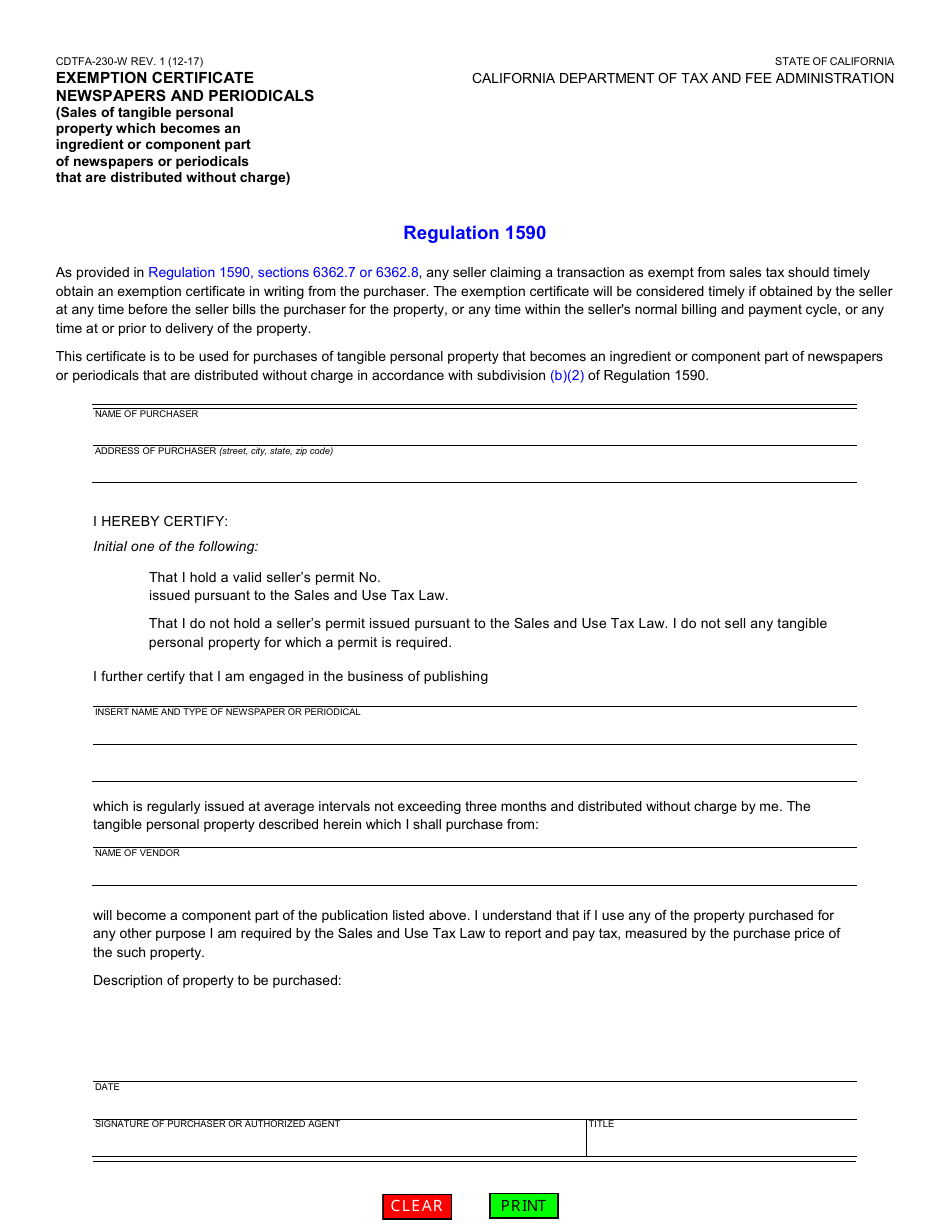

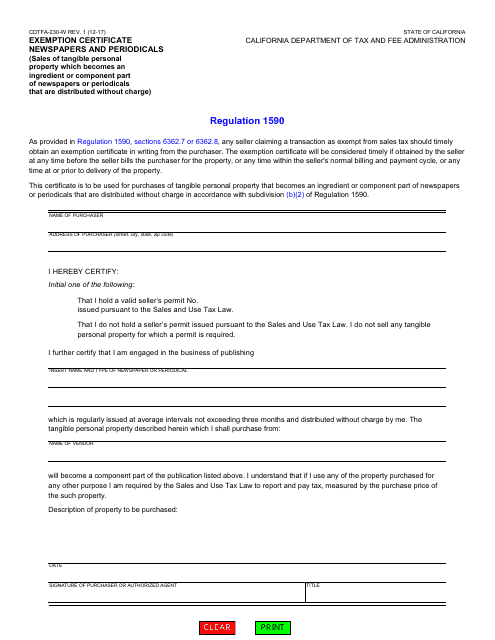

Form CDTFA-230-W Exemption Certificate Newspapers and Periodicals (Sales of Tangible Personal Property Which Becomes an Ingredient or Component Part of Newspapers or Periodicals That Are Distributed Without Charge) - California

What Is Form CDTFA-230-W?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CDTFA-230-W?

A: Form CDTFA-230-W is an exemption certificate used for sales of tangible personal property that becomes an ingredient or component part of newspapers or periodicals that are distributed without charge in California.

Q: What is the purpose of Form CDTFA-230-W?

A: The purpose of Form CDTFA-230-W is to certify that the sales of tangible personal property will be used as an ingredient or component part of newspapers or periodicals distributed without charge in California, qualifying for an exemption from sales tax.

Q: Who needs to use Form CDTFA-230-W?

A: Businesses that sell tangible personal property which becomes an ingredient or component part of newspapers or periodicals distributed without charge in California need to use Form CDTFA-230-W.

Q: What is the exemption provided by Form CDTFA-230-W?

A: Form CDTFA-230-W provides an exemption from sales tax for the sales of tangible personal property that becomes an ingredient or component part of newspapers or periodicals distributed without charge in California.

Q: Is there a deadline for submitting Form CDTFA-230-W?

A: There is no specific deadline mentioned for submitting Form CDTFA-230-W. However, it is recommended to submit the form before making the exempt sales.

Q: Are there any penalties for non-compliance with Form CDTFA-230-W?

A: Failure to comply with the requirements of Form CDTFA-230-W may result in the assessment of sales tax, penalties, and interest by the CDTFA.

Q: Can I use Form CDTFA-230-W for other types of sales?

A: No, Form CDTFA-230-W is specifically for sales of tangible personal property that becomes an ingredient or component part of newspapers or periodicals distributed without charge in California. It cannot be used for other types of sales.

Q: Do I have to pay sales tax if I use Form CDTFA-230-W?

A: No, if Form CDTFA-230-W is properly completed and the sales meet the qualifying criteria, the sales of tangible personal property used for newspapers or periodicals distributed without charge in California will be exempt from sales tax.

Q: Who can I contact for more information about Form CDTFA-230-W?

A: For more information about Form CDTFA-230-W, you can contact the California Department of Tax and Fee Administration (CDTFA) directly.

Form Details:

- Released on December 1, 2017;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-230-W by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.