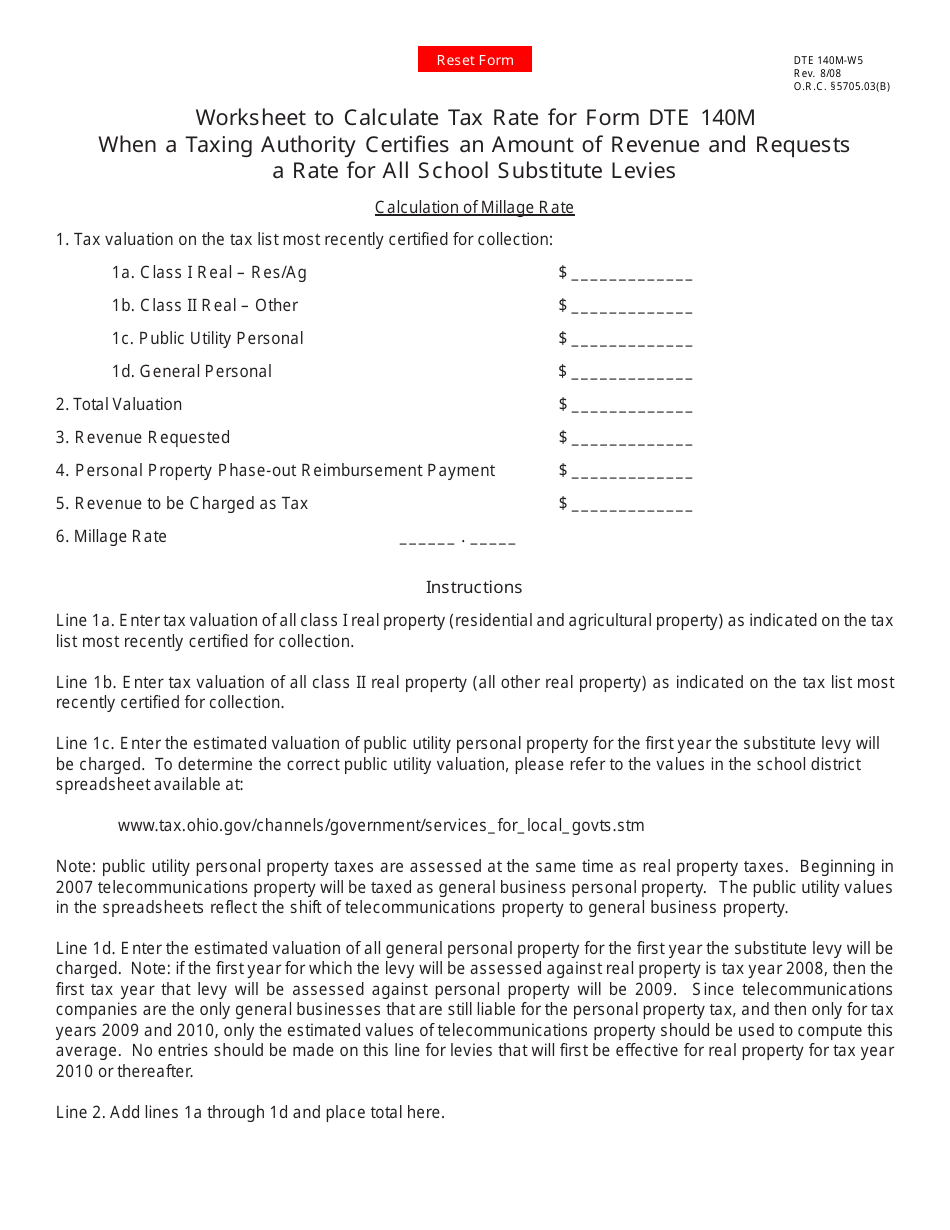

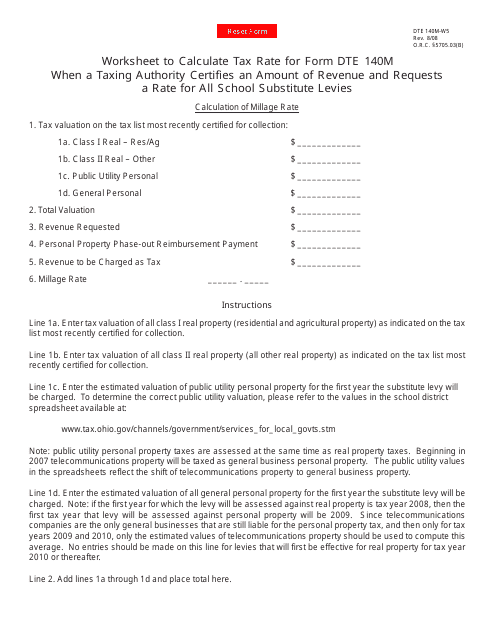

Form DTE140M-W5 Worksheet to Calculate Tax Rate for Form Dte 140m When a Taxing Authority Certifies an Amount of Revenue and Requests a Rate for All School Substitute Levies - Ohio

What Is Form DTE140M-W5?

This is a legal form that was released by the Ohio Department of Taxation - a government authority operating within Ohio. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form DTE140M-W5?

A: Form DTE140M-W5 is a worksheet used in Ohio to calculate the tax rate for Form DTE 140M when a taxing authority certifies an amount of revenue and requests a rate for all school substitute levies.

Q: What is Form DTE 140M?

A: Form DTE 140M is a form used in Ohio to report the current year's taxable value of qualifying property and the tax allocation for each tax year for all School Districts.

Q: What is a taxing authority?

A: A taxing authority is an entity that has the power to levy taxes or assess property for taxation purposes, such as a school district or local government.

Q: What is a school substitute levy?

A: A school substitute levy is a type of tax levy used to generate revenue for school districts in Ohio in place of or in addition to traditional property taxes.

Q: How is the tax rate calculated for Form DTE 140M?

A: The tax rate for Form DTE 140M is calculated using the information provided on Form DTE140M-W5, which includes the certified amount of revenue from the taxing authority.

Q: What information is needed to calculate the tax rate?

A: To calculate the tax rate, you will need the certified amount of revenue from the taxing authority and the taxable value of qualifying property for each tax year.

Form Details:

- Released on August 1, 2008;

- The latest edition provided by the Ohio Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form DTE140M-W5 by clicking the link below or browse more documents and templates provided by the Ohio Department of Taxation.

Download Form DTE140M-W5 Worksheet to Calculate Tax Rate for Form Dte 140m When a Taxing Authority Certifies an Amount of Revenue and Requests a Rate for All School Substitute Levies - Ohio

1

2