![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-9

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-9

for the current year.

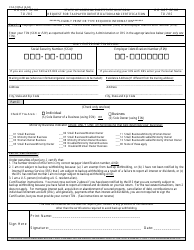

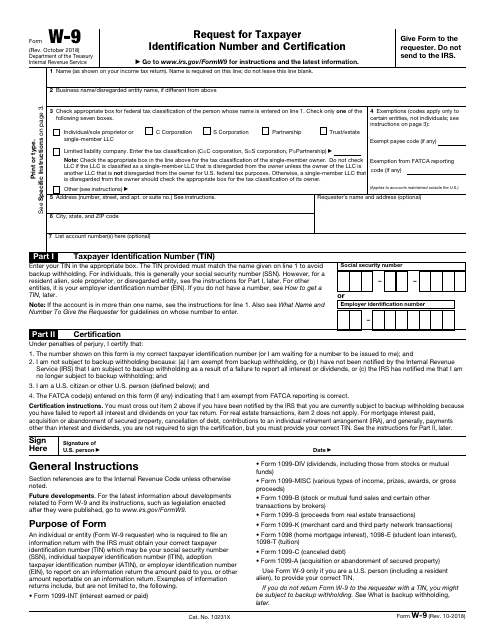

IRS Form W-9 Request for Taxpayer Identification Number and Certification

What Is IRS Form W-9?

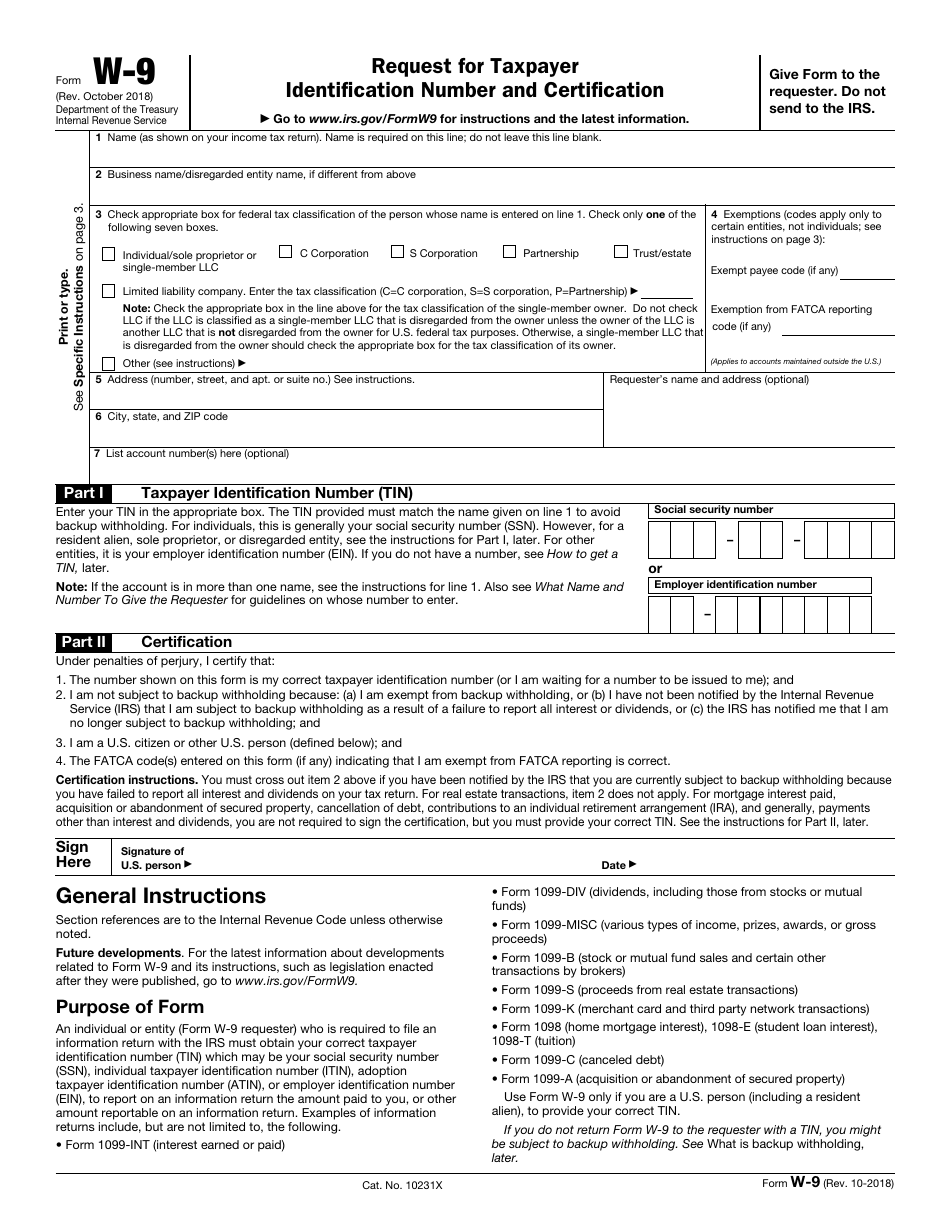

IRS Form W-9, Request for Taxpayer Identification Number and Certification , is an application that a taxpayer (a recipient) is required to fill out by an entity or an individual (a requester). This form is required because the requester must receive the recipient's correct Taxpayer Identification Number (TIN) in order to submit an information return to the Internal Revenue Service (IRS) on the amount paid to the recipient. The newest version of this form was released by the IRS on October 1, 2018 .

For example, when a company makes certain payments, they have to report them to the IRS. One of the most commonly used applications for it is Form 1099-MISC, which reports miscellaneous payments by entities. These payments can include things such as prizes, awards, gross proceeds, payments for services, medical payments, rents, nonemployee compensations, etc. In order to fill out Form 1099-MISC, an entrepreneur must know certain information about the receiver of the payment: name, address, and TIN. Since incorrect information submitted to the IRS is considered perjury, Form W-9 is needed here as an official request to the taxpayer to provide their correct TIN and certify that the number shown on the form is valid.

How to Get IRS Form W-9?

A taxpayer can be requested to fill out a W-9 tax form by a third party who is required to file an information return with the IRS. The form will be mailed or emailed to the taxpayer with a demand to send it back. A fillable version of the IRS W-9 Form is available for download below.

What Is a Substitute Form W-9?

According to the Form W-9 Requester Instructions, it is allowed for the requester to develop and use a substitute Form W-9. This substitute form must contain substantially similar information to the official IRS version. The key things that it must clearly state are as follows:

- A valid TIN.

- The taxpayer is a U.S. citizen or other U.S. person (explained in the text below).

- The FATCA code (if stated in the form) is valid.

Some states use a substitute to Form W-9 on a regular basis. Each substitute form says in which circumstance it's applicable. These states include:

How to Fill Out IRS Form W-9?

According to the Requester Instructions of Form W-9, the form is supposed to contain certain information:

- Name, address, and signature of the taxpayer;

- TIN in the form of Employer Identification Number (EIN) or Social Security Number (SSN);

- Certification that the information in the form is correct;

- General instructions that state the purpose of the form and other details.

The form is supposed to be filled out only if a taxpayer is considered to be a self-employed worker, such as a consultant, freelancer or independent contractor. If a taxpayer is an employee, then the W-9 Form is not applicable. In this case, a taxpayer is supposed to fill out IRS Form W-4 (Employee's Withholding Allowance Certificate), which is used only by employees to determine allowances.

The form is required for all of the following groups of people and entities:

- A U.S. citizen or a U.S. resident alien;

- A company or corporation created in the U.S. or under the laws of the U.S.;

- Any estate, other than a foreign estate;

- A domestic trust (as defined in Form W-9 instructions).

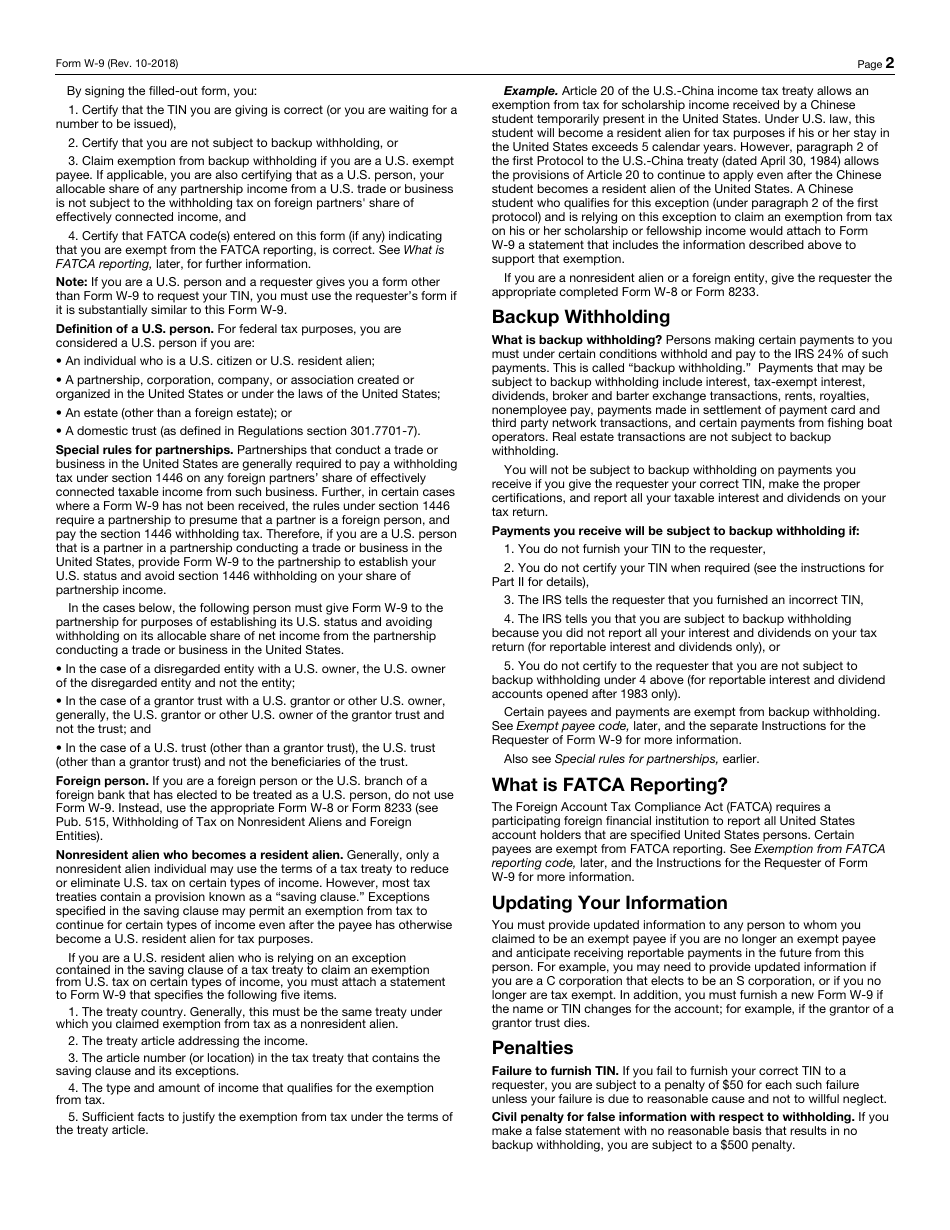

W-9 Form instructions state that the filled out form is supposed to be sent to the requester. It can be mailed or, if the requester established a system for electronic submissions that meet all the requirements stated in the instructions, it can be submitted electronically (or by fax). The electronic system requirements are stated as follows:

- The electronic system must guarantee that the information received by it is the information sent;

- The electronic system must provide the same information as the paper version of the document;

- The electronic system must be able to provide a hard copy of the document (if the IRS requests it);

- The electronic system must guarantee that the person submitting the information is the person identified on the form.

W-9 Related Forms:

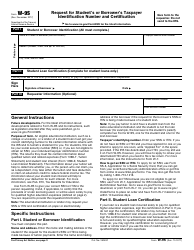

- Form W-9S, a Request for Student's or Borrower's Taxpayer Identification Number and Certification. This is an application which is supposed to be requested by an educational institution (a university or college) or a lender of a student loan from students or loan borrowers;

- Form W-9 (SP). This form is exactly the same as Form W-9, but it has been translated into Spanish

All three W-9 Forms contain the same amount of information and have equal legal force.

Download IRS Form W-9 Request for Taxpayer Identification Number and Certification

1

2

3

4

5

6