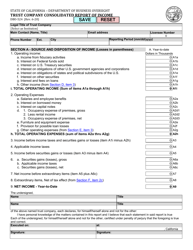

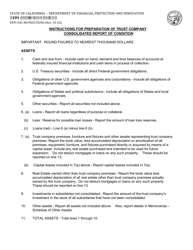

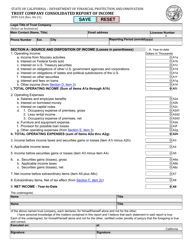

Instructions for Form TR-100 Trust Company Consolidated Report of Condition and Income - Missouri

This document contains official instructions for Form TR-100 , Trust Company Consolidated Report of Condition and Income - a form released and collected by the Missouri Department of Commerce and Insurance.

FAQ

Q: What is Form TR-100?

A: Form TR-100 is the Trust Company Consolidated Report of Condition and Income in Missouri.

Q: Who needs to file Form TR-100?

A: Trust companies in Missouri are required to file Form TR-100.

Q: What is the purpose of Form TR-100?

A: Form TR-100 serves to report the financial condition and income of trust companies in Missouri.

Q: When is Form TR-100 due?

A: Form TR-100 is due within 45 days after the end of the calendar quarter.

Q: Is there a filing fee for Form TR-100?

A: Yes, there is a filing fee associated with Form TR-100. The fee amount may vary.

Instruction Details:

- This 12-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Missouri Department of Commerce and Insurance.

Download Instructions for Form TR-100 Trust Company Consolidated Report of Condition and Income - Missouri

1

2

3

4

5

6

7

8

9

10

11

12