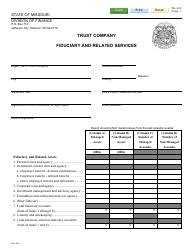

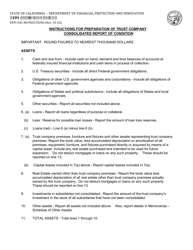

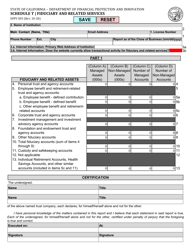

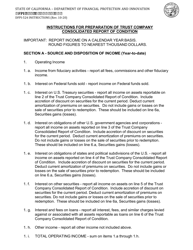

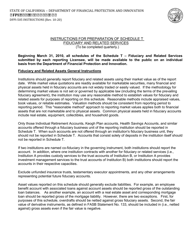

Instructions for Form TR-102 Trust Company Fiduciary and Related Services - Missouri

This document contains official instructions for Form TR-102 , Trust Company Fiduciary and Related Services - a form released and collected by the Missouri Department of Commerce and Insurance.

FAQ

Q: What is Form TR-102?

A: Form TR-102 is a document used in Missouri for reporting trust company fiduciary and related services.

Q: Who needs to file Form TR-102?

A: Trust companies in Missouri are required to file Form TR-102.

Q: What is the purpose of Form TR-102?

A: The purpose of Form TR-102 is to report information about trust company fiduciary and related services in Missouri.

Instruction Details:

- This 8-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Missouri Department of Commerce and Insurance.

Download Instructions for Form TR-102 Trust Company Fiduciary and Related Services - Missouri

1

2

3

4

5

6

7

8