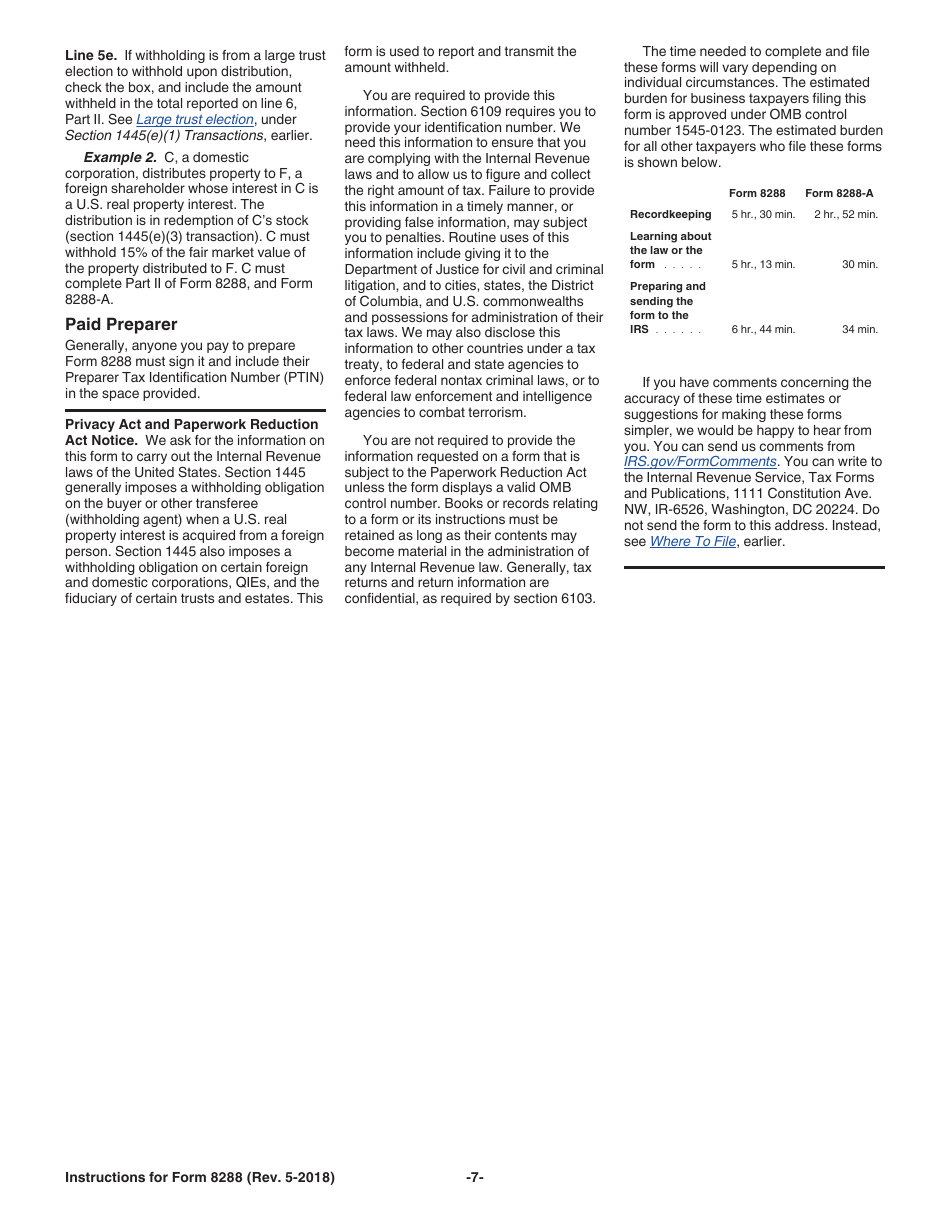

Instructions for IRS Form 8288 U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests

This document contains official instructions for IRS Form 8288 , U.S. Real Property Interests - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8288 is available for download through this link.

FAQ

Q: What is IRS Form 8288?

A: IRS Form 8288 is the U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests.

Q: Who needs to file IRS Form 8288?

A: Foreign persons who have disposed of U.S. real property interests need to file IRS Form 8288.

Q: What is the purpose of IRS Form 8288?

A: The purpose of IRS Form 8288 is to report and pay withholding tax on the sale or disposition of U.S. real property interests by foreign persons.

Q: How do I file IRS Form 8288?

A: IRS Form 8288 can be filed either electronically or by mail to the IRS.

Q: When is the deadline to file IRS Form 8288?

A: The deadline to file IRS Form 8288 is generally within 20 days after the transfer of the U.S. real property interest.

Q: What happens if I don't file IRS Form 8288?

A: Failure to file IRS Form 8288 or pay the withholding tax can result in penalties and interest being assessed by the IRS.

Instruction Details:

- This 7-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 8288 U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests

1

2

3

4

5

6

7