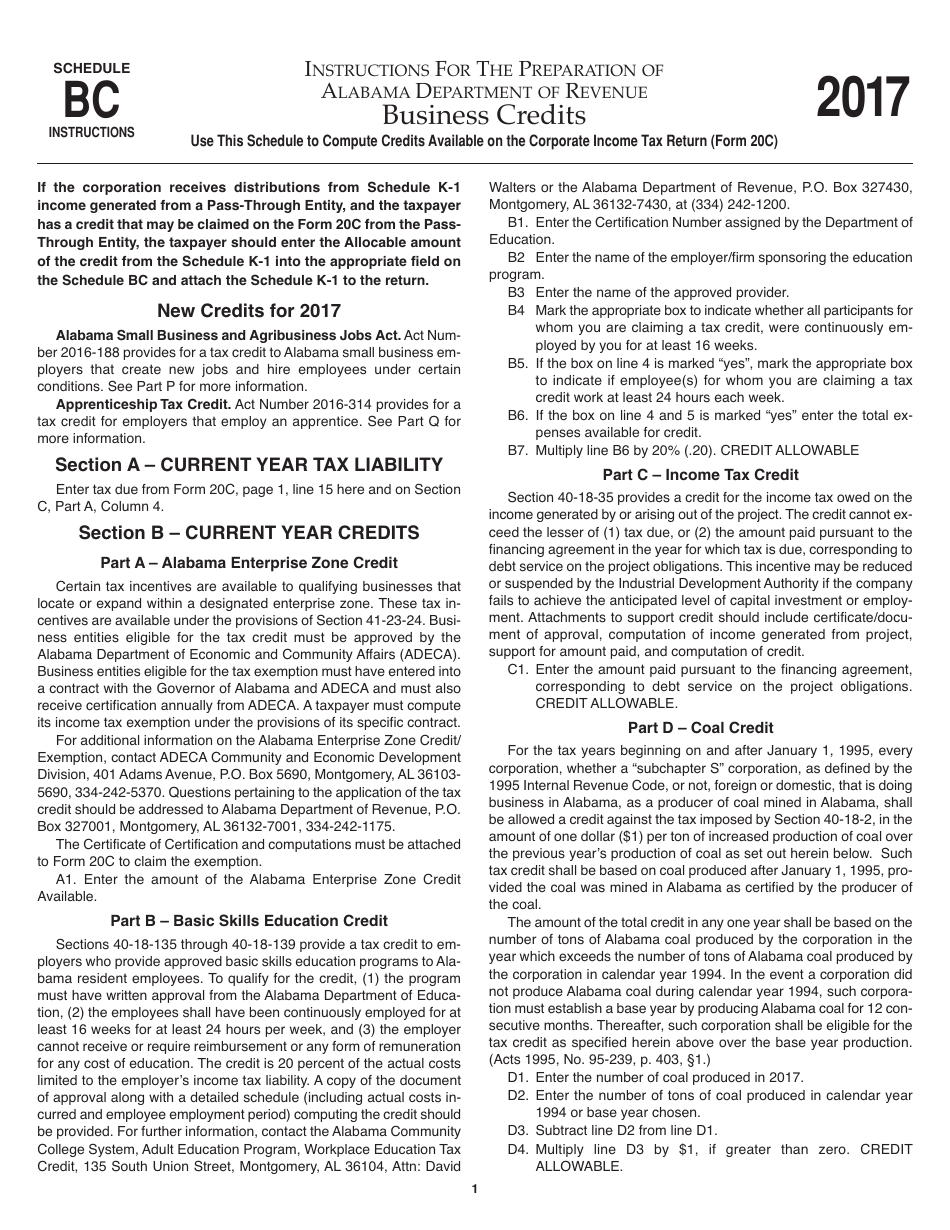

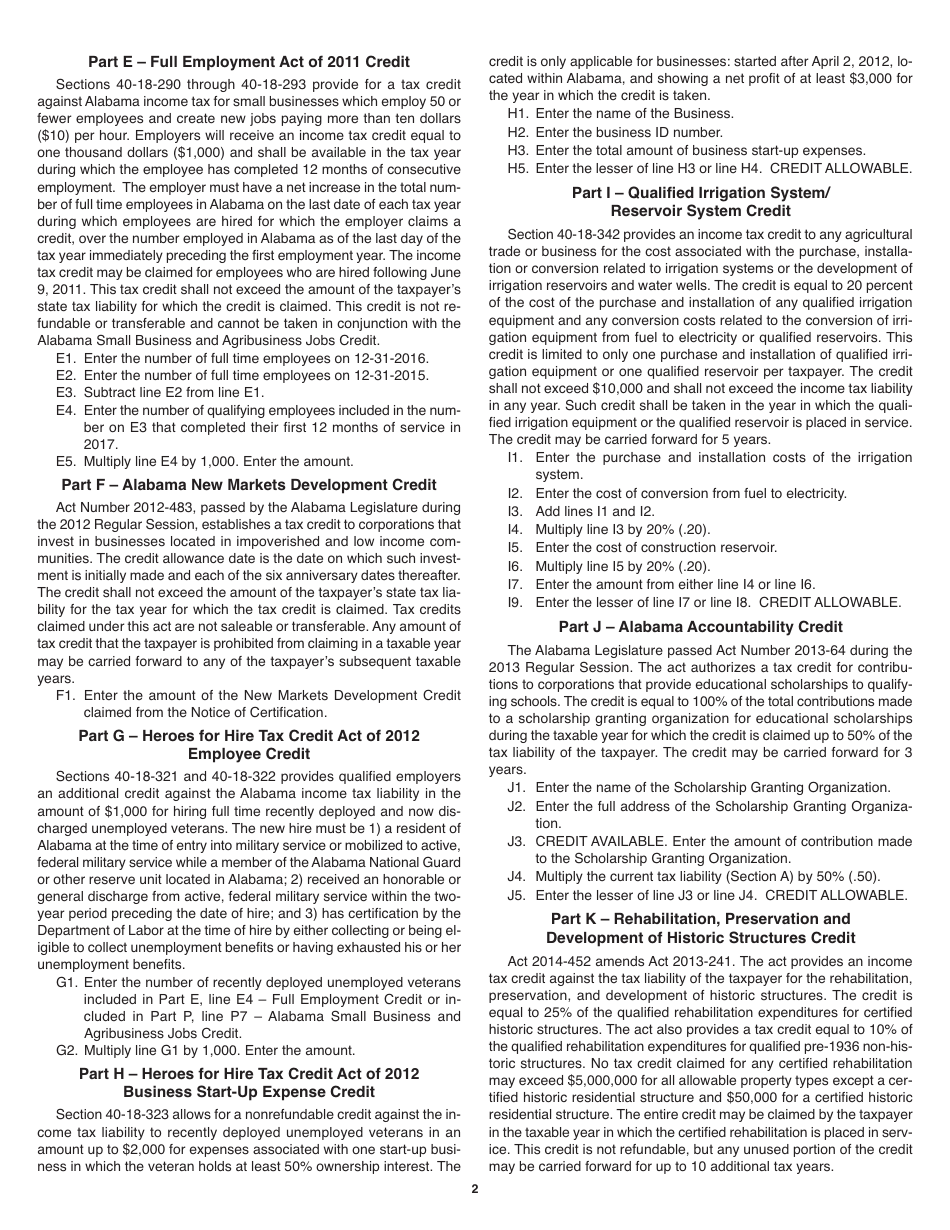

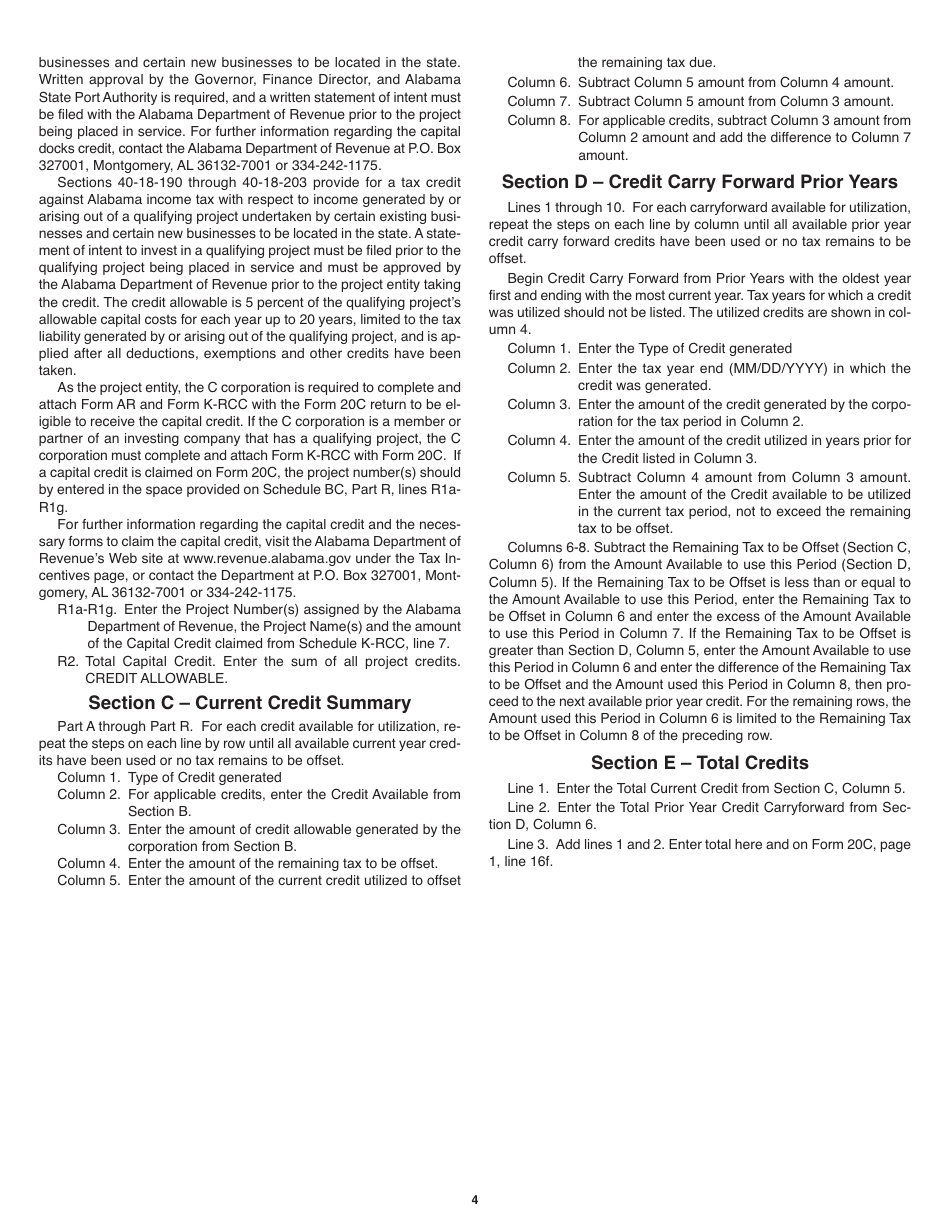

Instructions for Form 20C Schedule BC Business Credits - Alabama

This document contains official instructions for Form 20C Schedule BC, Business Credits - a form released and collected by the Alabama Department of Revenue.

FAQ

Q: What is Form 20C Schedule BC?

A: Form 20C Schedule BC is a tax form used in Alabama to claim business credits.

Q: What are business credits?

A: Business credits are tax incentives or deductions that businesses can claim to reduce their tax liability.

Q: Who needs to file Form 20C Schedule BC?

A: Businesses in Alabama that are eligible for any of the business credits listed on the form need to file Form 20C Schedule BC.

Q: What information is required on Form 20C Schedule BC?

A: Form 20C Schedule BC requires businesses to provide details about the specific business credits they are claiming.

Q: Is there a filing deadline for Form 20C Schedule BC?

A: Yes, the deadline for filing Form 20C Schedule BC is the same as the deadline for filing the Alabama Business Privilege Tax Return, which is typically due on April 15th.

Q: Can Form 20C Schedule BC be filed electronically?

A: Yes, businesses have the option to file Form 20C Schedule BC electronically.

Q: What should I do if I have questions or need assistance with Form 20C Schedule BC?

A: If you have questions or need assistance with Form 20C Schedule BC, you can contact the Alabama Department of Revenue for guidance.

Instruction Details:

- This 4-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Alabama Department of Revenue.

1

2

3

4